A Look At Clover Health (CLOV) Valuation After First Positive GAAP Net Income And Q1 2026 Turnaround Progress

Clover Health CLOV | 0.00 |

Clover Health Investments (CLOV) drew fresh attention after reporting its first-ever positive GAAP net income alongside robust Q1 2026 results, with Medicare Advantage membership growth, strong retention, and improving cohort profitability in focus for investors.

The Q1 2026 update and first positive GAAP net income appear to sit behind a sharp shift in sentiment, with a 30 day share price return of 59.82% and 90 day share price return of 67.46%, even as the 1 year total shareholder return declined 5.15% and the 3 year total shareholder return remains very large.

If the Clover story has you watching healthcare technology more closely, this could be a good moment to see what else is moving via 29 healthcare AI stocks

After such a sharp short term rally and a first profitable quarter on GAAP terms, investors now face a simple question: is Clover Health still trading at a discount, or is the recent momentum already pricing in future growth?

Most Popular Narrative: 24.3% Overvalued

At a last close of $3.50 versus a narrative fair value of $2.82, the most followed view sees Clover Health trading ahead of its core assumptions while hinging heavily on long term execution.

The analysts have a consensus price target of $2.82 for Clover Health Investments based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $3.2, and the most bearish reporting a price target of just $2.5.

The narrative leans on rapid earnings improvement, double digit revenue growth and a rich future earnings multiple, all anchored by a single discount rate and tight profitability band. It raises the question of which assumptions do the heavy lifting in that fair value and how sensitive the outcome is to even small changes in margins or growth.

Result: Fair Value of $2.82 (OVERVALUED)

However, this narrative still depends on sensitive assumptions. Rising medical and pharmacy costs, along with potential Medicare reimbursement changes, could both quickly challenge it.

Another View: Cash Flows Point In The Opposite Direction

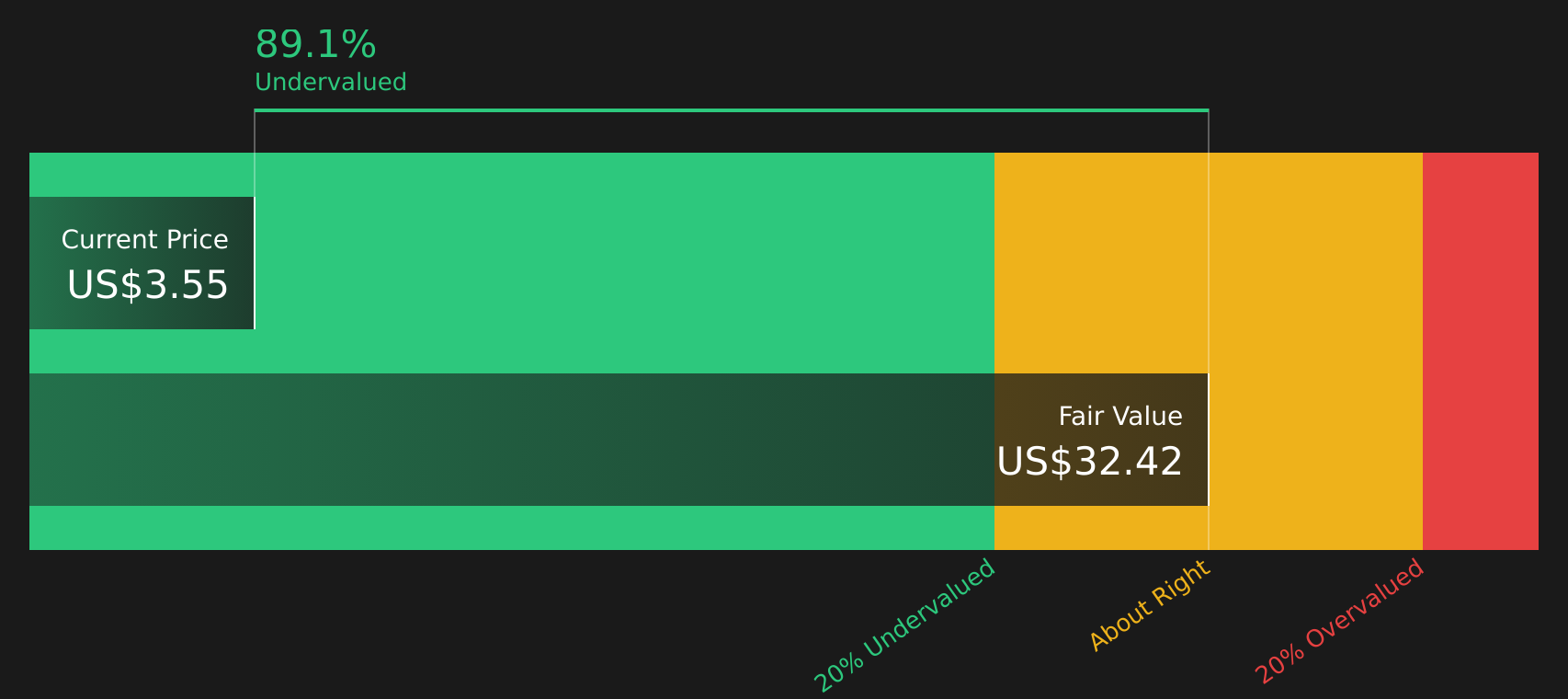

While the analyst narrative suggests Clover Health is 24.3% overvalued at $3.50 versus a $2.82 fair value, our DCF model points the other way. In that framework, the stock trades well below an estimated future cash flow value of $32.42, which raises a very different question for investors.

Next Steps

With sentiment clearly split between risk and reward, this is the moment to look through the data yourself and decide where you stand. To help you weigh both sides, take a closer look at the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Clover has sharpened your focus, do not stop here. Widen your watchlist and let fresh ideas compete for a place in your portfolio.

- Spot potential value opportunities early by scanning 54 high quality undervalued stocks and see which stocks currently line up with stronger fundamentals than their prices suggest.

- Prioritise resilience by checking out 66 resilient stocks with low risk scores so you can focus on companies with lower risk scores instead of guessing where the next shock might land.

- Hunt for underfollowed prospects using the screener containing 21 high quality undiscovered gems and make sure you are seeing quality ideas before they appear on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.