A Look At EastGroup Properties (EGP) Valuation After Strong Q1 Results And Updated Earnings Guidance

EastGroup Properties, Inc. EGP | 0.00 |

EastGroup Properties (EGP) drew fresh attention after reporting first quarter sales of US$190.23 million and net income of US$94.62 million, along with new earnings guidance for the second quarter and full year 2026.

The earnings release and new guidance appear to have coincided with firming sentiment, with a 10.4% 30 day share price return and a 28.35% 1 year total shareholder return suggesting that momentum has been building rather than fading.

If this earnings driven move has you looking beyond a single stock, it could be a good moment to broaden your search and check out 18 top founder-led companies

With the share price around US$202 and trading only slightly below the average analyst target, the real question is whether EastGroup is still offering value or if the market is already pricing in future growth.

Most Popular Narrative: 2.5% Undervalued

With EastGroup Properties last closing at $202.22 against a narrative fair value of $207.37, the current setup leans slightly in favor of the narrative view that the shares are underpriced, using an 8.55% discount rate to bring future expectations back to today.

Structural US population growth and migration to Sunbelt markets continues to underpin robust demand for modern industrial or logistics properties, directly benefiting EastGroup's core portfolio and positioning the company for sustained revenue and NOI growth as these regions outpace national averages.

Curious what earnings path and margin profile sit behind that fair value, and why the narrative leans on a richer future P/E than the sector average? Those assumptions, plus the expected revenue runway and share count trajectory, are what really explain the small gap between the current price and the $207.37 figure.

Result: Fair Value of $207.37 (UNDERVALUED)

However, there is still real risk that slower development leasing and exposure to weaker coastal markets could pressure rent growth and test this underpriced narrative.

Another Angle On Valuation

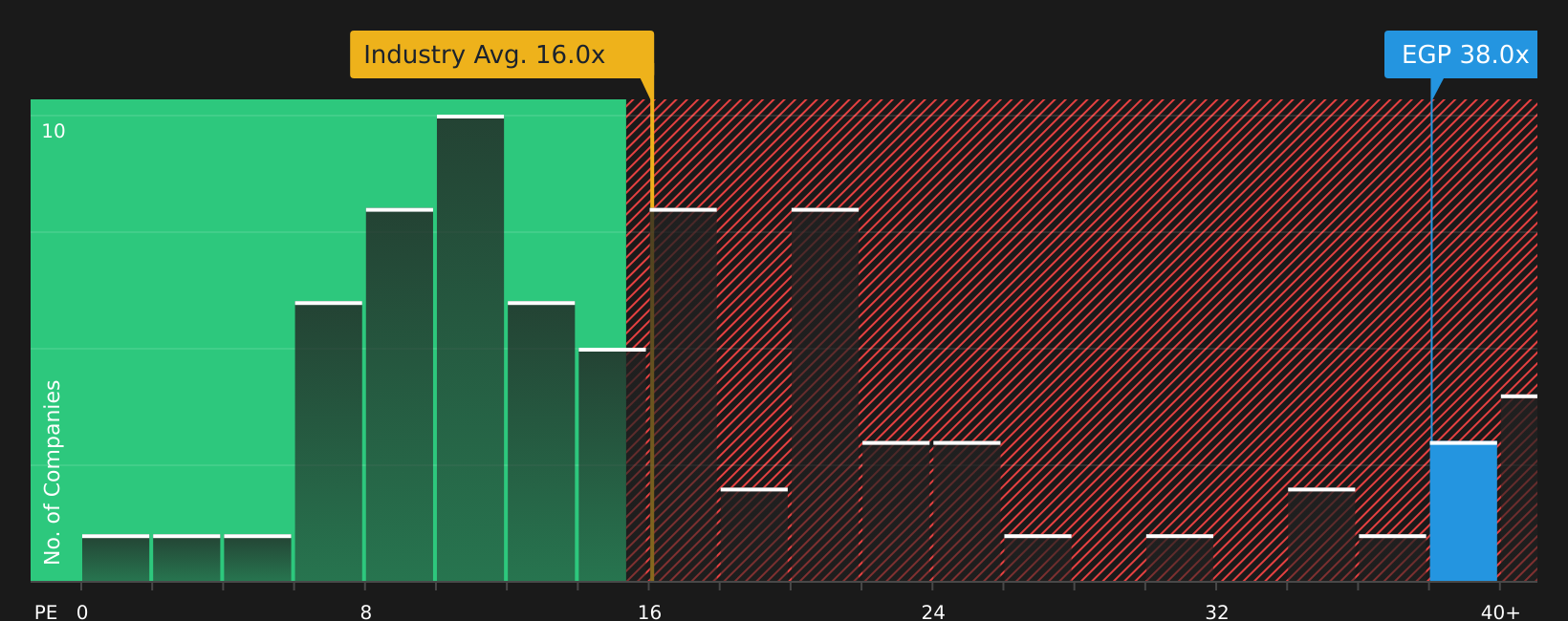

The popular narrative says EastGroup is about 2.5% undervalued at a fair value of $207.37, but the current P/E of 37.1x paints a different picture. That is far above the global Industrial REITs average of 16.7x, a peer average of 26.5x, and even the fair ratio estimate of 31.5x.

Put simply, the share price already reflects a richer earnings multiple than both peers and the fair ratio that the market could move toward. This raises the question of how much room is left if growth or sentiment cools.

Next Steps

With sentiment split between a slightly underpriced fair value view and a rich P/E, it helps to move fast and weigh the trade off yourself using 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If EastGroup has sharpened your interest in quality stocks, this is the moment to widen your watchlist and spot opportunities before everyone else does.

- Target income potential with companies that may support stronger cash flows by reviewing 14 dividend fortresses which is built on resilient payout profiles.

- Hunt for quality that is not fully reflected in current prices by checking the screener containing 25 high quality undiscovered gems before they attract wider attention.

- Prioritise capital protection by focusing on 72 resilient stocks with low risk scores to avoid leaving your portfolio exposed when conditions change.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.