A Look At Digital Realty Trust (DLR) Valuation After BofA Downgrade On AI Demand And Development Concerns

Digital Realty Trust, Inc. DLR | 181.69 | +0.69% |

BofA Securities recently downgraded Digital Realty Trust (DLR) from Buy to Neutral, citing slower capture of AI related demand and development deals concentrating in markets where the data center REIT has less exposure.

The downgrade comes after a mixed stretch for the stock, with a 2.8% 30 day share price return, an 8.2% 90 day share price decline, and a 5.3% 1 year total shareholder return loss, contrasting with a 65.1% 3 year total shareholder return.

If this AI driven data center story has your attention, it could be a good moment to widen your research and check out high growth tech and AI stocks for more ideas.

With Digital Realty now trading at a discount to both analyst targets and some intrinsic estimates, yet facing questions around AI focused growth and market positioning, investors may be wondering whether this pullback represents a potential opportunity or whether the market is already fully reflecting what comes next.

Most Popular Narrative: 20.2% Undervalued

Digital Realty Trust's most followed narrative pegs fair value at about $197.78, compared with the last close of $157.87, framing a clear valuation gap for investors to weigh.

Increasing data center revenue, supported by robust leasing activity, renewal leases with fixed escalators, and a focus on AI and cloud infrastructure demand, forecasts continued growth in adjusted EBITDA and FFO, enhancing profitability.

Curious how a company with projected revenue growth, lower future margins and a much higher implied earnings multiple still lands on this fair value? The narrative leans heavily on contracted backlog, a large development pipeline and fee income from capital partners. Want to see exactly how those moving parts translate into the valuation gap?

Result: Fair Value of $197.78 (UNDERVALUED)

However, record leasing and AI demand could still disappoint if new supply in key U.S. markets outpaces customer commitments, or if power constraints delay turning that backlog into revenue.

Another View: Valuation Ratios Send A Different Signal

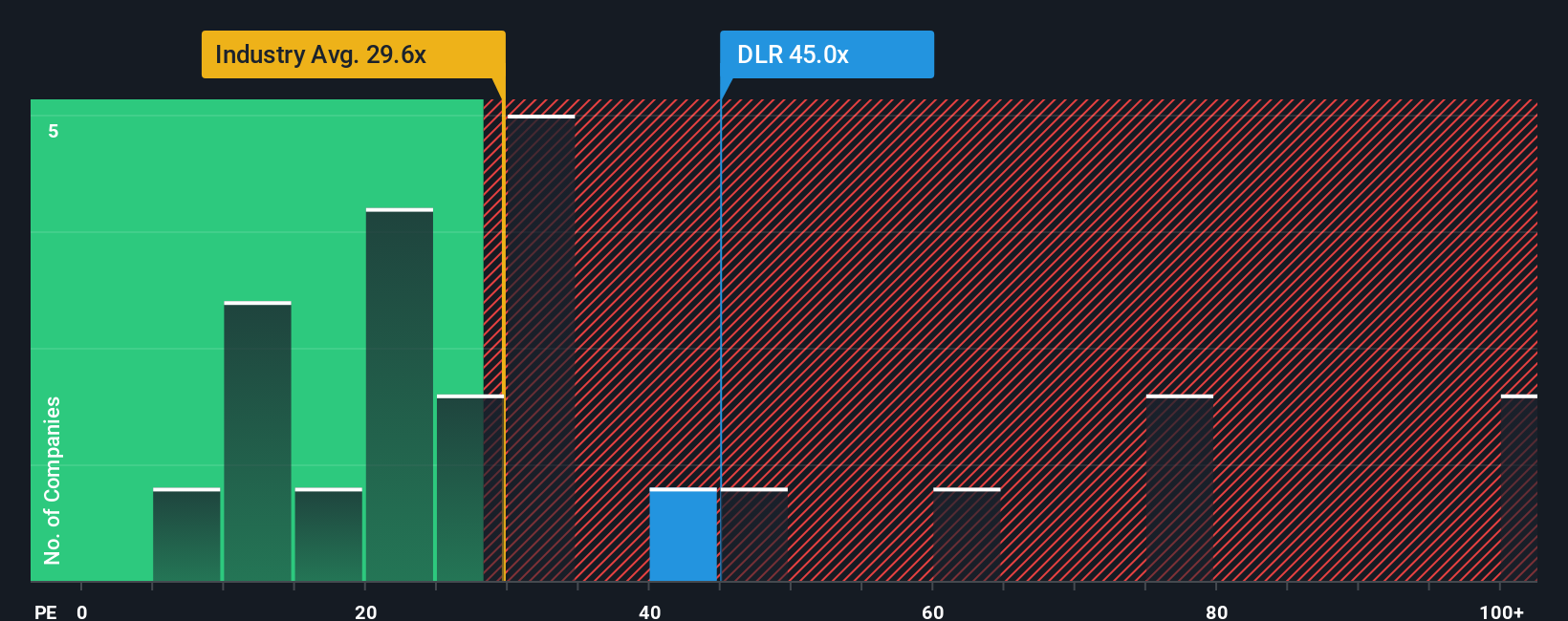

That 20.2% “undervalued” fair value hinges on forward growth and margin assumptions, but the current P/E of 39.9x tells a tougher story. It sits above the US Specialized REITs average of 28.1x, the peer average of 34.7x, and the fair ratio of 30.7x.

In plain terms, the share price currently bakes in a richer earnings multiple than both peers and the level our fair ratio suggests the market could move toward. This adds valuation risk even if cash flow based models point to upside. Which signal do you think should carry more weight right now?

Build Your Own Digital Realty Trust Narrative

If you look at the numbers and come to a different conclusion, or prefer to test your own assumptions, you can build a custom valuation story in just a few minutes using Do it your way.

A great starting point for your Digital Realty Trust research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Digital Realty has sparked your interest, do not stop here. Broaden your watchlist now so you are not looking back wishing you had acted sooner.

- Hunt for underappreciated opportunities where expectations might be lower than potential using these 883 undervalued stocks based on cash flows as a starting point for fresh names.

- Zero in on companies related to AI by scanning these 25 AI penny stocks and see which businesses are already aligning with this theme.

- Target income focused ideas by checking these 12 dividend stocks with yields > 3%, where yields above 3% could add a different source of return to your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.