A Look At Enphase Energy (ENPH) Valuation After Earnings Beat And Upbeat Guidance

Enphase Energy, Inc. ENPH | 34.92 | -8.78% |

Enphase Energy (ENPH) is back in focus after its latest earnings report topped market expectations on both revenue and earnings, paired with first quarter guidance that came in above analyst forecasts.

The latest update has triggered a sharp rebound in sentiment, with a 1 day share price return of 5.35% and a 90 day share price return of 64.79%. However, the 1 year total shareholder return remains a 21.61% loss, so recent momentum is rebuilding from a weaker long term base.

If strong moves in Enphase are catching your eye, this could be a good moment to see what else is setting up in solar and storage, including 24 power grid technology and infrastructure stocks.

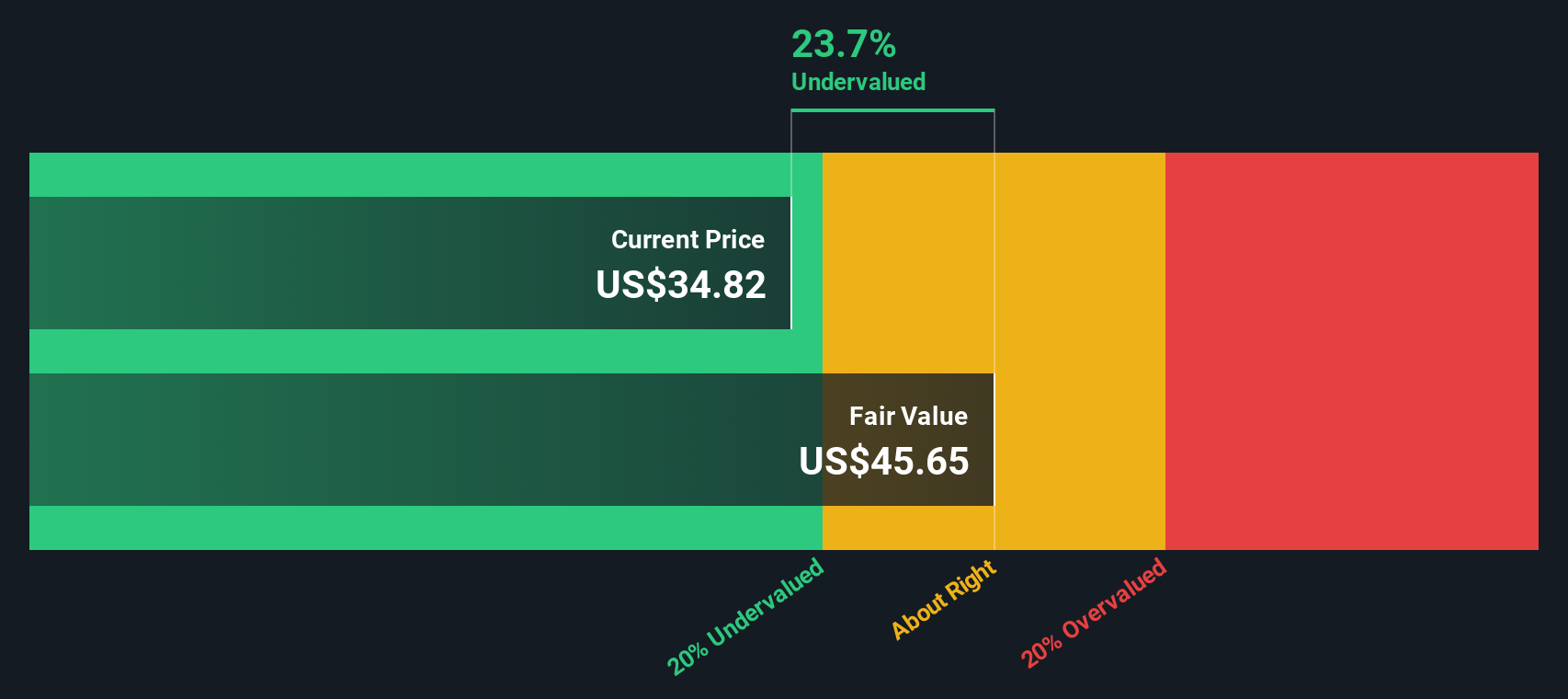

With the share price up sharply and the stock trading at around a 9% premium to the average analyst target, but an implied 37% premium to some intrinsic estimates, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 35.2% Undervalued

Against Enphase Energy's last close at $49.80, the most followed narrative pegs fair value at $76.86, implying a sizeable valuation gap based on long term assumptions rather than short term sentiment.

Enphase’s Serviceable Addressable Market (SAM) Is Not Justified. While past performance gives us a basis to build upon, we need to review whether Enphase can recover and surpass previous results. Currently, analysts are modeling revenues of $1.6B by 2025. However, they extrapolate that Emphase will recover 2023 revenue levels by 2027. This needs to be consistent with the growth potential of Enphase, which I analyze below.

Curious how this fair value gets to $76.86 when recent growth expectations are more muted? The narrative leans heavily on long range revenue recovery, resilient margins and a specific multiple to frame what Enphase could be worth if those building blocks fall into place.

According to Goran_Damchevski, that tension between a pressured solar cycle today and a larger future addressable market is central to the $76.86 estimate, with the 9.7% discount rate and profit margin assumptions doing a lot of the work behind the scenes.

Result: Fair Value of $76.86 (UNDERVALUED)

However, this narrative could change if microinverters prove more durable than feared or if policy shifts make residential solar payback periods more attractive again.

Another View: Our DCF Flags Overvaluation

While the most followed narrative sees Enphase Energy as 35.2% undervalued at a fair value of $76.86, our DCF model points the other way. At $49.80, ENPH is trading above our future cash flow value estimate of $36.26, which screens as overvalued on this method.

That gap between a user led narrative and the SWS DCF model raises an important question for you: which set of assumptions about growth and risk do you trust more when the price is already leaning toward optimism?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Enphase Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Enphase Energy Narrative

If you are not fully aligned with these views or simply prefer to rely on your own work, you can build a custom thesis in minutes using Do it your way.

A great starting point for your Enphase Energy research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Enphase has you thinking more broadly about your portfolio, do not stop here. Lining up a few fresh ideas now could make a real difference later.

- Target quality at a discount by reviewing our list of 53 high quality undervalued stocks that combine strong fundamentals with prices that may not fully reflect them yet.

- Prioritize resilience by checking out 86 resilient stocks with low risk scores, a group of companies filtered for lower risk scores that can help steady your holdings.

- Get ahead of the crowd by scanning our screener containing 25 high quality undiscovered gems, where lesser known names with solid financials are waiting for closer attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.