A Look At Estée Lauder (EL) Valuation After Cautious 2026 Guidance And Tariff Impact Forecast

Estee Lauder Companies Inc. Class A EL | 69.12 | -2.25% |

Estée Lauder Companies (EL) is back in focus after its latest earnings update, where stronger profitability and a raised outlook were accompanied by cautious guidance for fiscal 2026 and a planned $100 million tariff hit.

The latest earnings release and cautious fiscal 2026 guidance triggered a sharp reset in expectations, with the stock dropping heavily around the announcement and posting a 7 day share price return of a 16.24% decline, even though the 90 day share price return of 9.5% and 1 year total shareholder return of 47.32% show that longer term momentum has been more positive.

If this volatility has you looking beyond beauty, it could be a good moment to broaden your search and check out our screener of 22 top founder-led companies.

With Estée Lauder now trading below its recent levels and showing an intrinsic discount alongside a modest gap to analyst targets, the key question is whether recent weakness signals an undervalued entry point or if the market already reflects its future growth.

Most Popular Narrative: 4.6% Undervalued

Estée Lauder's most followed narrative currently pegs fair value at about $104.30 per share, a touch above the last close of $99.47, which puts a small valuation gap under the microscope.

Significant investment is being allocated to product innovation across prestige price tiers, with a focus on clinically backed and trend driven skincare, makeup, and luxury fragrance launches; innovation is targeted to exceed 25% of sales in fiscal '26, and faster time to market is being emphasized, likely enhancing premium pricing power, brand equity, and gross margins.

Curious how this push into higher end fragrance and faster product cycles feeds into the $104 fair value, future margins, and earnings power assumptions? The narrative leans on steady top line growth, a step change in profitability, and a richer future earnings multiple to justify that price tag, but the exact mix of those drivers is where the story gets interesting.

Result: Fair Value of $104.30 (UNDERVALUED)

However, the story could shift quickly if travel retail stays weak or if China and other key emerging markets face disruptions that keep revenue and margins under pressure.

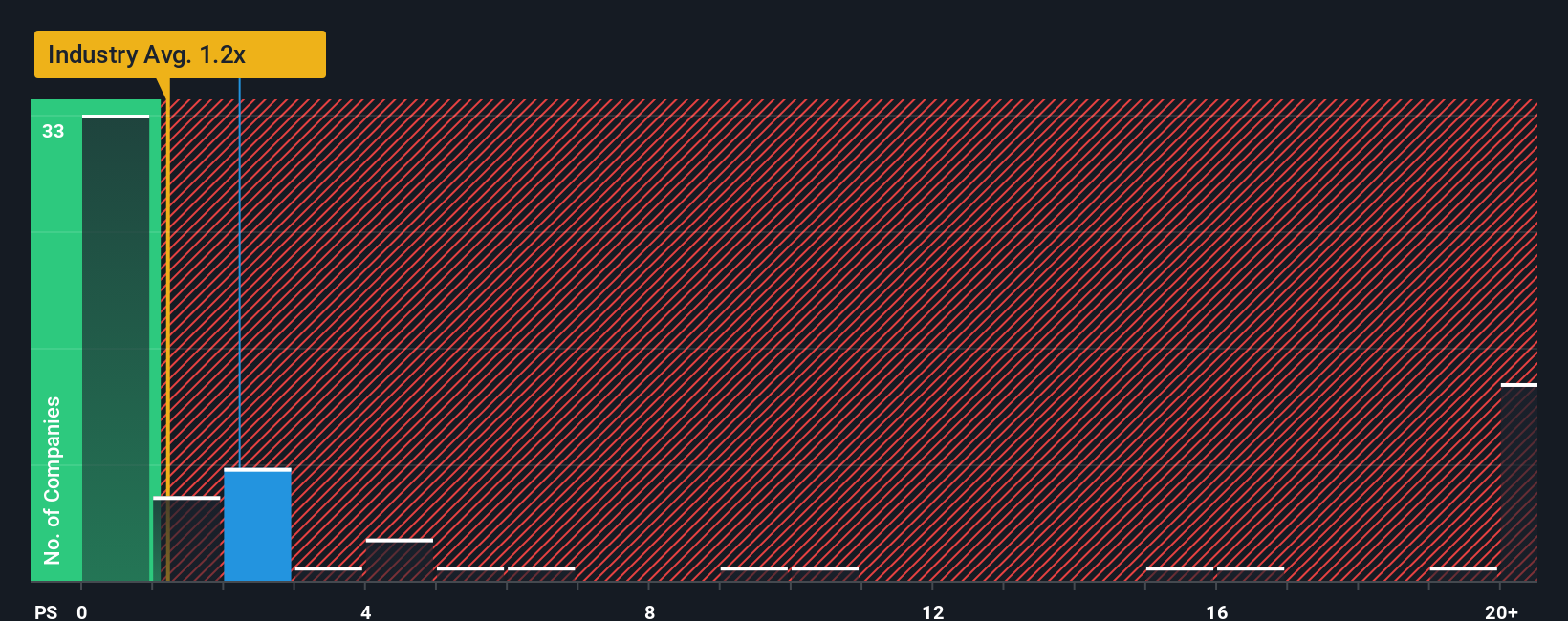

Another View: Multiples Point to a Richer Price Tag

While our fair value estimate suggests Estée Lauder trades about 13.2% below intrinsic value, its current P/S ratio of 2.5x tells a tougher story. That is richer than the US Personal Products industry at 1x, peers at 2x, and even above its own fair ratio of 2.2x. This raises the question of how much valuation risk you are really comfortable with here.

Build Your Own Estée Lauder Companies Narrative

If you see the numbers differently or simply want to test your own assumptions, you can build a personalised Estée Lauder view in just a few minutes, starting with Do it your way.

A great starting point for your Estée Lauder Companies research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Estée Lauder has sharpened your focus, do not stop here. Use the same data driven approach to explore additional opportunities across sectors and styles.

- Target potential mispricings by scanning through 52 high quality undervalued stocks which combine quality fundamentals with prices that may not fully reflect their strengths.

- Strengthen your income stream by reviewing 14 dividend fortresses designed for investors who want higher yields supported by solid business profiles.

- Prioritise resilience by checking companies in our 84 resilient stocks with low risk scores which score well on financial stability and risk metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.