A Look At E.l.f. Beauty (ELF) Valuation After Strong Q3 Results And Raised Outlook

e.l.f. Beauty, Inc. ELF | 69.86 | +1.39% |

e.l.f. Beauty (ELF) has moved into the spotlight after reporting strong third quarter results and lifting its fiscal 2026 outlook, with raised guidance for both revenue and earnings capturing investor attention.

Despite the strong Q3 report and raised outlook, the share price has recently pulled back, with a 1-day share price return of a 9.18% decline and a 7-day share price return of a 9.61% decline, while the 5-year total shareholder return of around 230% shows how powerful the longer term move has been. That mix of short term weakness and longer term strength suggests sentiment has cooled in the near term even as the longer history still reflects meaningful value creation for shareholders.

If this latest update has you thinking about what else is moving in consumer facing brands, it could be worth widening your search to other growth stories via our 22 top founder-led companies.

With the stock around $76.86, a value score of 2 and an intrinsic value estimate that implies a premium rather than a discount, the key question is whether recent weakness signals a genuine opening or if markets are already pricing in future growth.

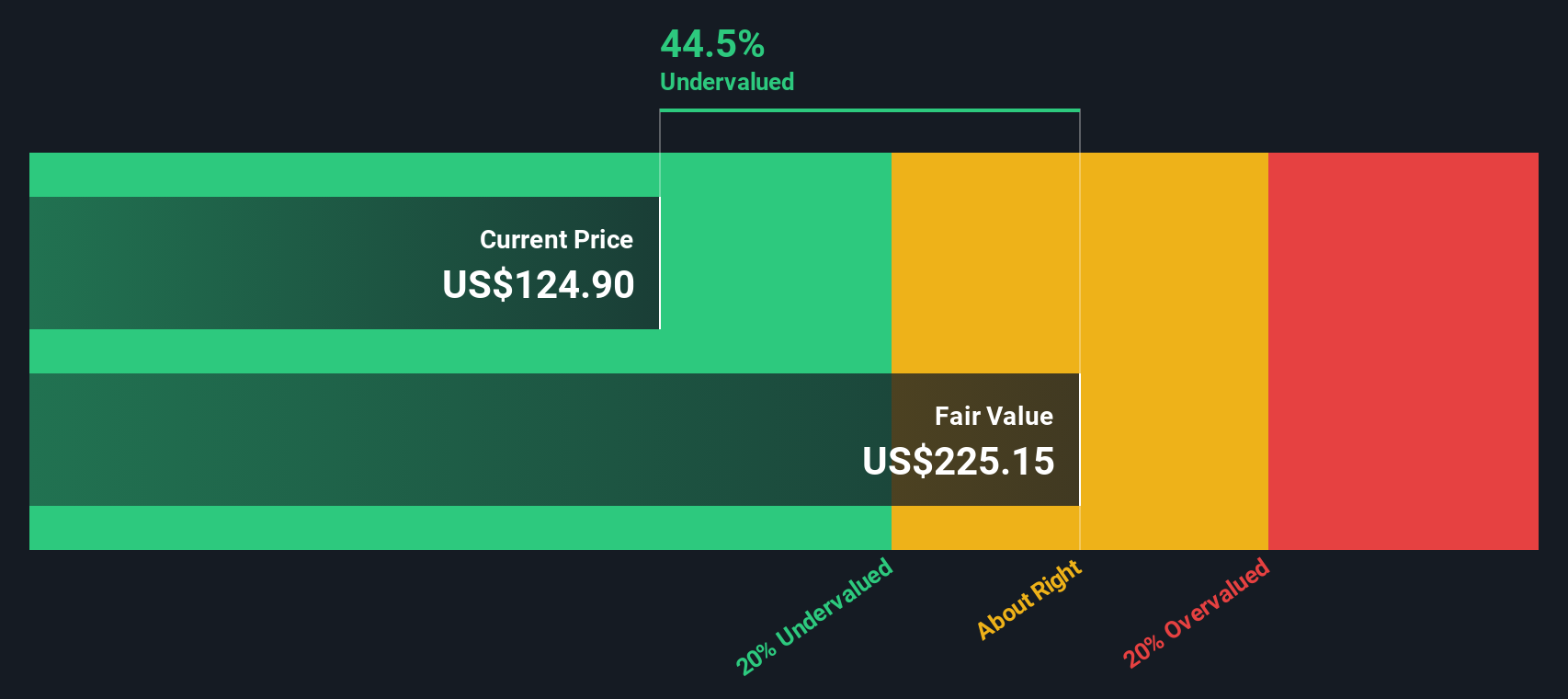

Most Popular Narrative: 69.4% Undervalued

According to the most followed narrative for e.l.f. Beauty, a fair value of $251.03 sits far above the last close at $76.86. This sets up a wide gap between market pricing and that narrative view.

Strong Brand Positioning and Product Innovation: e.l.f. Beauty has established itself as a leading brand in the masstige beauty category, offering high-quality products at affordable prices. The company is known for its innovative approach to product development, consistently introducing new and exciting items that appeal to a wide range of consumers.

Want to see what kind of growth curve could justify such a large gap between price and fair value? According to WallStreetWontons, the narrative leans on ambitious revenue expansion, rising profitability and a premium future earnings multiple that you would usually associate with faster growing sectors, all rolled into one valuation story.

Result: Fair Value of $251.03 (UNDERVALUED)

However, this bullish story could be challenged if sales growth continues to slow while rising costs and higher debt servicing start to pressure profitability and flexibility.

Another View: Cash Flows Paint a Tighter Picture

The popular narrative points to a fair value of $251.03 and calls e.l.f. Beauty undervalued, but our DCF model lands closer to $54.94 per share. With the stock at $76.86, that framework suggests the shares look expensive, not cheap. Which story do you lean toward?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out e.l.f. Beauty for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own e.l.f. Beauty Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a custom view in just a few minutes with Do it your way

A great starting point for your e.l.f. Beauty research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If e.l.f. Beauty has you thinking harder about where to put your next dollar, do not stop here. Use the tools that help you compare across many opportunities.

- Spot potential value by scanning companies that screen well on quality and pricing using our 55 high quality undervalued stocks.

- Prioritise resilience by checking out companies that pass our 81 resilient stocks with low risk scores for more stable risk profiles.

- Hunt for fresh opportunities off the beaten path with our screener containing 25 high quality undiscovered gems that highlight lesser known names with solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.