A Look At First Citizens BancShares (FCNC.A) Valuation After Earnings Guidance And Preferred Share Offering

Earnings reaction and new preferred offering put First Citizens BancShares in focus

First Citizens BancShares (FCNC.A) is back on investors’ radar after its latest earnings release and 2026 guidance on net interest margin and operating expenses prompted a sharp share-price reaction.

Alongside that outlook, the bank completed a US$400 million fixed income offering of 16,000,000 non convertible depositary shares at US$25 each, with a fixed coupon and a US$0.5545 per share discount.

Beyond the immediate earnings reaction, First Citizens BancShares’ recent moves sit against a mixed backdrop, with a 90 day share price return of 18.91% and a five year total shareholder return close to 2x. This suggests long term momentum alongside shorter term swings in sentiment around guidance and capital raising.

If this bank news has you thinking about where else capital might flow in financial services and infrastructure, it could be a good time to scan 22 top founder-led companies for other potential ideas.

With First Citizens BancShares trading at US$2,160.99, sitting at about a 5% discount to the latest analyst price target and an indicated intrinsic discount of roughly 22%, the key question is whether this signals a genuine opportunity or if the market already reflects its future growth.

Most Popular Narrative: 5.4% Undervalued

First Citizens BancShares is trading at $2,160.99 against a widely followed narrative fair value of $2,283.57, setting up a modest valuation gap that hinges on how its 2026 roadmap plays out.

The company is leveraging its strong balance sheet and liquidity position to continue share repurchase programs, which are expected to improve earnings per share (EPS) significantly by reducing the number of shares outstanding.

First Citizens anticipates further growth in deposits through its Direct Bank and General Bank, using digital strategies and proactive marketing to attract and retain clients, potentially enhancing net interest income as deposit rates decline.

Curious what sits behind that fair value gap? The narrative leans heavily on measured revenue growth, firm margins, and a future earnings multiple that assumes disciplined execution. The exact mix of those inputs might surprise you.

Result: Fair Value of $2,283.57 (UNDERVALUED)

However, you also need to weigh the risk that rate cuts could pressure net interest income, and that SVB related credit losses or commercial real estate stress could hit earnings.

Another Angle On Valuation

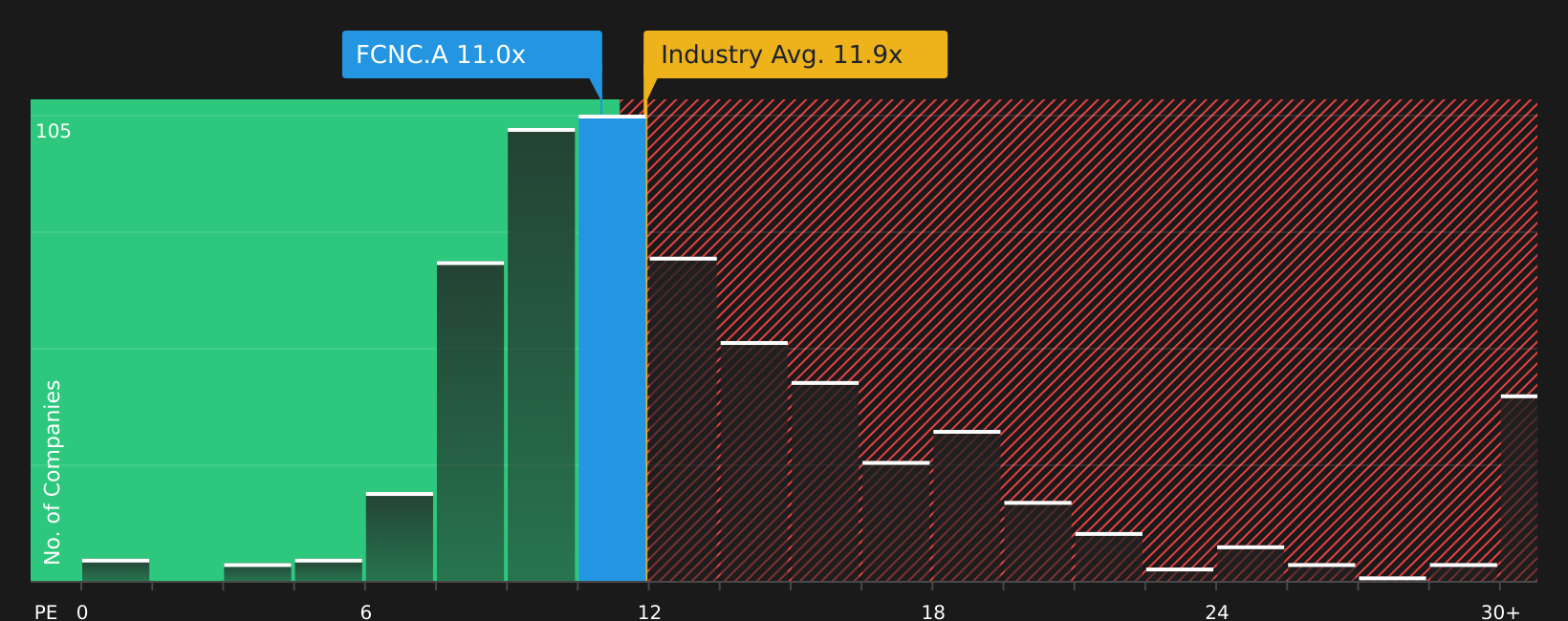

The first view leans on future earnings and narrative fair value, but the current P/E of 12.1x tells a slightly different story. That is just above the US Banks industry at 12x, below peers at 19.6x, and under the fair ratio of 13.5x. This points to some valuation cushion but also less obvious mispricing. Which signal do you trust more?

Build Your Own First Citizens BancShares Narrative

If this view does not quite fit how you see First Citizens BancShares, you can quickly test your own assumptions and build a custom story in minutes, starting with Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding First Citizens BancShares.

Looking for more investment ideas?

If you are weighing what to do next after looking at First Citizens BancShares, it makes sense to widen your net and see what else stands out.

- Target reliable cash generators by scanning our list of 52 high quality undervalued stocks, which combine attractive pricing with solid fundamentals.

- Strengthen your income stream by reviewing 14 dividend fortresses, which aim to pair higher yields with resilience.

- Prioritise resilience and sleep better at night by focusing on 84 resilient stocks with low risk scores, which score well on our risk filters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.