A Look At First Solar (FSLR) Valuation After Choppy Recent Share Price Moves

First Solar, Inc. FSLR | 0.00 |

First Solar stock snapshot after recent performance

First Solar (FSLR) has drawn fresh attention after recent price moves, with the stock closing at US$214.57 and showing mixed returns over the past week, month and past 3 months.

For investors tracking longer horizons, the company’s total returns over the past year, 3 years and 5 years offer additional context alongside current valuation metrics and reported profitability.

Recent share price moves have been choppy, with an 11.6% 1-month share price return set against a 21.8% share price decline year to date. The 1-year total shareholder return of 60.4% points to stronger longer term momentum.

If you are looking for other opportunities tied to the energy and infrastructure theme, this could be a good moment to scan 36 power grid technology and infrastructure stocks

With First Solar trading at US$214.57, an indicated 13.1% intrinsic discount and a value score of 4, the key question is whether this setup signals a genuine buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 37.6% Overvalued

Compared with First Solar's last close at $214.57, the most followed narrative on the stock applies a fair value of $155.98, which frames the current premium investors are paying.

Known for its high quality solar panels and government cooperation during the Biden administration, First Solar is a strong company when it comes to maintaining its operations and innovating on solar energy. Our team believes that First Solar is considerably below its fair value. The current semi bear market present in the US markets caused by President Trump’s tariffs and trade war threats has caused negative sentiments in the market which overall reflected on First Solar’s stock price causing it to drop below its fair price.

Curious how this narrative reaches its fair value? It leans heavily on expanding margins and confident long term revenue compounding, then layers on a premium future earnings multiple. Want to see which specific profitability and growth assumptions do the heavy lifting in that model, and how sensitive the outcome is to even small changes in those inputs?

Result: Fair Value of $155.98 (OVERVALUED)

However, shifts in government policy or weaker demand for solar projects could pressure First Solar’s revenue growth assumptions and challenge the premium multiple in this narrative.

Another View: Earnings Multiple Sends a Different Signal

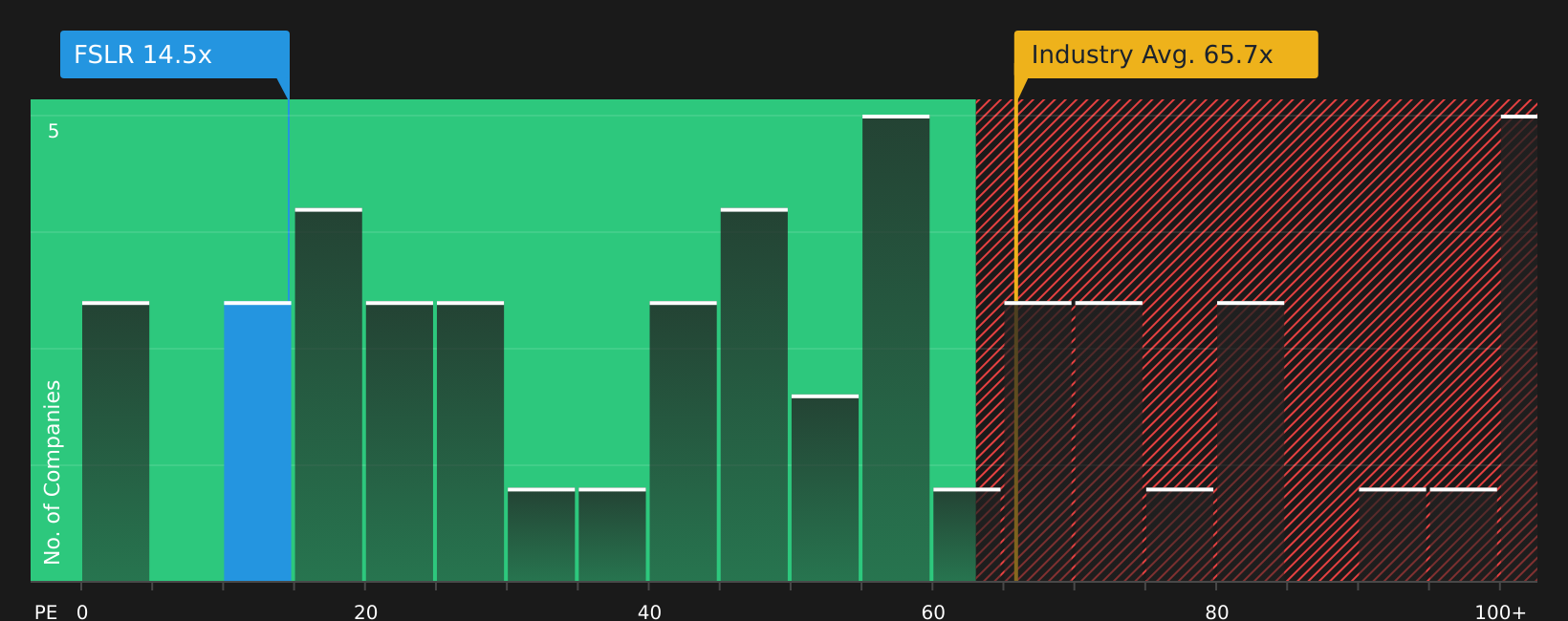

That 37.6% overvalued narrative sits awkwardly next to how the stock is priced on earnings. First Solar trades on a P/E of 13.8x, compared with 59.4x for the US Semiconductor industry and 90.8x for peers, while the fair ratio is 41.3x. That wide gap can look like a margin of safety or a sign the market is cautious. Which story do you think fits better?

Next Steps

With sentiment clearly split between valuation caution and earnings support, this is a good time to look at the numbers yourself, come to your own judgment, and then weigh both sides with 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with a single stock, you risk missing opportunities that better fit your goals, risk comfort and income needs across different parts of your portfolio.

- Pinpoint potential bargains by scanning 51 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their financial profile.

- Strengthen your core holdings by reviewing the solid balance sheet and fundamentals stocks screener (44 results) that can help support resilience when conditions get tougher.

- Spot earlier stage opportunities before they are widely followed by checking the 25 elite penny stocks with strong financials that already show stronger underlying financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.