A Look At Delek Logistics Partners (DKL) Valuation After Recent Unit Buyback And Tyler Tank Sale

Delek Logistics DKL | 0.00 |

Delek Logistics Partners (DKL) is back in focus after repurchasing 243,075 common units from Delek US Holdings for US$10 million, together with a US$19 million Tyler refinery tank sale that was settled in units.

The unit repurchase and earlier US$800 million senior notes issuance sit against a steady backdrop, with the latest US$51.24 share price reflecting a 9.02% year to date share price gain and 32.40% one year total shareholder return. This suggests positive long term momentum despite some recent short term softness.

If this kind of capital activity has you thinking more broadly about energy infrastructure, it could be worth scanning for other power grid and pipeline players through our 35 power grid technology and infrastructure stocks.

With units trading near a US$51.40 analyst target, steady revenue and net income growth, and an indicated intrinsic discount, the key question is whether DKL is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 30% Undervalued

With Delek Logistics Partners trading at $51.24 against a most followed narrative fair value of $51.40, the story hinges more on assumptions than on a wide price gap.

The full commissioning and expected ramp to capacity of the new Libby 2 gas plant in the Delaware Basin, along with associated investments (amine unit and AGI wells), positions Delek Logistics to capitalize on rising energy demand and stable domestic energy infrastructure needs, likely boosting gathering and processing volumes, EBITDA, and revenue growth.

Curious what kind of future revenue path, profit margin lift, and valuation multiple are baked into that fair value line? The narrative leans on a detailed earnings build, a specific profit margin step up, and a tighter range of outcomes than the headline price target spread suggests.

Result: Fair Value of $51.40 (UNDERVALUED)

However, that hinges on execution, and slower than expected Libby 2 ramp up or higher leverage costs could quickly challenge the current fair value narrative.

Another Way to Look at Valuation

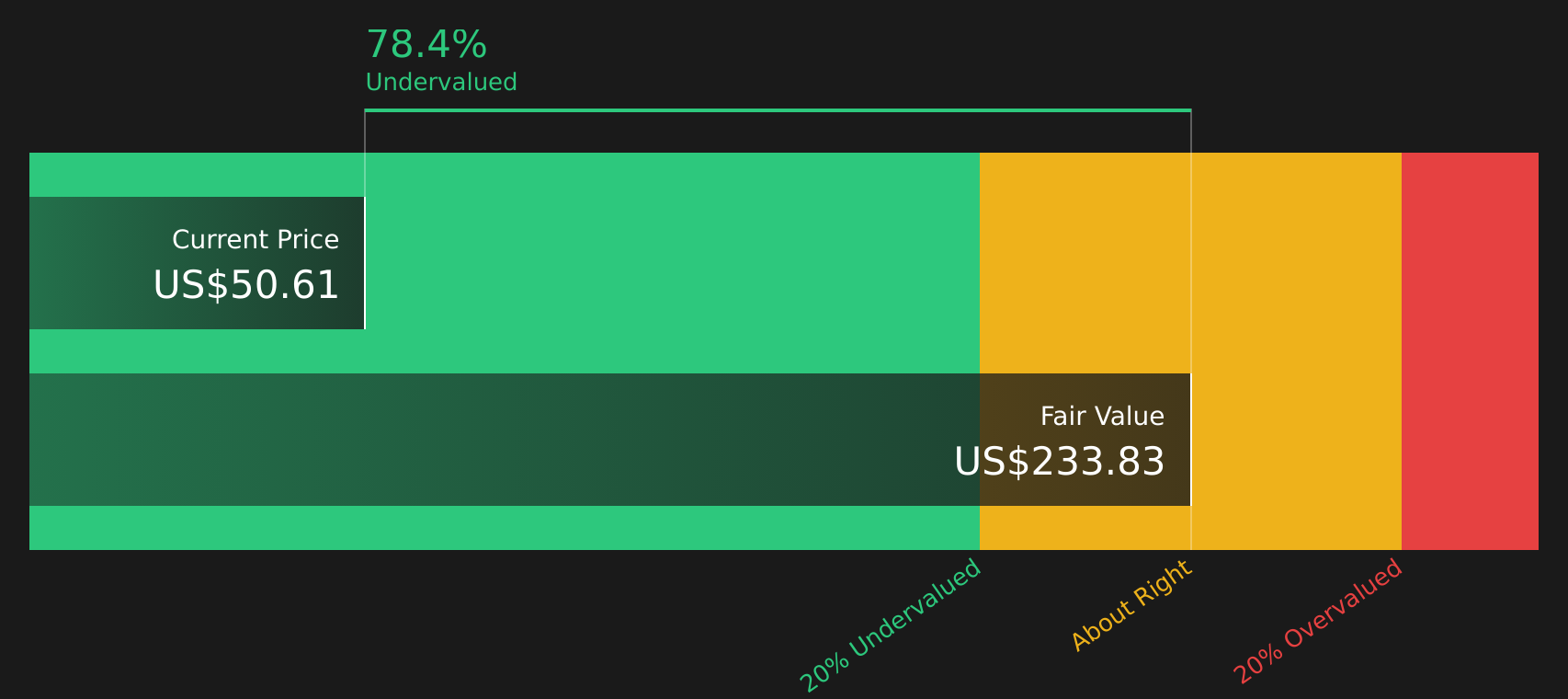

The narrative fair value of $51.40 suggests Delek Logistics Partners is only slightly undervalued, but the SWS DCF model presents a very different perspective. Units are trading well below its estimate of future cash flow value at $235.46. Which signal do you rely on when they differ this much?

Next Steps

If this combination of potential benefits and risks leaves you uncertain, this may be a good time to review the data yourself and stress test your view against the 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If DKL has sharpened your focus, do not stop here; broaden your watchlist with other clear, data backed setups that could suit your goals.

- Target stronger income potential by scanning companies that offer resilient payouts through our 10 dividend fortresses.

- Zero in on quality at a reasonable price by reviewing companies flagged as having attractive valuations with the 46 high quality undervalued stocks.

- Protect your downside by concentrating on companies assessed to have sturdier finances using the solid balance sheet and fundamentals stocks screener (46 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.