A Look At Dow (DOW) Valuation After Loss-Making Earnings And Renewed Cyclicals Interest

Dow, Inc. DOW | 38.84 38.84 | -0.82% 0.00% Pre |

Dow (DOW) is back in focus after its recent quarterly earnings showed a net loss for both the fourth quarter and full year, alongside fresh commentary from a high profile television analyst on cyclicals.

That earnings update, combined with the completed share repurchase program, has coincided with strong recent momentum, with a 30 day share price return of 27.61% and a 90 day share price return of 51.49%, even though the 1 year total shareholder return is a 6.52% decline and the 3 year total shareholder return is a 32.80% decline. This suggests a sharp rebound in sentiment after a weaker stretch for long term holders.

If cyclical materials names like Dow are back on your radar, it could be a moment to scan beyond chemicals and look at 24 power grid technology and infrastructure stocks as another angle on real economy exposure.

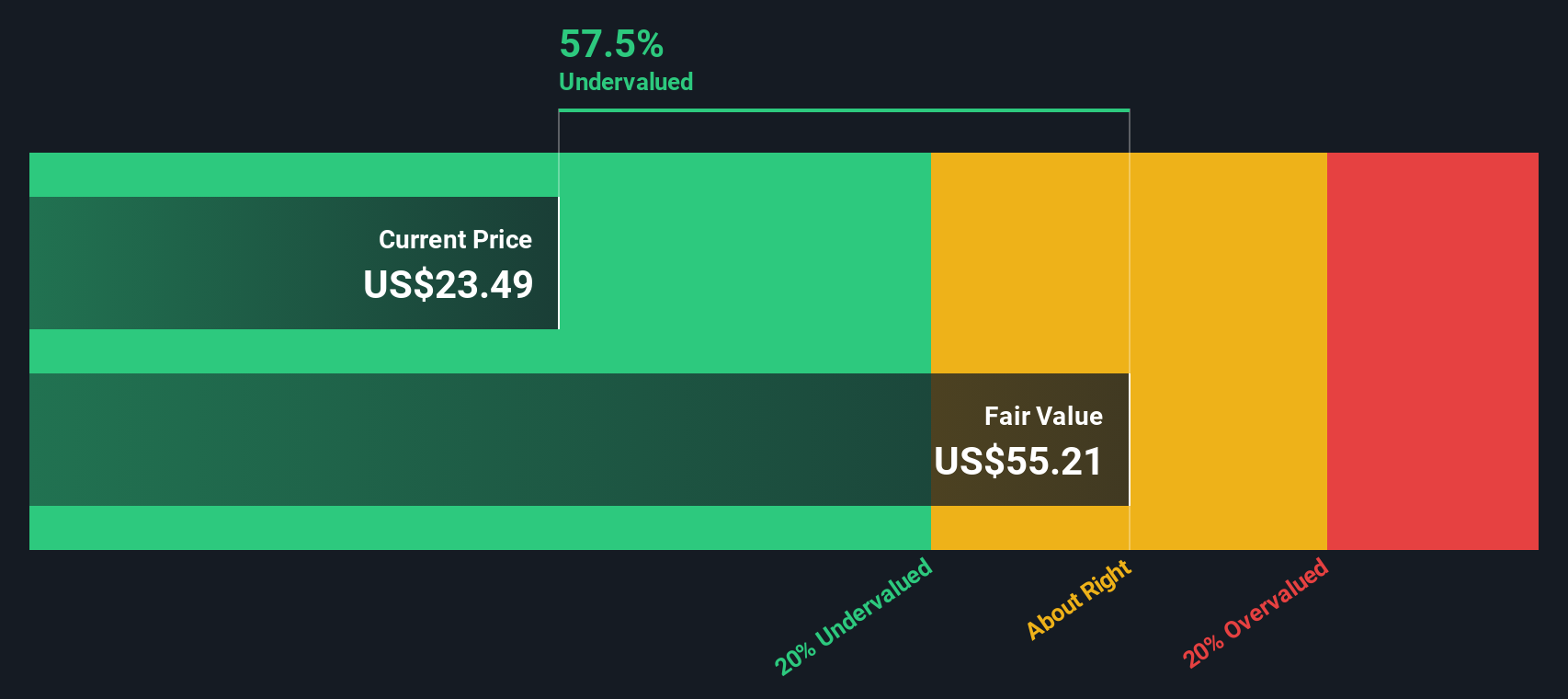

So with Dow posting a full year loss of US$2,623 million yet trading at a reported 38% intrinsic discount after a sharp recent rally, should you see value here or assume the market is already pricing in future growth?

Most Popular Narrative: 20.8% Overvalued

Dow last closed at $33.60, while the most followed narrative anchors fair value at $27.81. The story here is about how much optimism is already in the price.

Valuation Changes

• Fair Value: The model fair value estimate is effectively unchanged, moving marginally from US$27.82 to US$27.81 per share.

• Discount Rate: The discount rate has risen slightly from 7.85% to 7.87%, implying a modestly higher hurdle applied to future cash flows.

• Revenue Growth: Assumed revenue growth has increased from 0.73% to 1.46%, indicating a higher modeled top line growth rate.

• Net Profit Margin: The assumed profit margin has eased from 4.01% to 3.76%, reflecting slightly lower modeled profitability on future sales.

• Future P/E: The future P/E multiple used in the model has moved up from 15.22x to 15.88x, suggesting a somewhat higher valuation multiple assumption on projected earnings.

Want to see what is holding that fair value in place despite a loss making year and a higher assumed multiple? The core of this narrative sits in a slow but steady revenue path, a move from losses to positive margins, and an earnings profile that has to clear a higher discount rate. Curious how all of those ingredients balance out without blowing out the valuation model?

Result: Fair Value of $27.81 (OVERVALUED)

However, you still need to weigh risks such as ongoing margin pressure from higher feedstock and energy costs, as well as prolonged macro weakness that could sap demand and test this thesis.

Another Angle On Value

The most followed narrative sees Dow as 20.8% overvalued at $33.60 versus a fair value of $27.81, yet our DCF model points in the opposite direction, with Dow trading about 37.7% below its future cash flow value of $53.90. When two methods disagree this much, which story do you trust more?

Build Your Own Dow Narrative

If you interpret the numbers differently or prefer to test your own assumptions directly, you can build a custom view of Dow in just a few minutes, then Do it your way.

A great starting point for your Dow research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about sharpening your portfolio, do not stop at a single stock, use the Simply Wall St Screener to broaden your opportunity set.

- Hunt for quality at a discount with 51 high quality undervalued stocks that match strong fundamentals with prices that may not fully reflect them yet.

- Strengthen your income stream by scanning 14 dividend fortresses built around higher yield payouts that could support long term cash returns.

- Sleep easier by reviewing 83 resilient stocks with low risk scores that focus on companies scoring better on balance sheet and risk factors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.