A Look At COMPASS Pathways (CMPS) Valuation After Phase 3 COMP360 Data And Priority Review Voucher

COMPASS Pathways Plc Sponsored ADR CMPS | 0.00 |

COMPASS Pathways (CMPS) stock is in focus after the company reported a Q1 2026 net income of US$91.2 million and basic earnings per share of US$0.71, reversing a loss a year earlier.

The share price has been volatile, but the recent phase 3 data for COMP360 and the National Priority Voucher appear to be feeding into strong momentum. A 30 day share price return of 55.71% and a 1 year total shareholder return of 138.39% reflect how quickly sentiment has shifted in both the short and longer term.

If this kind of momentum in mental health treatment is on your radar, it may be worth seeing what else is moving across 29 healthcare AI stocks

With COMPASS Pathways now profitable, a market cap of about US$1.4b and a share price still below some analyst targets, the key question is simple: is there still mispricing here, or are markets already banking on future growth?

Most Popular Narrative: 52.7% Undervalued

Analysts following COMPASS Pathways see a fair value around $21.92 per share, compared with the last close at $10.37, which is a substantial valuation gap built on ambitious assumptions about COMP360 and its potential uses.

Completion of enrollment in the COMP006 Phase III trial and the plan to use 9 week data from Part A together with 26 week COMP005 data to support a rolling NDA process could shorten the path to potential approval, which would bring revenue forward and may support earlier earnings visibility.

Want to see what is sitting behind that bold valuation gap and the focus on COMP360? The narrative leans heavily on rapid revenue build, margin expansion and a premium future earnings multiple that is more often associated with mature, high conviction compounders rather than a company that currently reports no revenue and ongoing losses. The detailed storyline connects these moving parts into one fair value number.

Result: Fair Value of $21.92 (UNDERVALUED)

However, this hinges on COMP360 clearing Phase III and FDA review, and on COMPASS managing cash needs without heavy dilution if timelines or costs shift.

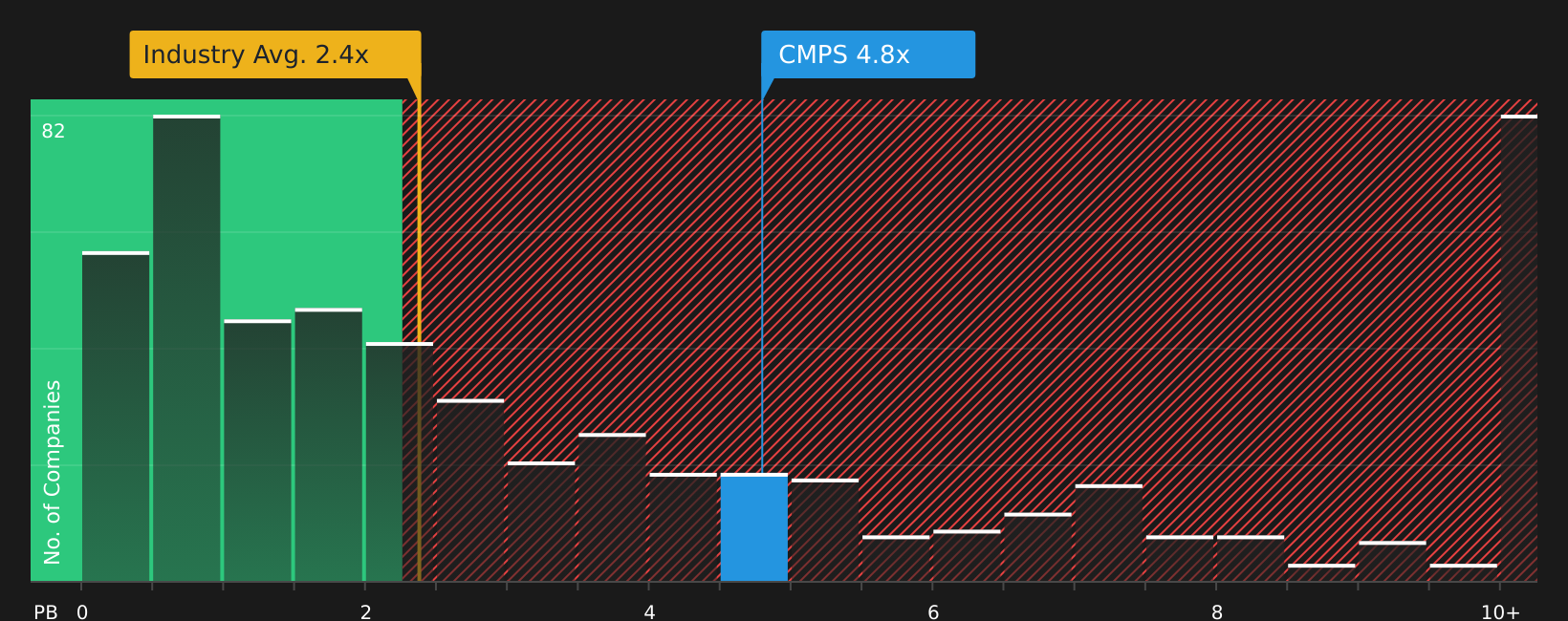

Another View: Price Versus Book Value

The analyst narrative leans on future earnings, but the current P/B ratio tells a different story. CMPS trades at 4.3x book value, compared with 2.4x for the US Biotechs industry and 2.7x for peers, so investors are paying a clear premium for each dollar of net assets.

That premium could signal confidence in COMP360, or it could simply stretch the margin for error if trials or approvals take longer than expected. The key question is whether you think the story justifies paying more than the sector for the same balance sheet foundation.

Next Steps

Sentiment around COMPASS Pathways is clearly split, so this is a moment to move fast, review the numbers, and shape your own stance using 2 key rewards and 4 important warning signs

Looking for more investment ideas?

If COMPASS Pathways has caught your attention, do not stop here. Broader context across sectors and styles can sharpen your conviction and reveal alternatives.

- Spot potential mispricing by reviewing stocks that screen as high quality yet priced attractively through the 51 high quality undervalued stocks.

- Strengthen your income stream by checking companies that show resilient payouts in the 14 dividend fortresses.

- Guard against unnecessary shocks by focusing on companies flagged in the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.