A Look At Fidelity National Information Services (FIS) Valuation After The Worldpay Exit And Issuer Solutions Acquisition

Fidelity National Information Services, Inc. FIS | 46.29 | +2.48% |

Fidelity National Information Services (FIS) recently reshaped its business mix by selling its remaining Worldpay stake and buying Global Payments' issuer solutions arm, while lifting its 2025 revenue and earnings guidance to reflect operational progress.

Even after the recent portfolio reshuffle and upgraded 2025 guidance, the 1-year total shareholder return of 23.71% decline and 5-year total shareholder return of 47.69% decline, alongside a 30-day share price return of 9.96% decline, suggest momentum has been weak as the market reassesses execution and risk around FIS’s refocused model.

If FIS’s repositioning has you thinking about where payment and banking technology might head next, it could be worth scanning high growth tech and AI stocks for other plays tied to AI driven financial services.

With FIS trading at $60.50 and sitting on multiyear share price declines despite upgraded 2025 guidance and new AI-focused offerings, is the reset already reflected in the stock, or could weakness suggest a potential opportunity that the market has not fully priced in?

Most Popular Narrative: 24.8% Undervalued

With Fidelity National Information Services last closing at $60.50 against a narrative fair value of $80.45, the widely followed thesis sees meaningful upside grounded in long term earnings power.

Increasing client demand for cloud-based and AI-powered fintech solutions, such as the launch of TreasuryGPT and Banker Assist, is allowing FIS to upsell higher-value, "stickier" products to financial institutions modernizing their operations, which should support long-term revenue expansion and improved net margins.

Curious what kind of earnings ramp and margin profile sit behind that fair value number? The narrative leans on calculated revenue progression and richer profitability assumptions that go well beyond today’s headline metrics.

Result: Fair Value of $80.45 (UNDERVALUED)

However, there are clear risks here, including tougher fintech competition and potential integration setbacks that could limit margins and challenge the long-term earnings story.

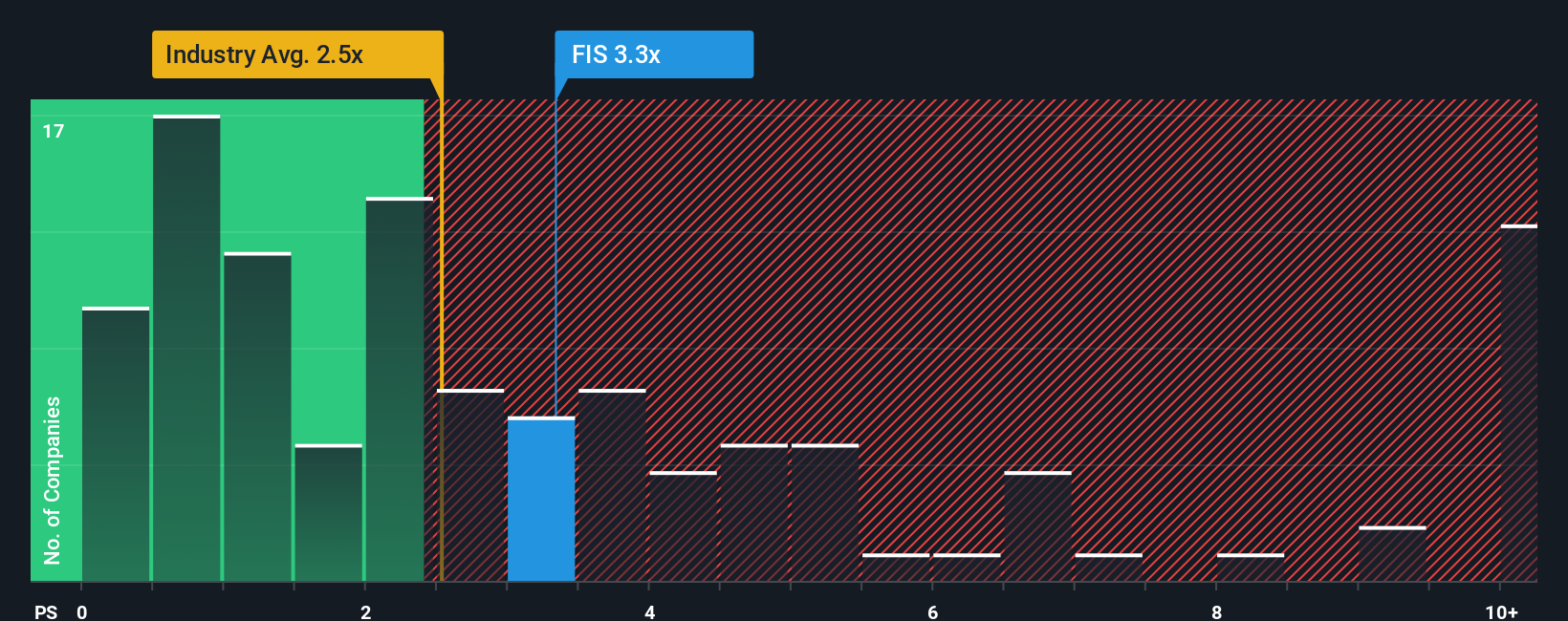

Another Take: What The P/S Ratio Is Saying

That 24.8% undervalued fair value hinges on long term earnings assumptions, but the current P/S ratio of 3x tells a different story. It is higher than both peers at 2.7x and the US Diversified Financial industry at 2.8x, and is almost in line with an estimated fair ratio of 3.1x.

In plain terms, the market is already paying a premium to peers. At the same time, only a small gap to the fair ratio hints at limited room for error if growth or margins fall short. If the optimistic earnings path wobbles, does a premium sales multiple still feel comfortable?

Build Your Own Fidelity National Information Services Narrative

If you think the numbers tell a different story, or you prefer to test your own assumptions, you can build a custom thesis in minutes with Do it your way.

A great starting point for your Fidelity National Information Services research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Ready for more stock ideas?

If FIS has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to quickly surface fresh, data driven ideas built around clear fundamentals.

- Target income potential by scanning these 14 dividend stocks with yields > 3% that might help you build a portfolio with more consistent cash returns.

- Spot growth themes early by checking out these 23 AI penny stocks tied to real business adoption of artificial intelligence, not just buzzwords.

- Hunt for mispriced opportunities by reviewing these 872 undervalued stocks based on cash flows that currently trade below what their cash flows may justify.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.