A Look At Core Scientific (CORZ) Valuation As Analysts Highlight Shift Toward High Performance Computing Leasing

Core Scientific CORZ | 16.23 | +6.08% |

Keefe, Bruyette & Woods recently highlighted a potentially attractive setup for Core Scientific (CORZ) as the company shifts focus from bitcoin mining to high performance computing leasing, drawing attention ahead of its February 18, 2026 earnings report.

At a share price of $18.09, Core Scientific has seen a 12.01% 7 day share price return and a 19.33% 90 day share price return, while its 1 year total shareholder return of 49.63% points to momentum building around the shift toward high performance computing leasing and recent analyst commentary.

If this focus on compute infrastructure has your attention, it could be a good time to scan a wider set of opportunities in AI infrastructure using our 34 AI infrastructure stocks as a starting point.

With shares at US$18.09 and analysts pointing to a US$26.03 target, along with strong recent returns, is Core Scientific still underappreciated by the market, or are investors already paying up for future growth potential?

Most Popular Narrative: 32.6% Undervalued

At $18.09 per share versus a most-followed narrative fair value of $26.82, the gap reflects a story built around AI power capacity and future hosting economics.

Updated models increasingly assume that Core Scientific will monetize its substantial power pipeline through high performance compute and AI infrastructure, which is seen as a structurally higher growth, higher multiple opportunity than pure Bitcoin mining.

Curious what sits behind that higher multiple view? Revenue expansion, margin rebuild, and a reworked earnings profile all feed into this target. The full narrative lays out how these assumptions tie back to that $26.82 figure and why a higher required return of just over 9% still supports an undervalued characterization.

Result: Fair Value of $26.82 (UNDERVALUED)

However, the narrative also leans on a successful pivot to HPC hosting and reduced reliance on CoreWeave, so any execution slip or client concentration shock could quickly challenge it.

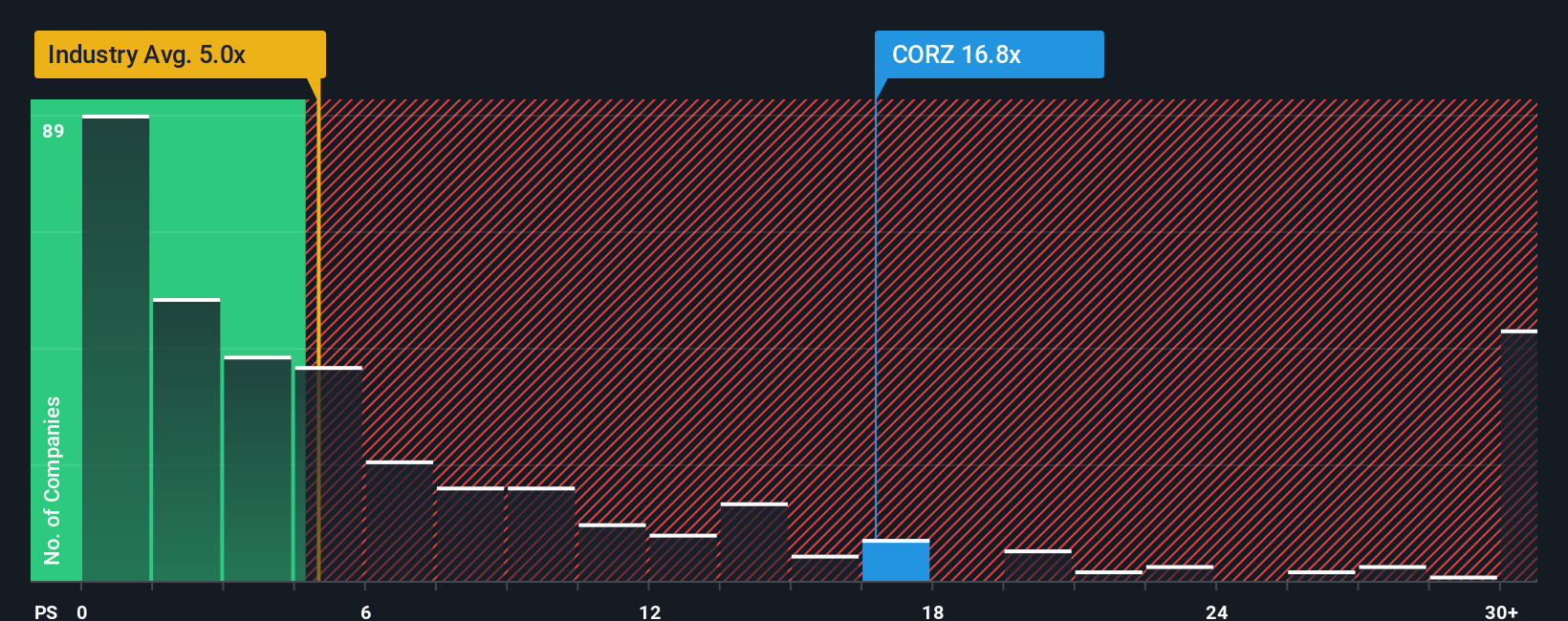

Another View: Expensive On Sales-Based Metrics

The narrative fair value of $26.82 suggests upside, but the current P/S of 16.8x tells a different story. That compares with 2.2x for peers, 3.8x for the wider US Software group, and a fair ratio of 3.8x, which points to meaningful valuation risk if sentiment cools.

When a stock trades that far above both its industry and fair ratio, you are essentially paying upfront for a lot of execution going right. The question is whether you are comfortable underwriting that kind of premium, or whether you would prefer names where the multiple has less air in it. See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Core Scientific Narrative

If parts of this story do not quite fit your view, or you would rather weigh the numbers yourself, you can build a custom thesis in just a few minutes, starting with Do it your way.

A great starting point for your Core Scientific research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one company, you could miss opportunities that fit your style even better, so keep building your watchlist while this research is fresh.

- Target resilient compounding potential by scanning our 51 high quality undervalued stocks that blend quality fundamentals with prices that still look reasonable.

- Protect your downside first by checking 85 resilient stocks with low risk scores focused on companies with more measured risk profiles.

- Get ahead of the crowd by reviewing our screener containing 24 high quality undiscovered gems before they sit on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.