A Look At Coterra Energy (CTRA) Valuation After Its Form 15 Deregistration Move

Coterra Energy CTRA | 0.00 |

Coterra Energy (CTRA) has moved to voluntarily deregister its common stock and several senior notes by filing Form 15 with the SEC, marking a material shift in its reporting and disclosure obligations for investors.

The share price has reacted sharply around these filings, with a 1-day share price return down 8.62% and a 7-day share price return down 7.97%. This follows a year-to-date share price return of 22.41% and a 1-year total shareholder return of 43.97%, suggesting that longer-term momentum has been stronger than the latest move.

If this shift in reporting status has you rethinking your energy exposure, it could be a good moment to broaden your search with 88 nuclear energy infrastructure stocks

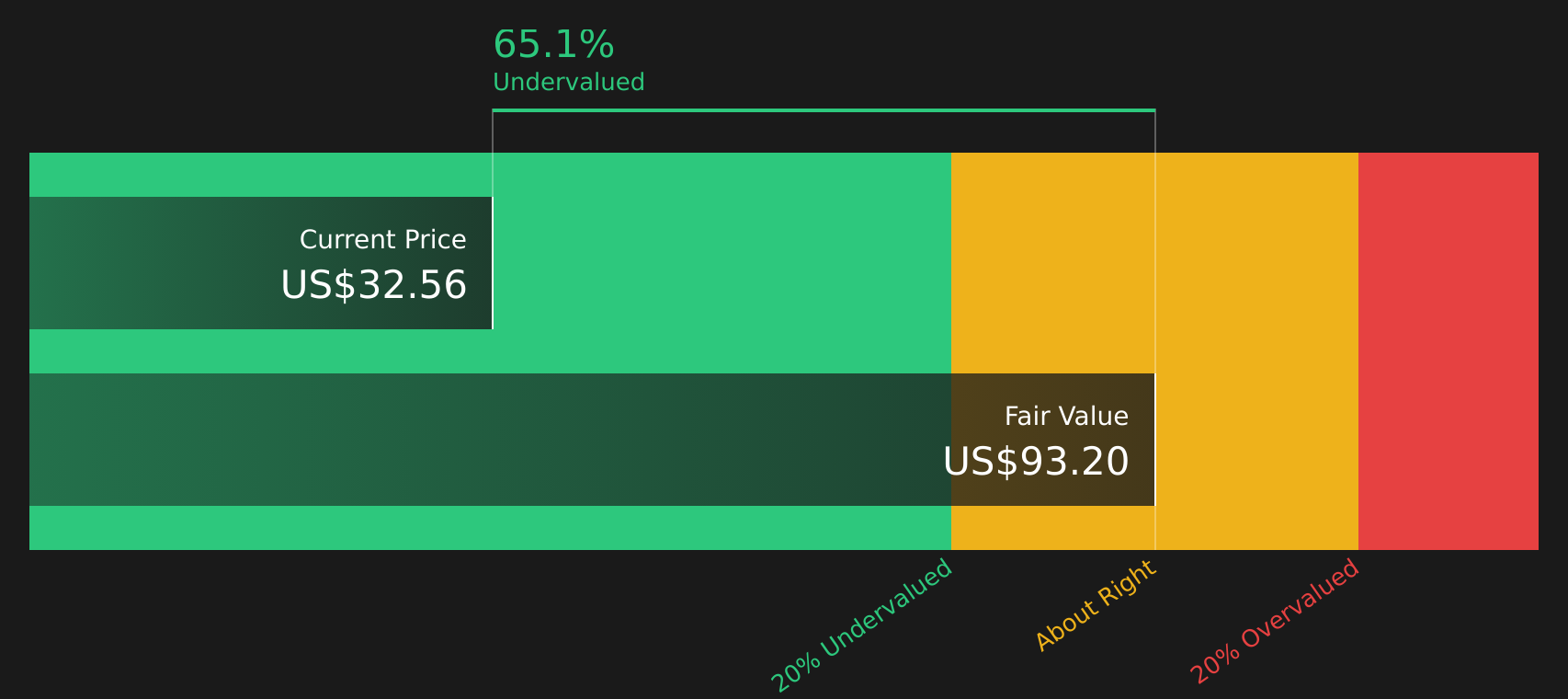

With the stock at US$32.56, trading at a discount to some intrinsic estimates and below the average analyst price target, investors may ask whether there is still value available or if the market is already pricing in potential future growth.

Most Popular Narrative: 27.4% Overvalued

The current fair value estimate in the most followed narrative, at $25.55, sits well below the last close at $32.56. This sets up a clear valuation gap for investors to judge, according to Bejgal.

In 3 years, Coterra is likely to solidify its position as a leading energy producer with enhanced capital efficiency and diversified revenue streams. By 5 years, the company could see robust earnings growth driven by the LNG market and efficient oil production.

Read the complete narrative. Read the complete narrative.

It may be useful to understand what kind of LNG driven revenue mix and margin profile would support that higher valuation path. The narrative focuses on improving efficiency, richer projects and a re rated profit multiple. The full set of assumptions is where the story becomes clear.

Result: Fair Value of $25.55 (OVERVALUED)

However, LNG market disruptions or tougher environmental rules in key regions could quickly challenge the earnings assumptions behind this narrative of 27.4% overvaluation.

Another View: Cash Flows Paint A Different Picture

The user narrative tags Coterra as 27.4% overvalued at a fair value of $25.55, yet our DCF model points in the opposite direction, with an estimated future cash flow value of $93.20 compared with the current $32.56 share price. That is a wide gap for you to weigh up, especially if you think cash flows tell the truer story.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Coterra Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between upside potential and meaningful concerns, it makes sense to act quickly and test the assumptions against your own data view using 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Coterra's story raised fresh questions, do not stop here. Broaden your watchlist with focused stock ideas that match the way you like to invest.

- Target steadier price behavior and sleep easier at night by scanning 67 resilient stocks with low risk scores that score well on resilience.

- Pursue long term compounding potential by reviewing screener containing 21 high quality undiscovered gems with strong fundamentals that are not on every investor's radar yet.

- Build a portfolio that can better handle shocks by concentrating on solid balance sheet and fundamentals stocks screener (46 results) backed by healthier financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.