A Look At CMS Energy (CMS) Valuation As Muskegon Solar Project Starts Powering Michigan Homes

CMS Energy Corporation CMS | 78.58 | +0.85% |

CMS Energy (CMS) is back in focus after Consumers Energy began operating Muskegon Solar, a 250 megawatt project on 1,900 acres that is sized to supply electricity for about 40,000 Michigan homes and businesses.

At a share price of $69.85, CMS Energy has seen a 5.7% decline in its 90 day share price return, while its 1 year total shareholder return of 8.6% indicates steadier long term momentum. Recent renewable projects like Muskegon Solar may influence how investors evaluate future growth and risk.

If Muskegon Solar has you thinking about where the next energy story could come from, it may be worth scanning other regulated utilities and infrastructure peers through fast growing stocks with high insider ownership.

With a recent 5.7% 90 day share price decline, a 1 year total return of 8.6% and a value score of 2, the real question is whether CMS Energy still trades below its fundamentals or if the market already prices in future growth.

Most Popular Narrative: 10.4% Undervalued

With CMS Energy’s fair value in the narrative set at $78 against a last close of $69.85, the story hinges on how future cash flows are being framed.

The accelerating demand for electricity, driven in part by large new data center projects and strong population and business growth within Michigan, is set to sustainably boost sales growth above prior forecasts, likely resulting in stronger top-line revenue and rate base expansion.

Want to see what sits behind that optimism on sales and rate base? The narrative leans heavily on projected revenue growth, expanding margins, and a premium earnings multiple. Curious how those pieces fit together to support that $78 fair value?

Result: Fair Value of $78 (UNDERVALUED)

However, this upbeat story can unravel if data center and load growth slow, or if Michigan regulators become less supportive on future rate cases and recovery.

Another View: DCF Is More Cautious

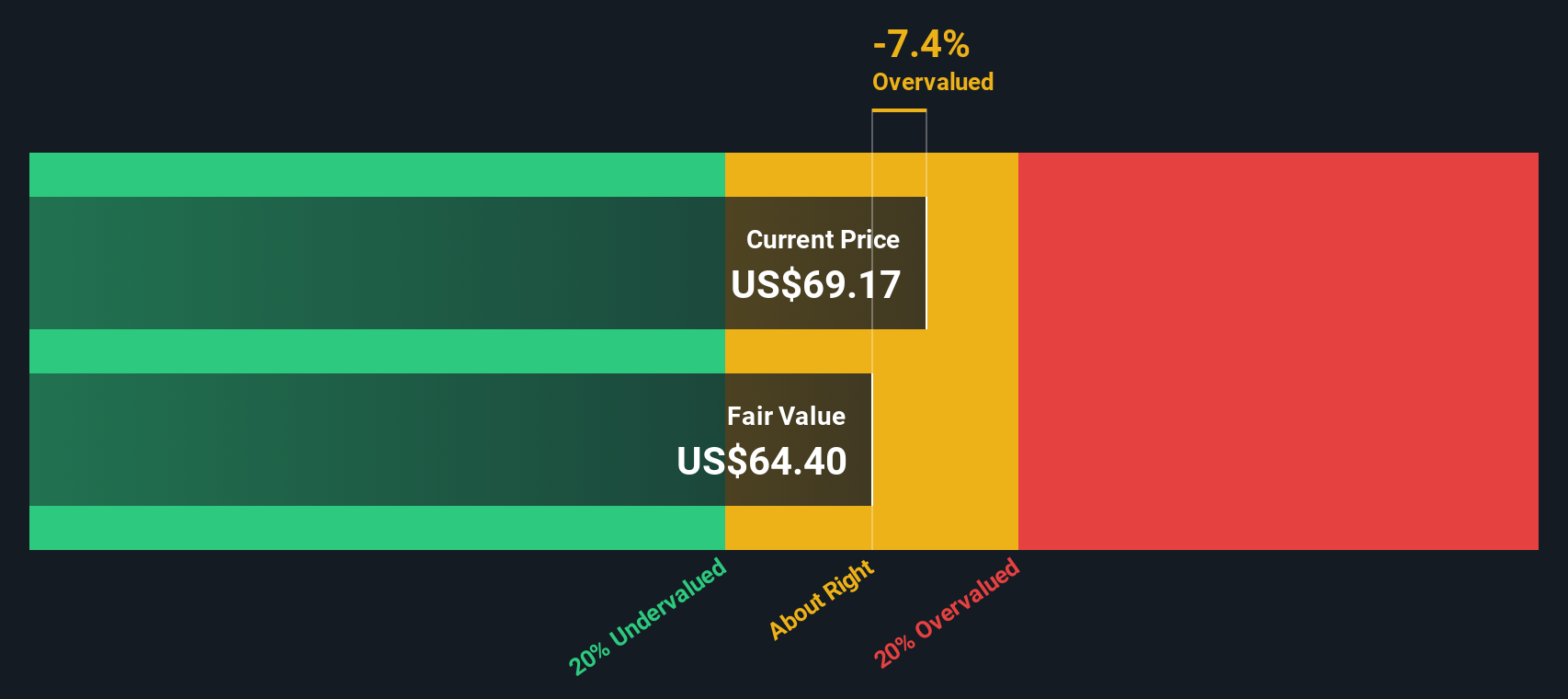

The 10.4% undervalued narrative hinges on analyst forecasts and a premium P/E. Our DCF model is less upbeat, with a fair value of US$66.72 versus the US$69.85 share price, which suggests that CMS Energy may be slightly overvalued rather than cheap. Which perspective seems more realistic to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CMS Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 881 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own CMS Energy Narrative

If you see the numbers differently or just prefer to test your own assumptions, you can build a complete CMS Energy story in minutes by starting with Do it your way.

A great starting point for your CMS Energy research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If CMS Energy is on your radar, do not stop there. Broaden your watchlist with ideas that match your style and keep fresh opportunities on the table.

- Spot potential value early by checking out these 3545 penny stocks with strong financials that pair smaller market caps with stronger balance sheets and fundamentals than you might expect.

- Target growth themes by scanning these 28 AI penny stocks that are tied to artificial intelligence trends without having to sift through hundreds of tickers on your own.

- Focus on price and cash flow discipline by reviewing these 881 undervalued stocks based on cash flows that screen for companies trading below what their cash flows may imply.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.