A Look At Dollar General (DG) Valuation As Expansion And Delivery Plans Draw Fresh Attention

Dollar General Corporation DG | 119.74 | +2.19% |

Dollar General (DG) is drawing fresh attention after announcing plans for about 4,730 real estate projects in fiscal 2026, alongside an expanded delivery push and growing interest from technical traders.

The recent real estate expansion plans and delivery push come on top of a sharp run in the shares, with a 90 day share price return of 49.14% and a 1 year total shareholder return of 116.69%. However, the 3 year and 5 year total shareholder returns remain negative overall, which suggests momentum has strengthened only relatively recently.

If this Dollar General news has you thinking about where else growth stories might emerge, it could be a good moment to scan our list of 23 top founder-led companies as potential next ideas.

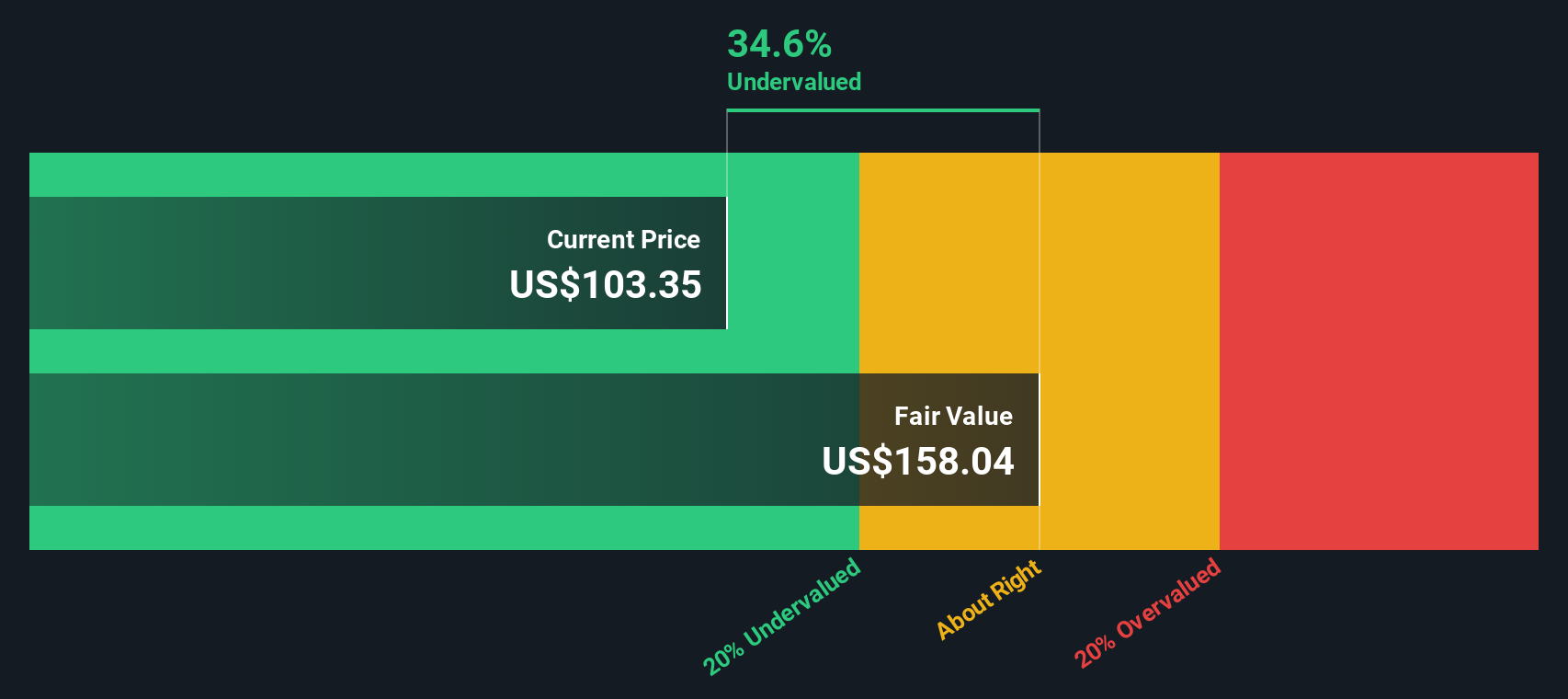

With the shares up triple digits over 1 year and trading around an implied 13% discount to some intrinsic value estimates, you have to ask: Is Dollar General still mispriced, or are investors already betting on future growth?

Most Popular Narrative: 10.5% Overvalued

Dollar General last closed at $153.84 compared with a widely followed fair value estimate of $139.25. This frames the current debate around how much future growth is already priced in.

Rapid scaling of digital initiatives including same-day delivery partnerships (DoorDash, Uber Eats), in-house DG delivery, and the DG Media Network positions Dollar General to capture incremental market share and drive higher-margin omni-channel revenue streams, boosting both sales and earnings over the long term.

Want to see what kind of revenue path and profit profile could support that valuation gap? The narrative leans on steady growth, firmer margins, and a richer future earnings multiple to make the numbers work.

Result: Fair Value of $139.25 (OVERVALUED)

However, that story can crack if rural store saturation starts to bite, or if labor and operating costs squeeze margins harder than expected, limiting the payoff from growth projects.

Another View: DCF Points the Other Way

Here is the twist. While the popular narrative frames Dollar General as about 10.5% overvalued versus a US$139.25 fair value, our DCF model suggests the shares at US$153.84 trade around 12.9% below an estimated future cash flow value of US$176.67. Which story do you think is closer to reality?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dollar General for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Dollar General Narrative

If you look at the numbers and come to a different conclusion, or simply want to test your own assumptions, you can build a custom Dollar General story in just a few minutes, starting with Do it your way.

A great starting point for your Dollar General research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Dollar General has sharpened your focus, do not stop here. Broaden your watchlist with a few targeted stock ideas that fit different roles in a portfolio.

- Target potential upside by scanning screener containing 23 high quality undiscovered gems that combine solid fundamentals with relatively low market attention.

- Strengthen your core holdings by reviewing companies in the solid balance sheet and fundamentals stocks screener (45 results) that prioritize financial resilience.

- Lock in reliable cash flow potential by checking out income ideas across 12 dividend fortresses that meet your yield preferences.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.