A Look At DuPont (DD) Valuation After The AmberLite FPA57 Resin Launch

E. I. du Pont de Nemours and Company DD | 45.48 | -1.58% |

What the AmberLite FPA57 launch could mean for DuPont de Nemours (DD)

DuPont de Nemours (DD) has introduced its AmberLite FPA57 resin, a weak base anion resin aimed at organic acid producers seeking longer cycle times, greater physical stability, and improved fouling resistance in purification systems.

DuPont de Nemours’ AmberLite FPA57 launch arrives after a steady run in the share price, with a 30 day share price return of 8.71% and a 90 day share price return of 17.66%. This sits alongside a 1 year total shareholder return of 42.64% that points to building momentum rather than a short term spike.

If you are looking beyond DuPont de Nemours for other material and industrial names touching advanced tech themes, this could be a useful moment to check out high growth tech and AI stocks as a next step.

With the shares up strongly over the past year and trading only about 2% below one estimate of intrinsic value, is DuPont still misunderstood by the market, or are investors already paying up for future growth?

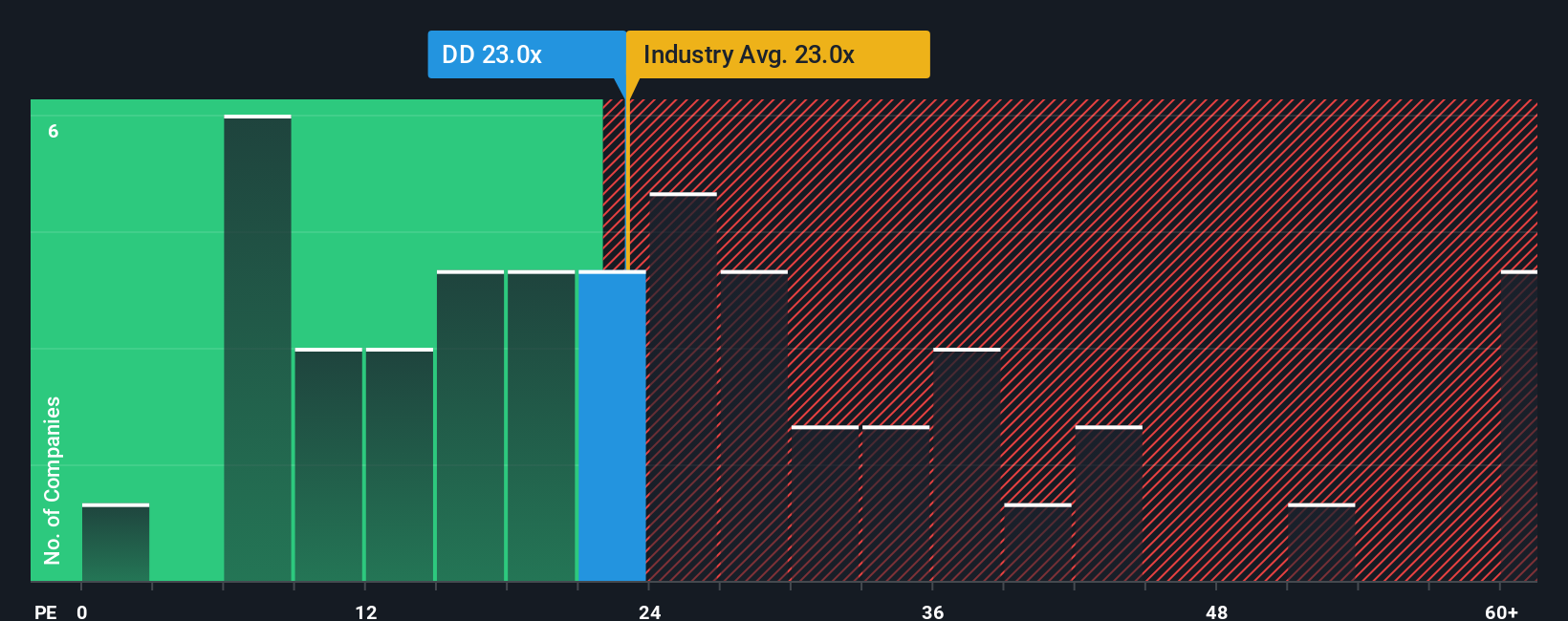

Most Popular Narrative: 9.7% Undervalued

At a last close of $44.43 versus a narrative fair value of $49.19, DuPont de Nemours is framed as modestly undervalued, with that gap tied directly to earnings and margin assumptions built into the model.

DuPont's accelerated growth in Electronics, particularly from AI-driven applications, advanced packaging, and high-performance computing, positions the company to capture outsized revenue expansion as node migrations and broader electronics market recovery unfold through 2025 and beyond.

Persistent strength and investment in Healthcare & Water, driven by surging global demand for clean water solutions and healthcare products, leverages favorable demographic, sustainability, and infrastructure trends to drive above-peer organic revenue growth and margin stability.

Curious how a materials name gets tagged with this kind of upside? The narrative leans on a sharp earnings ramp, fatter margins, and a richer future earnings multiple. Want to see exactly how those moving pieces stack up into that $49.19 figure and why the discount rate really matters here?

Result: Fair Value of $49.19 (UNDERVALUED)

However, the story could shift quickly if PFAS lawsuits become more costly than expected, or if China exposure in electronics encounters tighter trade and tech restrictions.

Another View: Market Multiple Flags Less Room for Error

While the narrative fair value of $49.19 suggests some upside from the $44.43 share price, the current P/E of 25.6x looks expensive next to both peers at 21.4x and a fair ratio of 23.8x. That richer multiple leaves less margin for disappointment if earnings progress stalls.

Build Your Own DuPont de Nemours Narrative

If this view does not quite line up with your own, or you prefer to test the assumptions yourself, you can build a fresh narrative in a few minutes by starting with Do it your way.

A great starting point for your DuPont de Nemours research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If DuPont has you thinking more broadly about your portfolio, this is the right moment to widen your search and see which other stories could fit your plan.

- Scan for potential mispriced opportunities by checking out these 872 undervalued stocks based on cash flows that might line up better with your return and risk comfort zone.

- Zero in on income potential by reviewing these 13 dividend stocks with yields > 3% that already offer yields above 3% without you having to sift through every stock manually.

- Tap into high growth themes by focusing on these 24 AI penny stocks that sit at the intersection of AI and public markets while this area is getting so much attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.