A Look At F5 (FFIV) Valuation After Raised 2026 Revenue Guidance And Solid Q2 Earnings

F5, Inc. FFIV | 0.00 |

F5 (FFIV) drew fresh investor attention after its Q2 2026 earnings update, where management raised full year revenue guidance, highlighted demand across application delivery and cybersecurity offerings, and noted strong free cash flow generation.

Recent price action reflects that increased confidence. The share price is up 6.6% over the past week, 15.1% over 3 months, and has a year to date share price return of 25.9%. The 3 year total shareholder return of 142.6% points to firmly established momentum.

If Q2 earnings have you rethinking your exposure to infrastructure and security, it could be a good time to widen the net and check out 37 AI infrastructure stocks

With F5 trading at $323.20 against an average analyst price target of $337.40 and an estimated intrinsic value gap of about 24%, the key question is whether this signals a genuine opportunity or if the market is already factoring in future growth.

Most Popular Narrative: 3.8% Overvalued

Compared with the latest $323.20 close, the most followed narrative pegs F5's fair value at $311.30, implying a small valuation premium that turns on a few key assumptions.

The ongoing shift to high-margin, recurring software and SaaS subscription revenue, along with strong renewal and expand activity from existing customers, is improving revenue visibility and predictability while supporting operating margin and EPS growth.

Read the complete narrative. Read the complete narrative.

Curious what kind of revenue mix and margin profile would need to hold up to support that premium? The narrative leans on recurring software strength, firm profitability, and a future earnings multiple that assumes investors continue to pay a premium for resilient security exposure.

Result: Fair Value of $311.30 (OVERVALUED)

However, slower take up of software, combined with heavy exposure to large enterprise and telecom budgets, could still unsettle the thesis if demand patterns shift.

Another View: Market Multiple Says “Good Value”

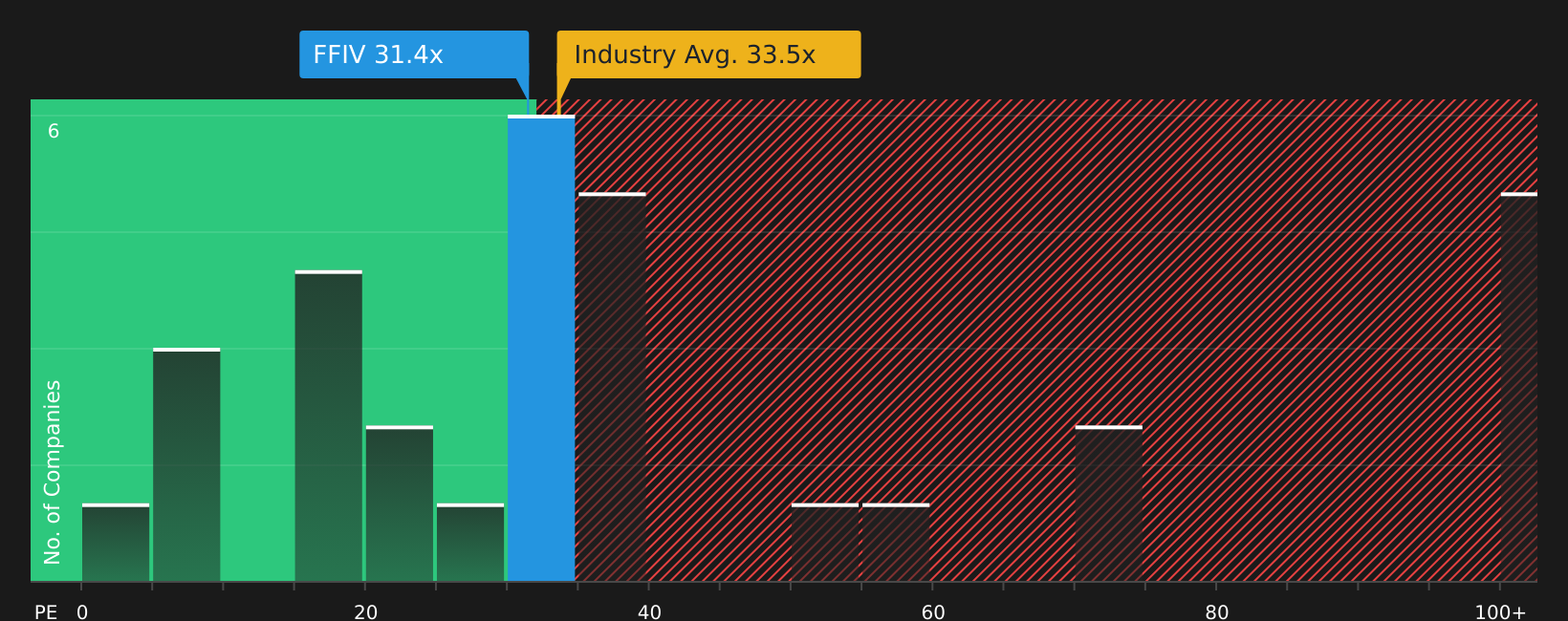

The analyst narrative points to F5 trading about 3.8% above its $311.30 fair value, yet the market ratio story is different. At a P/E of 25.9x versus a 28.7x fair ratio, 35.4x for the US Communications industry, and 91.6x for peers, the market is pricing F5 more cautiously. That gap could signal room for a re rating or serve as a reminder to question why the discount exists at all.

To see what the numbers say about this price, check the detailed valuation breakdown in the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mix of optimism and caution in this story, it makes sense to move quickly, review the facts yourself, and stress test the thesis from both sides by weighing the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

Focusing on one company can limit your options, so now is the moment to broaden your watchlist and let high quality data surface fresh opportunities.

- Start building a watchlist of quality at a reasonable price by scanning 50 high quality undervalued stocks that may offer stronger fundamentals than the headline names everyone is already watching.

- Strengthen the defensive side of your portfolio by reviewing solid balance sheet and fundamentals stocks screener (44 results) that aim to pair financial resilience with room for future compounding.

- Get ahead of the crowd by tracking screener containing 25 high quality undiscovered gems that might sit off the mainstream radar yet still meet strict quality and financial filters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.