A Look At Coterra Energy (CTRA) Valuation After Recent Share Price Pullback And Mixed Fair Value Signals

Coterra Energy CTRA | 0.00 |

Performance snapshot and why Coterra is on investors’ radar

Coterra Energy (CTRA) has drawn attention after a period where the stock shows a 1 day return of 0.09% and a 7 day return of 0.08%, with year to date performance of 22.41%.

Over the past month the stock shows a 2.69% decline, while the past 3 months reflect a 6.2% gain. This has prompted investors to reassess how recent share price moves line up with the company’s fundamentals.

Recent trading has been choppy, with the latest 1 day share price return of an 8.62% decline and a 7 day share price return of a 7.97% decline. This contrasts with a much stronger 22.41% year to date share price return and a 43.97% 1 year total shareholder return, suggesting longer term momentum has been stronger than the very recent pullback.

If this kind of move has you thinking about what else is moving in energy related areas, it could be a useful moment to scan 36 power grid technology and infrastructure stocks

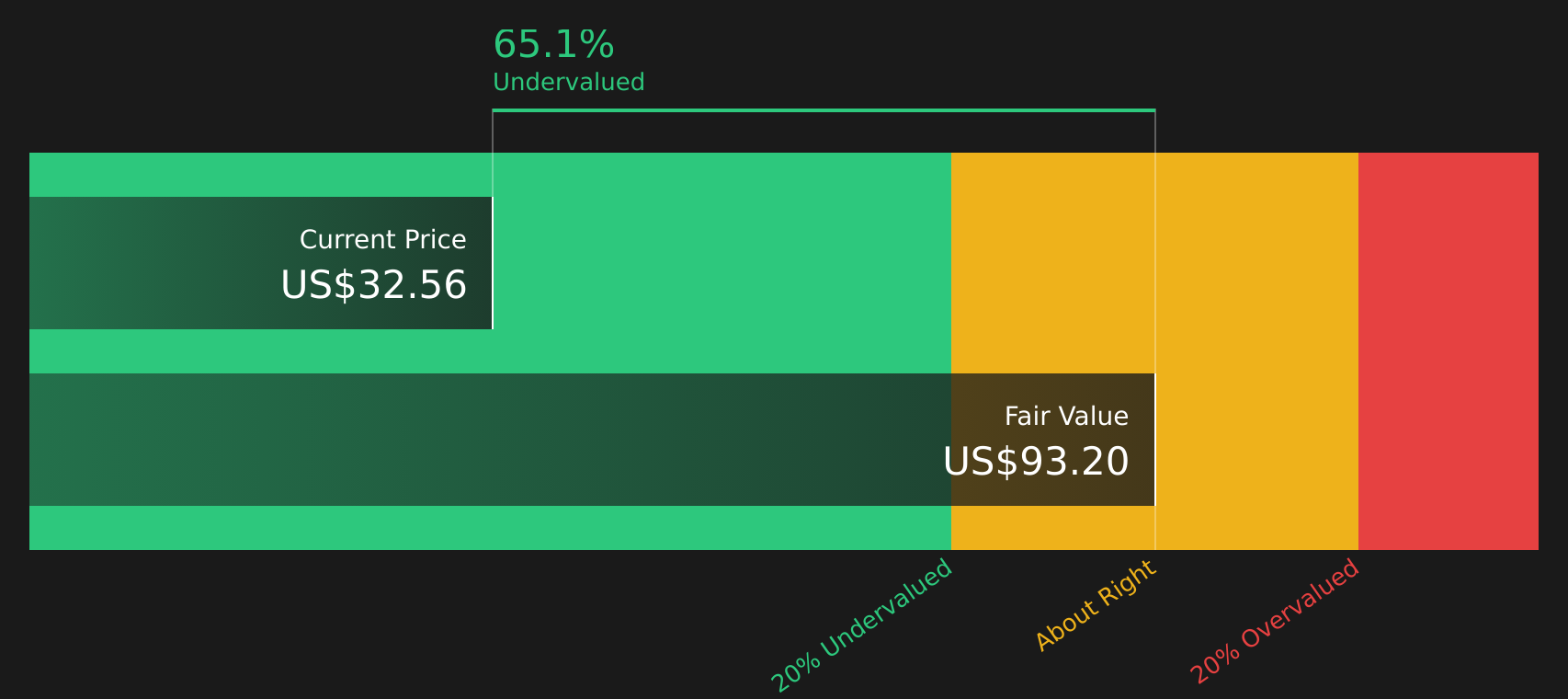

With Coterra posting steady revenue and net income growth, trading at $32.56 and sitting at a reported 65.07% intrinsic discount, investors are asking whether this stock is undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 27.4% Overvalued

According to the narrative by Bejgal, the current share price of $32.56 sits above an estimated fair value of $25.55, which is built on a detailed view of Coterra Energy’s project pipeline and earnings potential.

In 3 years, Coterra is likely to solidify its position as a leading energy producer with enhanced capital efficiency and diversified revenue streams. By 5 years, the company could see robust earnings growth driven by the LNG market and efficient oil production. Over 10 years, its extensive inventory and focus on innovation position it for sustainable long-term growth.

Want to see how LNG contracts, margin assumptions and long term production plans feed into that fair value? The key drivers sit inside this narrative, including how future earnings power and profitability are treated against today’s price.

Result: Fair Value of $25.55 (OVERVALUED)

However, LNG market disruptions or tougher environmental rules in regions like New Mexico could quickly challenge the assumptions behind Coterra’s current overvaluation narrative.

Another view on value: DCF flips the script

Bejgal’s narrative points to a fair value of $25.55 and a 27.4% overvaluation, but our DCF model points the other way. With an estimated future cash flow value of $93.20 per share, Coterra screens as deeply undervalued. This raises a simple question: which story do you trust more, the cash flows or the narrative multiple?

Next Steps

With such mixed views on Coterra’s value, it helps to look past the headlines and weigh the trade off between concern and optimism yourself. To see how those risks and potential rewards compare side by side, check out the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Coterra has caught your attention, do not stop there. Fresh opportunities often sit just beyond your current watchlist, and you do not want to overlook them.

- Target resilience by checking out companies that screen well on balance sheet strength and core fundamentals through the solid balance sheet and fundamentals stocks screener (44 results).

- Hunt for potential mispricings by reviewing the 51 high quality undervalued stocks that combine quality metrics with valuations that may appeal to value focused investors.

- Spot less crowded opportunities by scanning the screener containing 23 high quality undiscovered gems that pair solid fundamentals with relatively low investor attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.