A Look At Exxon Mobil (XOM) Valuation After Recent Share Price Strength

Exxon Mobil Corporation XOM | 160.69 | -0.06% |

Recent share moves and where Exxon Mobil (XOM) stands now

Exxon Mobil (XOM) has drawn fresh attention after a recent run in its share price, with the stock up around 13% over the past month and about 21% in the past 3 months.

That recent strength comes after a choppy year, with a 1 year total shareholder return of 33.98% supported by dividends and a 5 year total shareholder return of about 3x, even though the latest 1 day share price return of a 2.12% decline shows that momentum can pause.

If Exxon Mobil's move has you thinking about where else capital might work hard in energy and related areas, it could be a good time to scan aerospace and defense stocks for other large scale industrial plays tied to global demand and security themes.

With Exxon Mobil trading around $138.40, sitting close to some analyst targets but with an estimated 30% intrinsic discount, the key question is whether this reflects a genuine value gap or a market that has already priced in potential future growth.

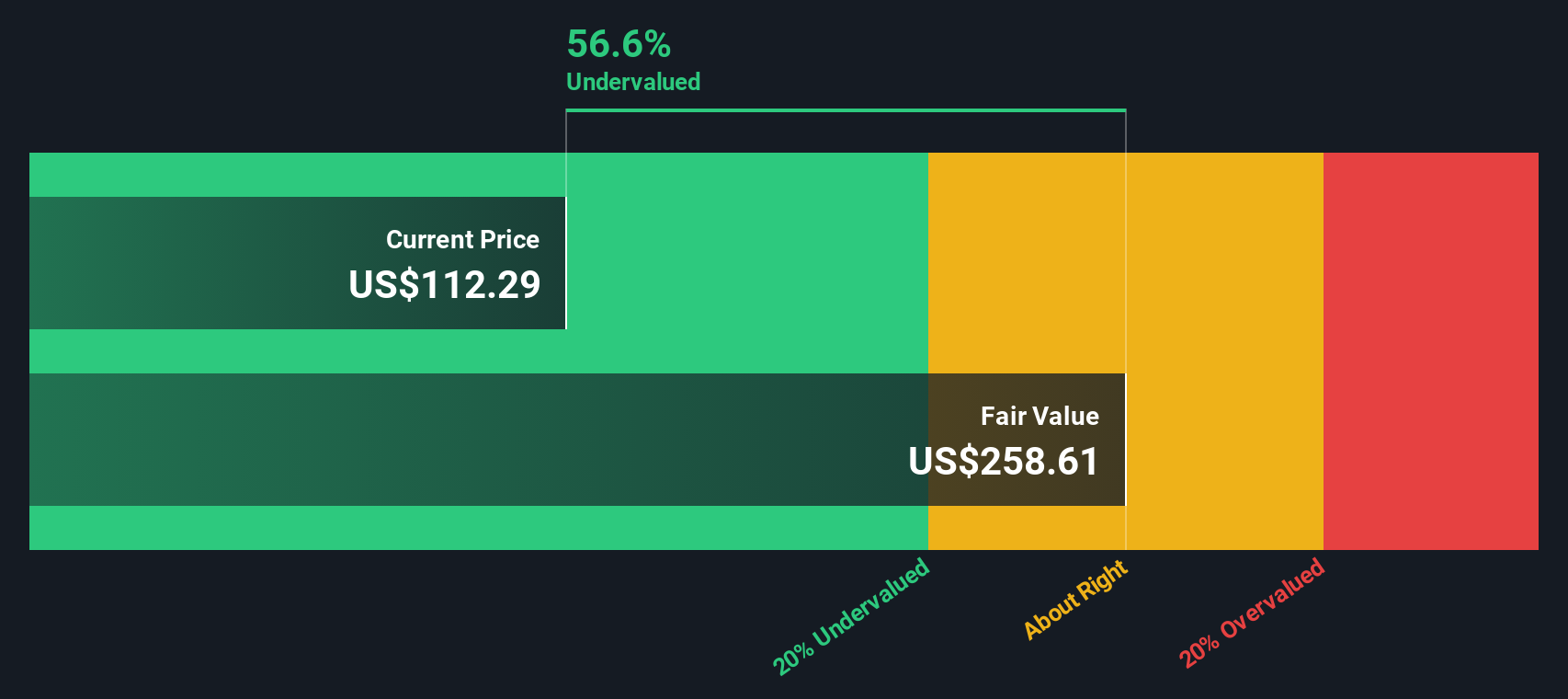

Most Popular Narrative: 4.8% Overvalued

Exxon Mobil's last close at $138.40 sits slightly above the narrative fair value of $132.00, which frames the current debate around upside from here.

This analysis concludes that Exxon Mobil (XOM) represents an investment opportunity, with a fair value of $132.00 per share, relative to a price of $112.32 at the time of the analysis. The view presented is based on the company's fundamental transformation, operational focus, and capital allocation approach, rather than on a speculative bet on higher oil prices.

Curious what sits behind that fair value? According to Helzur, the narrative leans heavily on cash flow durability, margin assumptions, and future earnings multiples that many investors might not expect.

Result: Fair Value of $132 (OVERVALUED)

However, this narrative could unravel if commodity prices weaken for a prolonged stretch or if Low Carbon Solutions fails to reach the earnings and policy support implied.

Another way to look at value

The user narrative leans on cash flows and a fair value of $132.00, but our DCF model paints a different picture, with an implied value of $197.61 per share. At a recent price of $138.40, that points to the shares trading below this DCF estimate, which raises a clear question: which story do you trust more, the market price or the cash flow model?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Exxon Mobil for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Exxon Mobil Narrative

If you look at the numbers and come to a different conclusion, or simply prefer doing your own work, you can build a complete view in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Exxon Mobil.

Looking for more investment ideas?

If Exxon Mobil has sharpened your focus on where your next dollar should go, do not stop here, broaden your watchlist with a few focused stock ideas.

- Spot potential value by scanning these 877 undervalued stocks based on cash flows that the market may be pricing cautiously compared to their underlying cash flows.

- Zero in on income opportunities by checking out these 13 dividend stocks with yields > 3% that offer yields above 3% alongside listed fundamentals.

- Get ahead of sector shifts by reviewing these 18 cryptocurrency and blockchain stocks that are tied to cryptocurrency and blockchain themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.