A Look At Colgate-Palmolive (CL) Valuation As Analyst Upgrades Highlight Defensive Appeal

Colgate-Palmolive Company CL | 85.14 | -0.32% |

Analyst attention shifts to Colgate-Palmolive (CL)

Recent calls from Barclays and Wells Fargo have pushed Colgate-Palmolive (CL) back into focus, as both firms reassessed the stock during a period when many investors are rotating toward defensive consumer names.

Those reassessments come as Colgate-Palmolive’s share price has quietly trended higher, with a 30-day share price return of 7.36% and a 90-day share price return of 10.01%. Its 3-year total shareholder return of 21.98% indicates steadier, longer-run compounding.

If Colgate’s recent move has you thinking about what else might be gaining interest, this could be a good time to check out fast growing stocks with high insider ownership.

With Colgate-Palmolive trading at $85.81 against an average analyst target of about $88.79, plus an indicated 30.67% intrinsic discount, the key question is whether this reflects a genuine value gap or whether the market is already pricing in expectations about future growth.

Most Popular Narrative: 1.9% Undervalued

Colgate-Palmolive's most followed narrative pegs fair value at about $87.47, only slightly above the $85.81 last close, which puts the focus squarely on the assumptions behind that number.

Productivity and restructuring initiatives ($200–$300 million over three years) are designed to free up resources for innovation, digital, and R&D investments, enabling incremental margin expansion and additional reinvestment for growth.

Curious what kind of revenue trajectory, margin lift and future P/E multiple are baked into that fair value, and how much depends on buybacks and emerging markets execution? The full narrative spells out the exact earnings path it assumes, the margin level it needs to hold and the premium multiple it expects the market to pay.

Result: Fair Value of $87.47 (UNDERVALUED)

However, this hinges on cost pressures and private label competition staying contained. Sustained input inflation or weaker pet nutrition demand could quickly challenge those fair value assumptions.

Another View: Earnings Multiple Sends A Different Signal

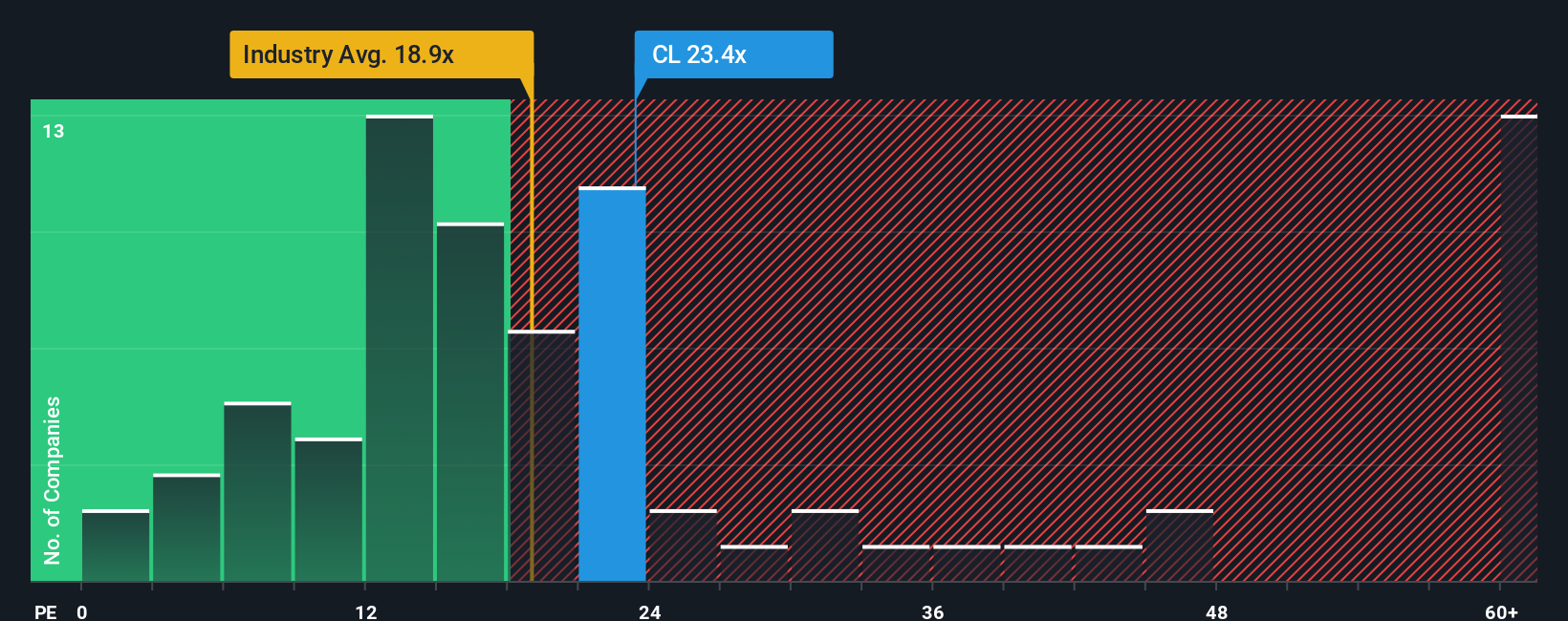

While the most followed narrative treats Colgate-Palmolive as 1.9% undervalued, the earnings multiple tells a cooler story. The stock trades on a P/E of 23.8x versus 17.2x for the global Household Products group and a fair ratio of 19x, as well as 21.2x for peers. That premium suggests less margin for error if growth or margins fall short. Which signal do you trust more?

Build Your Own Colgate-Palmolive Narrative

If you look at the numbers and come to a different conclusion, or just want to test your own thesis, you can build a complete narrative in minutes, starting with Do it your way.

A great starting point for your Colgate-Palmolive research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready to hunt for your next idea?

If Colgate-Palmolive has sharpened your thinking, do not stop here. Use the screener to quickly spot fresh ideas that fit what you care about most.

- Target higher income potential by scanning these 12 dividend stocks with yields > 3% that may suit investors focused on regular cash returns.

- Tap into future-facing themes by checking these 24 AI penny stocks that are tied to artificial intelligence trends.

- Pursue value focused opportunities by reviewing these 873 undervalued stocks based on cash flows that currently trade below their estimated cash flow worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.