A Look At EastGroup Properties (EGP) Valuation After Recent Share Price Softness

EastGroup Properties, Inc. EGP | 0.00 |

EastGroup Properties overview after recent trading performance

EastGroup Properties (EGP) has drawn fresh investor attention after a recent pullback, with the stock down around 2% over the past month even as the past 3 months show a gain.

At a recent close of US$198.21 and a market value of about US$10.6b, the industrial-focused real estate investment trust sits against a backdrop of annual revenue of US$735.38 million and net income of US$292.60 million.

In the short term, momentum has softened, with the share price down over the past month. However, a 10.18% year to date share price return and 19.87% 1 year total shareholder return indicate steadier longer term gains supplemented by dividends.

If this kind of steady, income supported profile appeals to you, it can be useful to compare it with other yield focused opportunities by scanning 9 dividend fortresses

With revenue of US$735.38 million, net income of US$292.60 million and the stock trading close to some estimates of intrinsic value, the key question is whether EastGroup still offers upside or if the market is already pricing in future growth.

Most Popular Narrative: 8% Undervalued

With EastGroup Properties last closing at $198.21 against a narrative fair value of $214.89, the current price sits a touch below that framework, putting the focus squarely on how much earnings power this industrial portfolio can deliver.

Persistent e-commerce expansion and ongoing supply chain modernization are ensuring elevated leasing spreads and high occupancy in EastGroup's infill, last-mile logistics facilities, supporting above-average rental rate growth and driving resilient net margins.

Read the complete narrative. Read the complete narrative.

Curious what underpins that fair value gap? The narrative leans on brisk top line growth, firm margins and a richer future earnings multiple than the sector. The exact mix of those inputs is what really moves the dial.

Result: Fair Value of $214.89 (UNDERVALUED)

However, this depends on tenants continuing to lease space at expected terms, while any prolonged slowdown in development leasing or tougher conditions in key markets could quickly test that fair value story.

Another View on Valuation

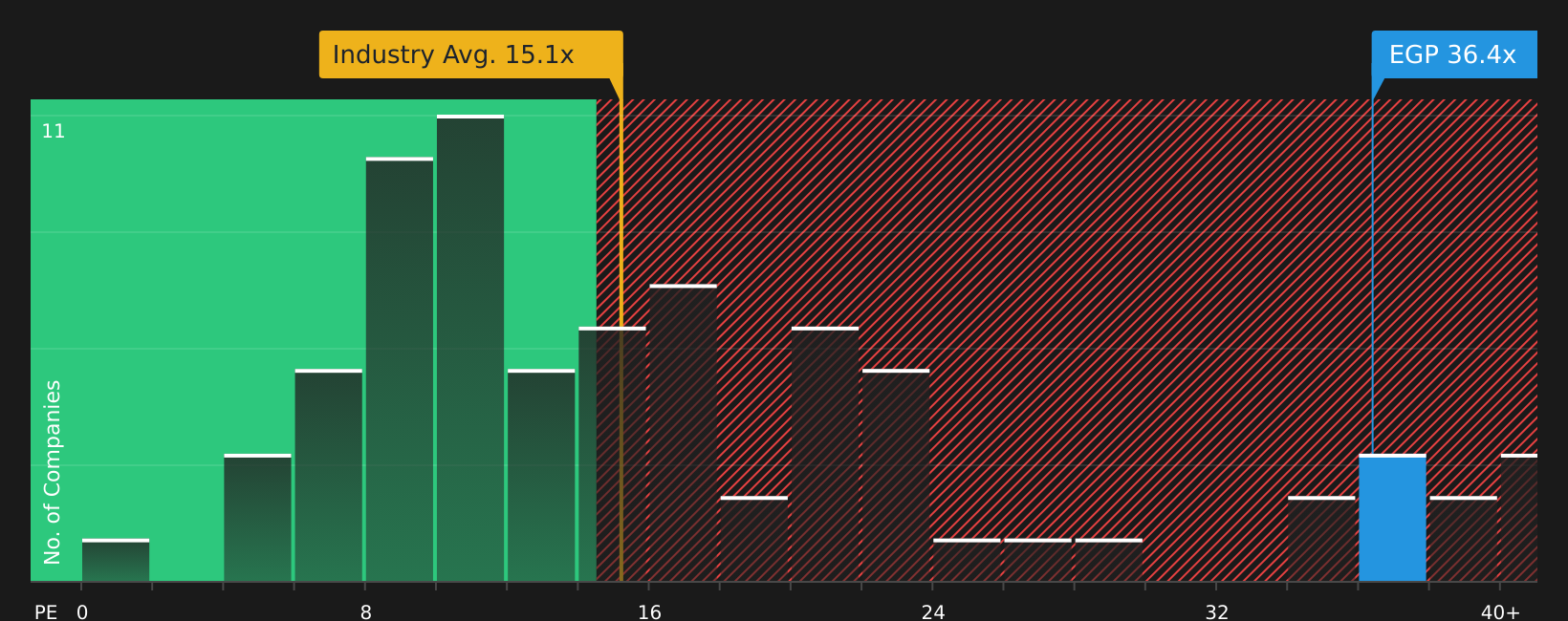

The fair value narrative suggests EastGroup is only 0.7% below intrinsic value, yet the market is already paying a P/E of 36.4x versus a fair ratio of 33.7x and about 26x for peers, with the broader global Industrial REITs group nearer 15x. That rich gap leaves less room if sentiment cools, so how comfortable are you paying up for quality here?

Next Steps

With mixed signals on valuation yet clear interest from both optimists and cautious investors, it makes sense to review the underlying data yourself and move promptly. To weigh up both sides of the story in one place, take a closer look at the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop with EastGroup. Broaden your watchlist today so you can compare income, quality and potential upside across a wider set of stocks and opportunities.

- Target resilient compounding potential by scanning companies in the 64 resilient stocks with low risk scores that may better match your comfort with volatility.

- Hunt for stronger value by reviewing the 49 high quality undervalued stocks and see which stocks currently offer more compelling fundamentals at their market prices.

- Strengthen the quality of your portfolio by focusing on businesses in the solid balance sheet and fundamentals stocks screener (46 results) that pair financial resilience with room for future decisions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.