A Look At Constellation Energy (CEG) Valuation After Calpine Deal And New Power Policy Proposals

Constellation Energy Corporation CEG | 272.82 | -2.38% |

Government plans for emergency power auctions, rate caps, and new plants have put Constellation Energy (CEG) in the spotlight just as its Calpine acquisition creates the nation’s largest electric producer and reshapes its clean energy mix.

Those policy headlines and the Calpine deal have landed on a stock that was already under pressure, with a 30 day share price return of a 22.8% decline and a year to date share price return of a 28.6% decline, even though the three year total shareholder return sits at a 208.6% gain, suggesting long term holders have still seen very strong gains while shorter term momentum has faded.

If you are watching how power producers react to changing grid needs and policy risk, this is also a moment to scan 87 nuclear energy infrastructure stocks as potential peers in the nuclear and energy infrastructure space.

With shares down double digits over the past year but three year returns still very strong, and with analyst targets well above the recent US$261.42 price, is this weakness a buying opportunity or is the market already pricing in future growth?

Most Popular Narrative: 34.6% Undervalued

The most followed valuation narrative puts Constellation Energy’s fair value at about $399.93 per share, well above the recent $261.42 close, and anchors that gap to nuclear backed cash flows and long term power demand.

Strategic investments and progress in nuclear plant restarts (Crane Clean Energy Center), upgrades (900MW in engineering), and selective M&A (Calpine acquisition) provide visible avenues for substantial capacity additions and operational synergies, enhancing EBITDA and free cash flow over the medium to long term.

Want to see what is built into that gap between price and fair value? The narrative leans on steady revenue gains, firmer margins, and a richer future earnings multiple. Curious how those moving parts fit together to justify a near $400 handle?

Result: Fair Value of $399.93 (UNDERVALUED)

However, you also need to weigh the possibility that rising nuclear regulatory and decommissioning costs, or slower data center deal flow, could challenge those upbeat earnings assumptions.

Another View: Price Tag Looks Full

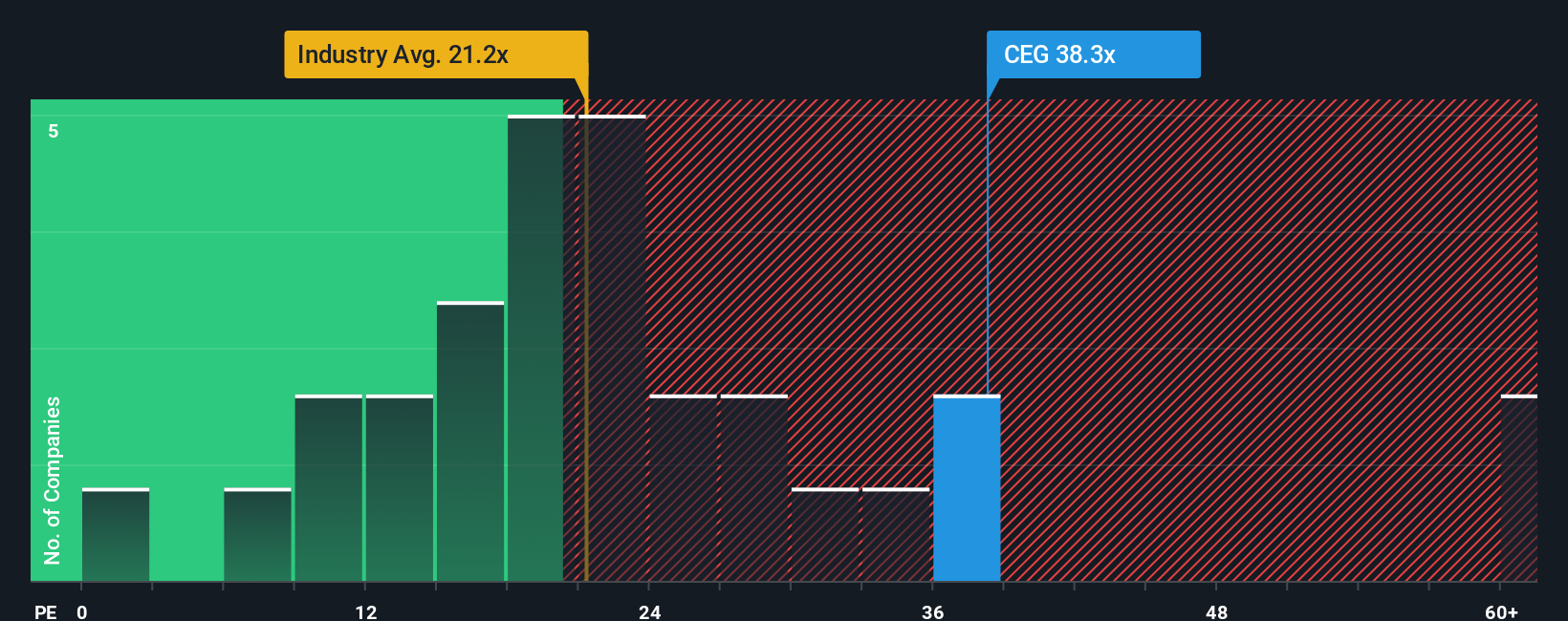

The narrative fair value says Constellation Energy looks 21.1% undervalued, yet the P/E ratio of 34.6x sits well above the US Electric Utilities industry at 20.9x, the peer average at 21.6x, and even the 32.7x fair ratio our model points to. That richer multiple could mean less room for error if growth or power prices soften, so how much premium are you really comfortable paying for this story?

Build Your Own Constellation Energy Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to build your own view from scratch, you can piece together your version of the Constellation Energy story in just a few minutes, Do it your way.

A great starting point for your Constellation Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at a single company; broaden your watchlist now or risk missing better aligned opportunities.

- Capture potential value by scanning our list of 53 high quality undervalued stocks that currently screen as high quality on both cash flows and balance sheet strength.

- Strengthen your income stream by reviewing 14 dividend fortresses that combine 5%+ yields with a focus on stability and capital protection.

- Protect your downside by filtering for 86 resilient stocks with low risk scores so you can anchor your portfolio with companies that carry lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.