A Look At Datadog (DDOG) Valuation After Its Earnings Beat And AI Focused Growth Outlook

Datadog DDOG | 120.36 | +1.42% |

Datadog (DDOG) is back in focus after its fourth quarter and full year 2025 earnings beat market expectations on both revenue and earnings, paired with upbeat 2026 revenue guidance and a growing emphasis on AI driven products.

The latest earnings beat and upbeat 2026 revenue guidance come after a volatile stretch, with a 12.1% 7 day share price return, a 30.5% 90 day share price decline, and a 56.5% 3 year total shareholder return that signals longer term momentum.

If Datadog's AI story has caught your attention, it might be a good time to scan other opportunities in the theme using our screener of 57 profitable AI stocks that aren't just burning cash.

With shares sliding 30.5% over 90 days but still carrying a premium growth profile, the key question now is whether Datadog is temporarily out of favor or whether the market already reflects years of future progress.

Most Popular Narrative: 39.9% Undervalued

With Datadog last closing at $125.20 against a most-followed fair value estimate of about $208.49, the valuation gap is wide enough to attract close attention, especially given the detailed growth and profitability roadmap behind that number.

Ongoing product innovation (e.g., autonomous AI agents, enhanced security modules, expanded log and data observability) is increasing platform breadth and relevance, providing cross-selling opportunities and driving higher average revenue per user and net retention rate, which in turn improves recurring revenue predictability and gross margins.

Curious what kind of revenue path and margin lift would need to sit behind a fair value this far above today’s price? The narrative leans on robust top line expansion, higher profitability and a rich future earnings multiple that together anchor that $208.49 figure. If you want to see exactly how those assumptions stack up across the next few years, the full narrative lays it out in black and white.

Result: Fair Value of $208.49 (UNDERVALUED)

However, this upbeat narrative can be tested quickly if competition forces pricing pressure across observability tools or if large AI native customers pull back on usage.

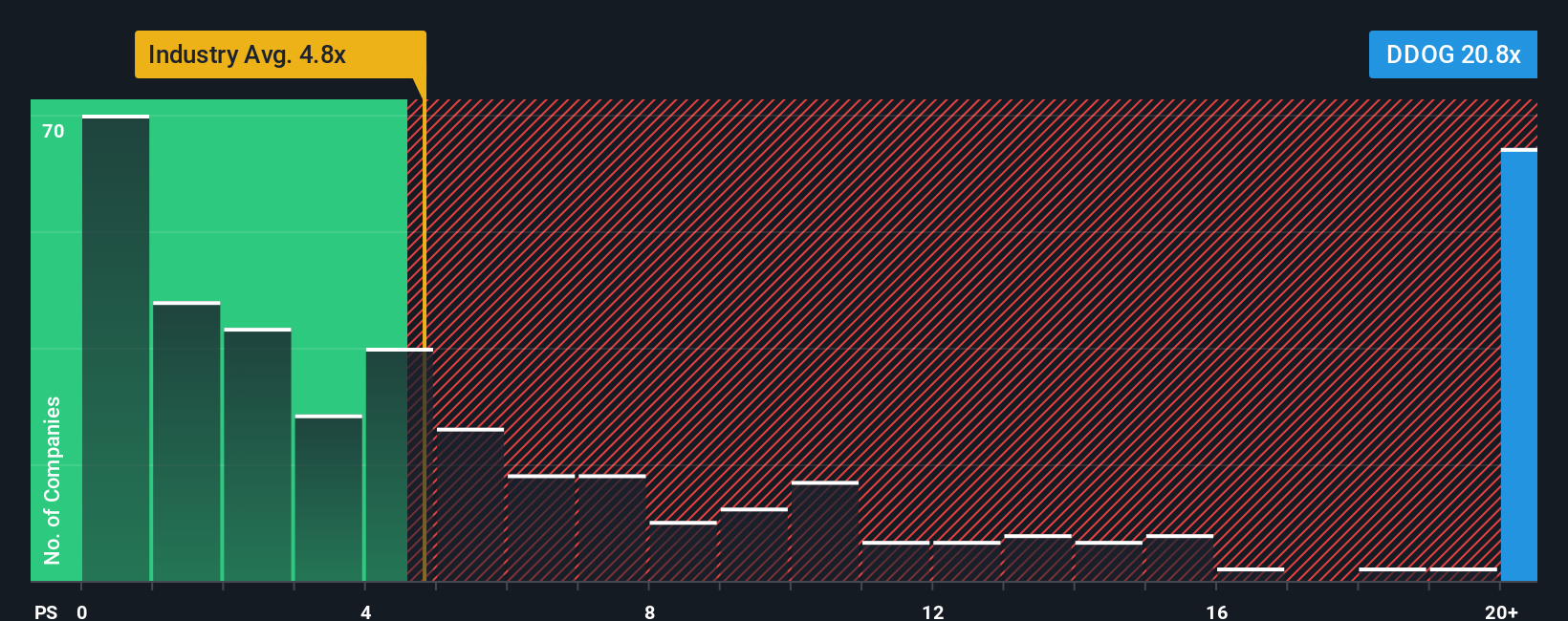

Another View: High P/S Keeps Expectations Loaded

That 39.9% gap to our fair value sits alongside a very full P/S of 12.9x, compared with 3.6x for the US Software industry, 6.9x for peers, and a fair ratio of 11.5x. The market is already paying up, so is this a margin of safety or a margin of error?

Build Your Own Datadog Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a fresh Datadog narrative in just a few minutes. Start with Do it your way.

A great starting point for your Datadog research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Datadog has sharpened your appetite for opportunities, do not stop here. Use the Simply Wall Street Screener to round out your watchlist with targeted ideas.

- Spot potential value opportunities early by checking out 53 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect them.

- Prioritize resilience by scanning 85 resilient stocks with low risk scores so you know which companies score well on stability before the next bout of volatility hits.

- Get ahead of the crowd by reviewing our screener containing 23 high quality undiscovered gems where lesser known names with strong underlying metrics might be waiting for attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.