A Look At Element Solutions (ESI) Valuation After Micromax And EFC Gases Acquisitions And Dividend Affirmation

Element Solutions Inc ESI | 34.08 | -1.56% |

Element Solutions (ESI) has drawn fresh attention after completing the acquisitions of Micromax and EFC Gases & Advanced Materials, expanding its footprint in semiconductor manufacturing and advanced materials, and affirming a quarterly dividend of $0.08 per share.

The recent Micromax and EFC Gases & Advanced Materials deals, along with fresh financing arrangements and the affirmed dividend, come against a backdrop of strong momentum, with a 90 day share price return of 29.75% and a five year total shareholder return of 96%.

If this has you thinking more broadly about materials, semiconductors and related supply chains, it could be a good time to check out 8 top copper producer stocks as another way to spot potential opportunities in resource linked names.

With Element Solutions sitting close to its all time high and trading only about 3% below one analyst price target, yet showing an estimated 22% intrinsic discount, is there still a buying opportunity here or is the market already pricing in future growth?

Most Popular Narrative: 2.2% Undervalued

Element Solutions' most followed narrative pegs fair value at $33.10, only slightly above the last close of $32.36, which puts a tight spotlight on the assumptions behind that number.

Successful commercialization and scaling of innovative products such as Kuprion's active copper, which addresses emerging challenges in advanced packaging and thermal management for hyperscalers and next-gen chips, is poised to enhance the margin profile and drive high-margin earnings growth over the next several years.

Want to see what sits behind that fair value call? The narrative leans on steady revenue expansion, fatter margins, and a future earnings multiple that has to do some heavy lifting.

Result: Fair Value of $33.10 (UNDERVALUED)

However, the story can change quickly if demand in core electronics and automotive markets softens, or if competitors pressure pricing and margins more than expected.

Another View: Rich P/E Puts Pressure On The Story

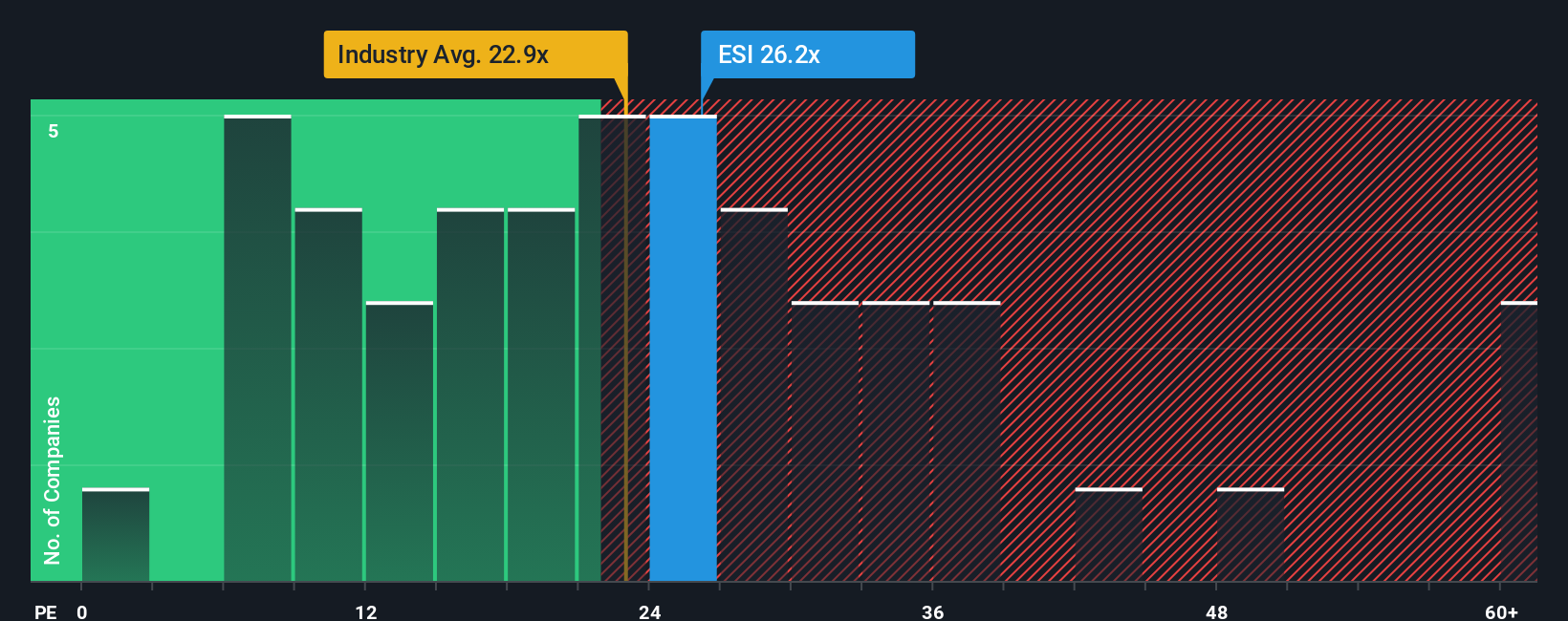

While the most popular narrative leans on a modest 2.2% discount to fair value, the current P/E of 32.7x tells a tougher story. That is well above the US Chemicals industry at 26.3x, the peer average at 22.8x, and even the fair ratio estimate of 23.5x.

In plain terms, the share price already builds in a lot of good news, which can limit upside if earnings or growth expectations slip. Does that premium feel justified to you, or does it tilt this more toward valuation risk than opportunity right now?

Build Your Own Element Solutions Narrative

If you are not fully sold on these narratives or simply prefer to test the numbers yourself, you can build a custom view in just a few minutes, starting with Do it your way.

A great starting point for your Element Solutions research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Element Solutions has sharpened your interest, do not stop here. Use the screener to quickly spot other opportunities that fit the way you like to invest.

- Hunt for strong value by checking companies our screener flags as 53 high quality undervalued stocks with solid fundamentals and support from their cash flows.

- Prioritise durability by reviewing solid balance sheet and fundamentals stocks screener (45 results) that focus on businesses with financial strength and resilience.

- Get early to potential standouts by scanning our screener containing 23 high quality undiscovered gems before they draw wider market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.