A Look At Commvault Systems (CVLT) Valuation After Earnings Beat And Softer Fiscal 2026 Guidance

Commvault Systems, Inc. CVLT | 79.93 | +1.94% |

Commvault Systems (CVLT) sent mixed signals to the market after third quarter results topped expectations, but fiscal 2026 revenue guidance fell short, sparking a sharp sell off despite buybacks and new Google Cloud product updates.

The earnings beat, softer fiscal 2026 guidance and ongoing buybacks have all fed straight into the price action, with a 7 day share price return of 33.75% decline and a 1 year total shareholder return of 46.21% decline. Meanwhile, 3 and 5 year total shareholder returns remain positive, suggesting recent momentum has faded after a stronger multi year run.

If this kind of volatility has you looking at other opportunities in software and cloud security, it could be a good moment to cast the net wider with high growth tech and AI stocks.

With earnings and guidance now on the table, the question is whether Commvault’s 33% slide and current valuation already reflect a slower growth path, or if the recent sell off has created a genuine mispricing of future growth.

Most Popular Narrative: 50.9% Undervalued

Commvault Systems' most followed valuation narrative pegs fair value at about $174.58 per share, almost double the recent $85.70 close, putting a spotlight on what would need to go right to close that gap.

Rapid expansion and successful cross-sell/upsell momentum within the SaaS (Metallic) platform, evidenced by 63% SaaS ARR growth, a 45% increase in multi-product customers, and 125% SaaS net dollar retention, point to continued improvement in the quality and predictability of future revenues, directly supporting margin expansion and higher earnings visibility.

Want to understand how recurring subscription mix, expected earnings growth, and a premium future earnings multiple all feed into that valuation gap story? The key threads are clear, and the exact revenue ramp, margin path, and discount rate assumptions are where the narrative really gets interesting.

Result: Fair Value of $174.58 (UNDERVALUED)

However, shorter term contracts and ongoing margin pressure could easily undermine that undervalued case if renewal behavior or deal timing is weaker than analysts expect.

Another View: High Multiple Signals Caution

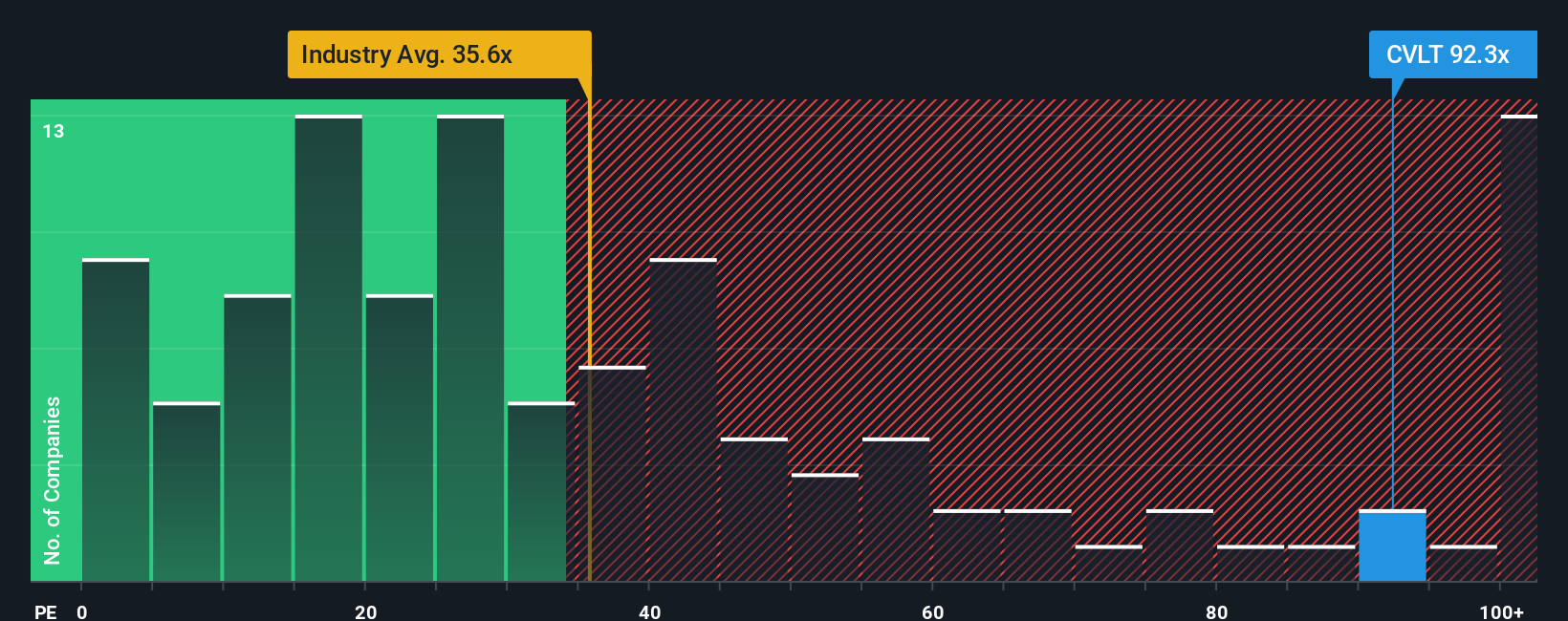

While the narrative-based fair value suggests strong upside, the current P/E of 43.3x tells a different story. It is above the estimated fair ratio of 33.9x, slightly ahead of the peer average of 42.7x, and well above the US Software industry at 28.2x. That kind of premium raises a simple question: how much optimism are you comfortable paying for?

Build Your Own Commvault Systems Narrative

If you see the story playing out differently, or prefer to review the numbers yourself, you can build a personalised view in minutes with Do it your way.

A great starting point for your Commvault Systems research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one company, you miss chances elsewhere, so take a few minutes now to scan fresh ideas that might better fit your goals.

- Spot potential rebound candidates by checking out these 3538 penny stocks with strong financials that pair smaller share prices with stronger financials than you might expect.

- Ride the next wave of automation by reviewing these 24 AI penny stocks as AI reshapes everything from software tools to data driven decision making.

- Hunt for value minded ideas by scanning these 887 undervalued stocks based on cash flows that focus on cash flow based pricing, not just headline stories.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.