A Look At Dutch Bros (BROS) Valuation As It Joins The S&P MidCap 400 And Expands Its Store Base

Dutch Bros, Inc. Class A BROS | 50.35 | -0.42% |

Dutch Bros (BROS) is drawing attention as it prepares to join the S&P MidCap 400 index, a milestone that may influence how funds track the stock and how investors view its growth story.

Recent trading tells a mixed story, with a 1 day share price return of a 5.36% decline at a last close of $54.39 and a year to date share price return of a 12.50% decline, while the 3 year total shareholder return of 39.96% still reflects earlier momentum that recent selling pressure has cooled. Alongside the upcoming S&P MidCap 400 inclusion, fresh store openings in markets like Florida and Texas, and heightened attention around upcoming earnings have kept Dutch Bros in focus as investors reassess growth potential and risk.

If this kind of growth story has your attention, it could be a good moment to look beyond coffee and scan fast growing stocks with high insider ownership for other fast moving names.

With Dutch Bros joining the S&P MidCap 400, opening new shops and carrying a value score of 1 alongside mixed recent returns, is the current share price a bargain, or is the market already baking in years of growth?

Most Popular Narrative: 29.2% Undervalued

At a last close of $54.39 versus a narrative fair value of about $76.84, the most followed storyline on Dutch Bros is clearly pricing in a higher long term opportunity than the current market quote suggests.

The evolving menu, featuring specialty beverages, energy drinks, and an expanded food pilot, taps into the consumer trend toward premiumization and customization in beverages; these higher-margin offerings and incremental morning daypart food sales support higher average ticket sizes and future margin/earnings growth. Tight operational control through a focus on company-owned stores (versus franchising), more efficient new shop build-outs, and favorable labor and input cost management are creating operational leverage as scale increases, supporting higher net margins and earnings growth as new units mature.

It may be useful to explore what kind of revenue trajectory and margin lift would need to align to reach that fair value, and what earnings multiple this story leans on, without yet seeing the exact playbook behind those projections.

Result: Fair Value of $76.84 (UNDERVALUED)

However, rising labor costs and a tougher backdrop for restaurant spending could pressure margins and same shop sales, which would challenge the growth assumptions behind that 29.2% undervaluation story.

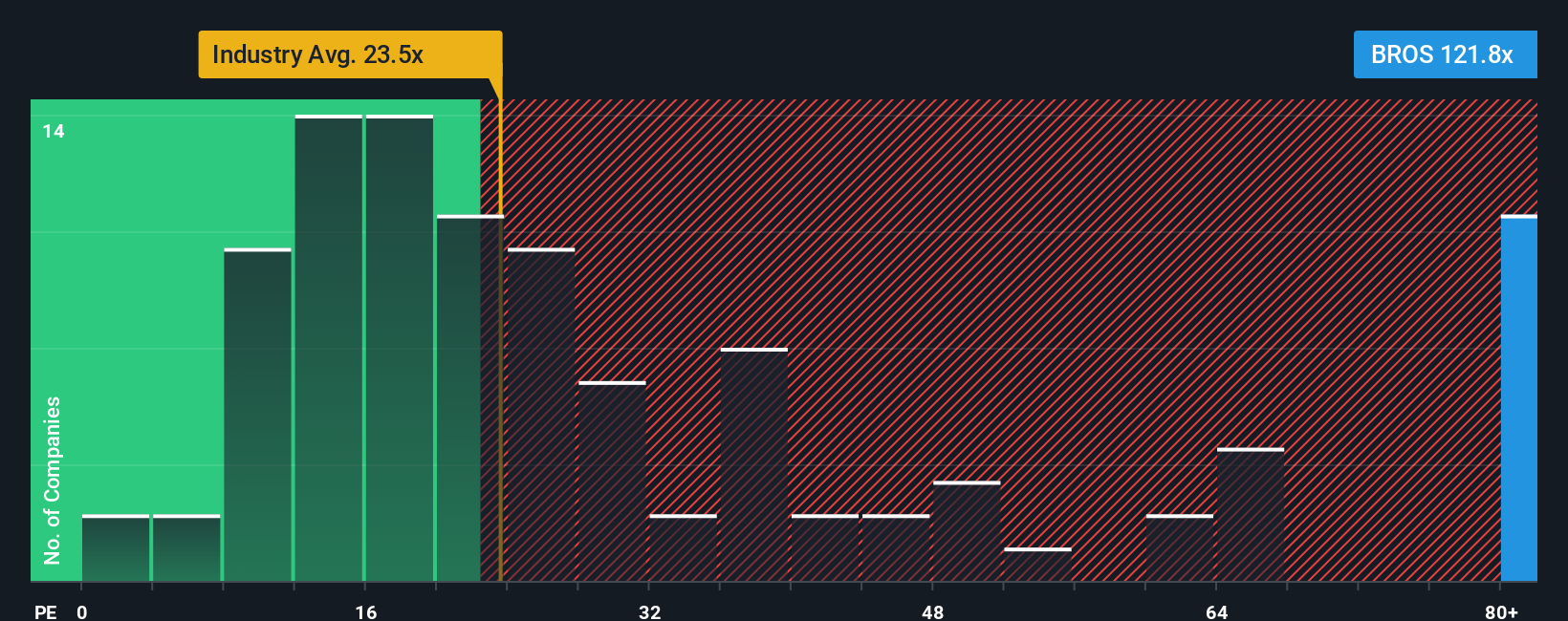

Another Way to Look at It: High P/E Brings Its Own Questions

That 29.2% narrative undervaluation sits next to a very different message from the current P/E. At about 111.3x earnings versus a 21.2x industry average, a 34.9x peer average and a 33.7x fair ratio, Dutch Bros is priced at a hefty premium that leaves less room if the growth story stumbles.

Build Your Own Dutch Bros Narrative

If you look at these numbers and reach a different conclusion, or just prefer to test your own assumptions, you can build a custom Dutch Bros view in a few minutes. To get started, use Do it your way.

A great starting point for your Dutch Bros research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Dutch Bros has you thinking about what else might be on your radar, do not stop here. Your next strong idea could be a few filters away.

- Spot potential value plays early by scanning these 868 undervalued stocks based on cash flows that currently screen as trading below what their cash flows imply.

- Capture growth themes in technology by checking out these 25 AI penny stocks aligned with artificial intelligence trends across different industries.

- Add income angles to your watchlist by reviewing these 14 dividend stocks with yields > 3% offering yields above 3% alongside equity exposure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.