A Look At Diamondback Energy’s Valuation As Mixed Returns Stir Investor Interest

Diamondback Energy, Inc. FANG | 0.00 |

Why Diamondback Energy Is On Investors’ Radar Today

Diamondback Energy (FANG) is drawing fresh attention after recent share moves, with the stock showing a negative 1 day return and a mixed pattern across the past week and month.

While the latest 1 day share price return of 2.38% and 7 day share price return of 7.39% point to cooling near term momentum, the 25.01% year to date share price return and 43.66% 1 year total shareholder return show the longer term trend has been stronger.

If recent moves in Diamondback Energy have you thinking about other opportunities in energy infrastructure, this is a good time to scan the market using the 36 power grid technology and infrastructure stocks

With Diamondback trading at a discount to both analyst targets and some intrinsic estimates, yet already carrying strong multi year returns, investors may question whether this still represents a buying opportunity or if markets are already pricing in future growth.

Most Popular Narrative: 14.5% Undervalued

The most followed narrative puts Diamondback Energy’s fair value at $222.70, compared with the last close of $190.44, framing the stock as underpriced against those assumptions.

Ongoing consolidation in the Permian Basin, with Diamondback positioned as the "consolidator of choice" due to its industry-best integration, low cost structure, and ability to deliver synergies from recent large acquisitions (e.g., Double Eagle, Endeavor), supports future growth in scale, cost savings, and higher EBITDA margins.

Want to see what is built into that valuation gap? The narrative leans on firm revenue expectations, rising margins and a richer profit multiple in later years.

Result: Fair Value of $222.70 (UNDERVALUED)

However, rising operating costs in the Permian and the shift toward secondary drilling zones could pressure margins and challenge the assumptions behind that 14.5% undervaluation gap.

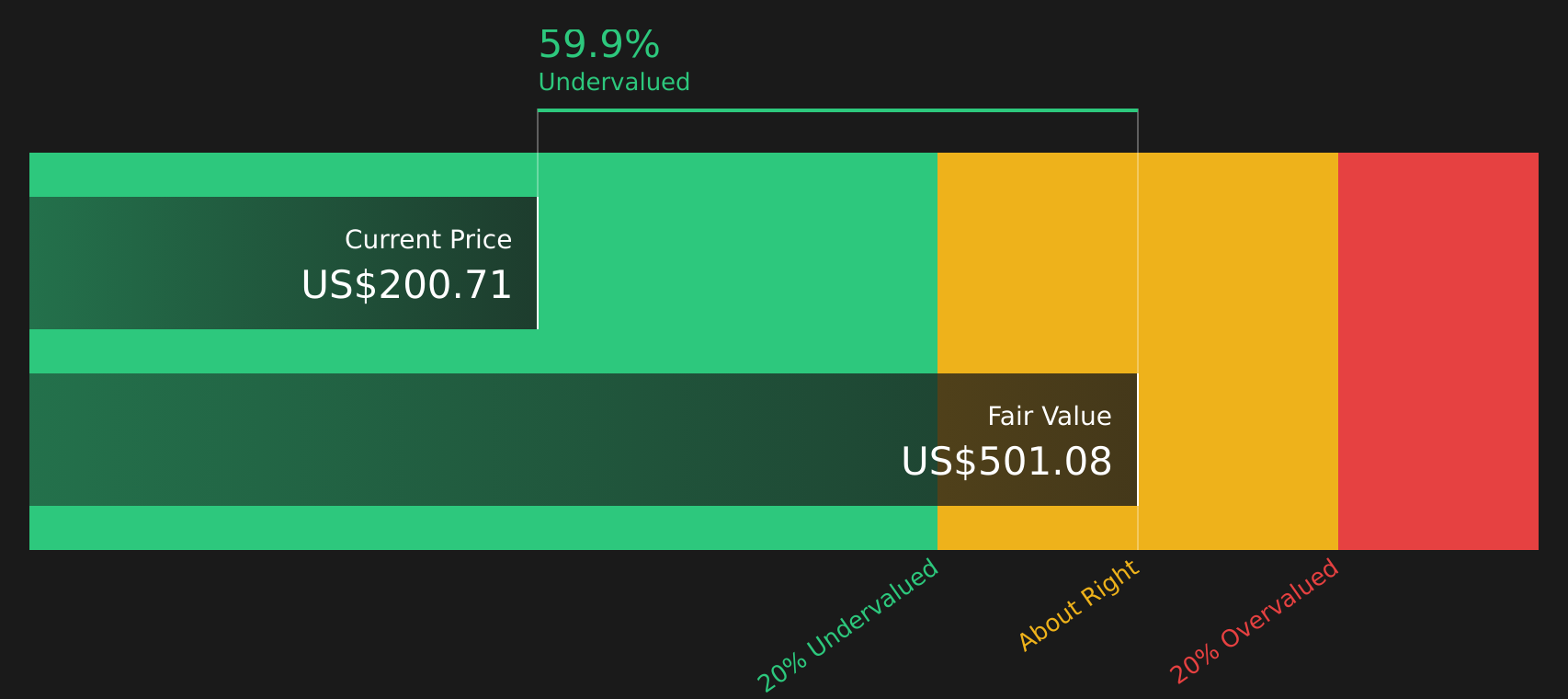

Another Angle On Valuation

The earlier view relies on fair value at $222.70 and a 14.5% undervaluation, but the SWS DCF model points to a much larger gap, with Diamondback Energy at $190.44 versus an estimated future cash flow value of $491.68. That is a wide spread. Which set of assumptions do you trust more?

Next Steps

With mixed signals on value and future returns, sentiment is clearly divided, so this is a good moment to review the underlying data yourself and weigh both sides. To sharpen that view, make sure you understand the 2 key rewards and 4 important warning signs.

Looking For More Investment Ideas?

If you stop with just one stock, you risk missing other opportunities that better match your goals, risk comfort and income needs.

- Target potential income powerhouses by checking out companies in the 12 dividend fortresses and see which payouts might line up with your cash flow goals.

- Spot potential mispriced opportunities by reviewing the 51 high quality undervalued stocks and compare how their fundamentals stack up against what the market is currently willing to pay.

- Focus on financial resilience by scanning the solid balance sheet and fundamentals stocks screener (44 results) and see which companies pair healthier balance sheets with solid underlying businesses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.