A Look At Coupang (CPNG) Valuation After Major Data Breach And Growing Legal Scrutiny

Coupang, Inc. Class A CPNG | 21.55 21.33 | +0.28% -1.02% Pre |

Why Coupang (CPNG) is back in focus for investors

Coupang (CPNG) is back under the spotlight after confirming a massive data breach affecting over 33 million customers, along with fresh disclosures of additional compromised records and a wave of securities class action lawsuits.

The data breach, regulatory probe and cluster of class action filings appear to be weighing on sentiment. Coupang’s 30 day share price return shows a decline of 20.34% and its year to date share price return reflects a decline of 24.43%. Its 3 year total shareholder return of 7.55% contrasts with a 1 year total shareholder return decline of 25.26%, suggesting recent momentum has faded after earlier gains.

If recent volatility around Coupang has you thinking about where else growth and risk might balance out differently, it could be a good time to scan 22 top founder-led companies for potential new ideas.

With Coupang shares down sharply over the past year but trading at what some see as a meaningful discount to analyst targets, you have to ask yourself: is this a reset that opens a buying window, or is the market already marking down future growth?

Most Popular Narrative: 51.2% Undervalued

At a last close of $17.66 versus an implied fair value of about $36.23, the most followed Coupang narrative paints a very different picture to recent price action and sets up some punchy growth assumptions.

The scaling of new verticals, such as Fulfillment and Logistics by Coupang (FLC), Coupang Eats, and Coupang Play, is expanding Coupang's total addressable market, diversifying revenue streams, and providing additional pathways for high-margin and recurring revenue growth.

Want to see what powers that valuation jump? This narrative leans heavily on compounded earnings growth, richer margins, and a future earnings multiple usually reserved for market favorites. Curious how those moving parts stack together to reach that fair value line?

Result: Fair Value of $36.23 (UNDERVALUED)

However, there is still a real risk that sustained losses in newer markets or higher ongoing logistics and technology costs could pressure margins and challenge those upbeat assumptions.

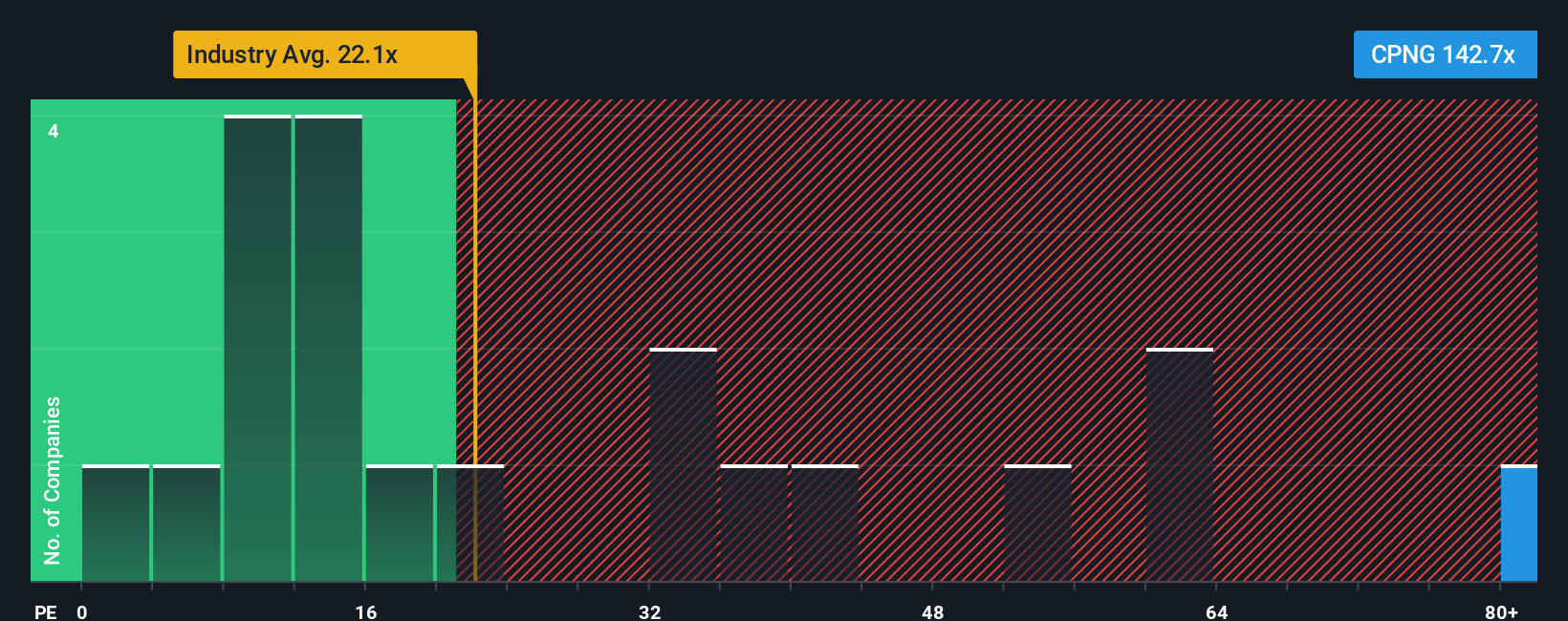

Another Angle: Earnings Multiple Sends a Different Signal

That 51.2% discount to fair value sounds appealing, but the current P/E of 82.7x is far higher than both the North American Multiline Retail average at 18.3x and the company’s own fair ratio of 36.6x. Is this a rare opportunity or just a lot of optimism priced in?

Build Your Own Coupang Narrative

If you look at these numbers and reach a different conclusion, or just prefer to stress test the assumptions yourself, you can build a custom view of Coupang in a few minutes, then Do it your way.

A great starting point for your Coupang research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are weighing what to do with Coupang next, do not stop here. Broaden your watchlist and give yourself more options with a few focused stock lists.

- Target quality at a discount by scanning 51 high quality undervalued stocks and see which companies pair stronger fundamentals with prices that lag behind their assessed worth.

- Prioritise resilience by reviewing 85 resilient stocks with low risk scores so you can spot businesses with lower assessed risk profiles before the crowd pays attention.

- Spot tomorrow’s potential standouts early with our screener containing 24 high quality undiscovered gems and see which underfollowed names already post solid financial indicators.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.