A Look At Dorchester Minerals (DMLP) Valuation After Higher Institutional Interest And A Dividend Increase

Dorchester Minerals, L.P. DMLP | 0.00 |

Dorchester Minerals (DMLP) is back on investor radars after GraniteShares Advisors LLC lifted its stake by 34.2% and the partnership raised its quarterly cash distribution to $0.7557 per unit.

The higher quarterly cash distribution and increased institutional interest have arrived while the unit price has climbed, with a 30 day share price return of 4.0% and a 90 day share price return of 24.6%, alongside a 1 year total shareholder return of 14.5% and a 5 year total shareholder return of about 2.4x.

If this kind of income focused commodity exposure interests you, it may be worth widening your search using our screener of 28 elite gold producer stocks

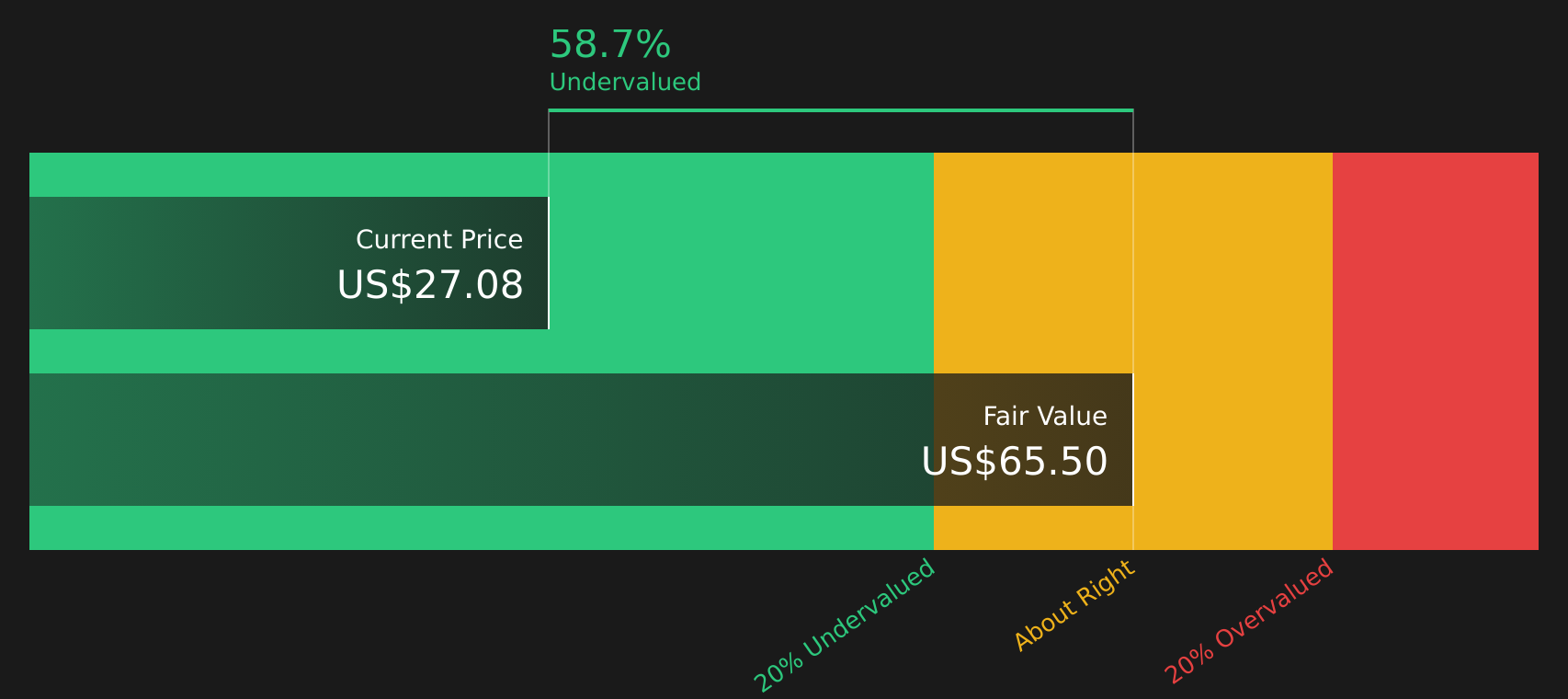

With units trading at $27.96, a value score of 2 and an estimated intrinsic discount of about 62%, the key question for you is simple: is Dorchester Minerals still undervalued, or is the market already pricing in future growth?

Preferred P/E of 24.4x: Is it justified?

Dorchester Minerals currently trades on a P/E of 24.4x, which sits above both the US Oil and Gas industry average of 15.6x and its peer average of 24.2x, even though the SWS DCF model suggests the units trade at a 62.2% discount to an estimated future cash flow value of $74 per unit.

The P/E multiple tells you how much investors are paying today for each dollar of current earnings. This tends to matter a lot for mature, income focused partnerships like DMLP, where growth visibility is limited and most of the return can come from distributions. A higher P/E can reflect confidence that current earnings are sustainable or that the income stream is attractive enough to justify paying more for each dollar of profit.

Here, there are some tensions for you to weigh. On one side, earnings have grown by 8.1% per year over the past 5 years and the company reports high quality earnings, with a solid 18.8% Return on Equity that sits just below the 20% threshold used as a high bar. On the other side, earnings fell 38.1% over the past year and net profit margins moved from 57.7% to 37.6%. This means the current multiple rests on a year where profitability has already compressed, while the units still look expensive relative to both the industry P/E of 15.6x and the peer average of 24.2x.

Against that backdrop, the SWS DCF model points to a fair value of $74 per unit compared to the last close at $27.96. This is based on projected future cash flows from the existing royalty and net profits interests and discounting them back to today. That approach can be useful for a royalty partnership like Dorchester Minerals because cash flows are closely tied to underlying production and commodity price assumptions rather than heavy reinvestment plans. This means changes in volumes, pricing or costs can have a direct impact on estimated fair value.

Result: Price-to-Earnings of 24.4x (OVERVALUED)

However, the story could change quickly if commodity prices soften or if production from Dorchester Minerals royalty properties and net profits interests falls below expectations.

Another View: Cash Flows Tell a Different Story

While the current 24.4x P/E suggests Dorchester Minerals trades at a premium to the US Oil and Gas industry, the SWS DCF model points in the opposite direction, indicating the units trade at about a 62% discount to an estimated future cash flow value of $74 per unit. For you, that sets up a clear question: is the earnings multiple too rich, or are the cash flow assumptions too cautious?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dorchester Minerals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With both risks and rewards in play, this story is not one to sit on for long. Review the numbers, stress test your own assumptions, and weigh the 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If Dorchester Minerals is on your radar, do not stop there. Use targeted stock lists to uncover more opportunities that might fit your income and risk preferences.

- Target potential mispricings by scanning companies that look attractively valued on multiple checks through the 62 high quality undervalued stocks.

- Strengthen your income stream by reviewing businesses that meet strict yield and resilience criteria using the 13 dividend fortresses.

- Cut through the noise and focus on financially robust companies by checking the solid balance sheet and fundamentals stocks screener (40 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.