A Look At Digital Realty Trust’s Valuation As AI Demand And 2026 Guidance Support Record Bookings

Digital Realty Trust, Inc. DLR | 181.69 | +0.69% |

Digital Realty Trust (DLR) has put fresh numbers on the table, reporting fourth quarter and full year 2025 results, along with new 2026 guidance, record bookings, and updates tied to AI and cloud demand.

The recent earnings release, record bookings, and expanded AI-focused data center footprint appear to sit behind the 10.6% 1 month share price return and strong 3 year total shareholder return of 70.3%, with momentum still building.

If this AI and data infrastructure story has your attention, it could be a good time to look at other infrastructure names powering the trend, starting with 34 AI infrastructure stocks.

With DLR up 10.6% in a month and trading at a reported intrinsic discount of about 29%, plus an 11% gap to the average analyst target, you have to ask: is there still a window here, or is the market already baking in the next leg of AI driven growth?

Most Popular Narrative: 58.1% Overvalued

According to the most followed narrative, Digital Realty Trust's fair value of $110.45 sits well below the last close of $174.57, which puts a clear question mark over how much of the AI and cloud story is already reflected in the price.

Digital Realty should be a leading global provider of AI-ready and hyperscale data centers, with stronger cloud partnerships, a global footprint, and higher-margin interconnection services.

Read the complete narrative. Read the complete narrative.

Curious what kind of revenue growth, margin profile, and future earnings multiple are built into that fair value? The narrative leans on steady expansion in AI focused workloads, richer interconnection income, and a future valuation framework that might surprise you once you see the assumptions laid out side by side.

Result: Fair Value of $110.45 (OVERVALUED)

However, there are clear pressure points, including higher interest costs for a heavily leveraged REIT and the risk that hyperscalers shift more capacity in house.

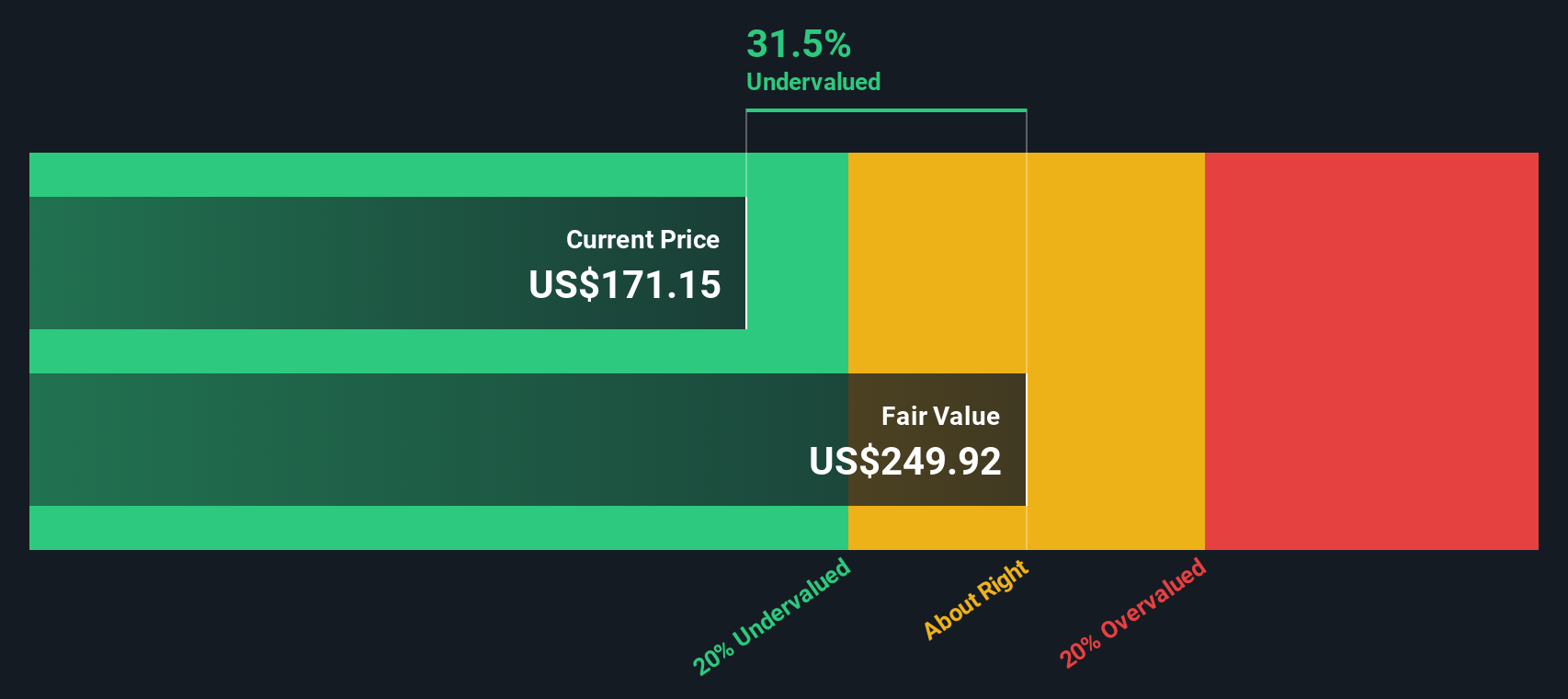

Another View: Cash Flows Tell a Different Story

That 58.1% overvalued fair value of $110.45 is based on earnings assumptions, but our DCF model points in the opposite direction. On this view, DLR at $174.57 is trading at a 29.2% discount to an estimated future cash flow value of $246.67. This raises a simple question: which lens do you trust more when cash flows and earnings disagree this much?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Digital Realty Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Digital Realty Trust Narrative

If you see the numbers differently or prefer to test your own assumptions, you can pull the data together, stress test the story, then Do it your way and put your version on the record.

A great starting point for your Digital Realty Trust research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If you are weighing what to do next, do not stop at a single stock. Use the Simply Wall St screener to pressure test fresh ideas and keep your watchlist sharp.

- Target value opportunities that pair quality with a discount by scanning our 51 high quality undervalued stocks and see which names meet your standards.

- Protect your downside first by focusing on resilience with the 85 resilient stocks with low risk scores, highlighting companies that score well on risk metrics.

- Get ahead of the crowd by reviewing our screener containing 24 high quality undiscovered gems, where smaller, less followed companies with solid fundamentals might not yet be widely discussed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.