A Look At Flagstar Bank (FLG) Valuation After Narrowed Net Loss And Turnaround Progress

Flagstar Financial FLG | 13.48 | +0.82% |

Flagstar Bank National Association (FLG) is back in the spotlight after reporting a net loss of US$177 million for 2025, lower than the prior year, along with reduced charge-offs and renewed attention from value-focused investors.

Investors appear to be weighing Flagstar’s smaller net loss and lower charge offs against its recent history. A 90 day share price return of 27.81% and a 1 year total shareholder return of 9.57% sit alongside a 3 year total shareholder return of 47.53% and a 5 year total shareholder return of 47.33%.

If Flagstar’s turnaround is on your radar, this could also be a good moment to widen your search and check out 23 top founder-led companies as potential next ideas to research.

With FLG trading at US$14.11 and only a small discount to the US$14.75 analyst target, yet still reporting a US$177 million loss, it is worth asking whether there is real value left here or whether the market is already pricing in future growth.

Most Popular Narrative: 2.4% Overvalued

Flagstar’s most followed narrative pegs fair value at $13.78, just below the recent $14.11 share price. The story therefore hinges on how its turnaround unfolds.

Systematic runoff and refinancing of low coupon multifamily and CRE loans, with proceeds redeployed into higher yielding C&I assets or used to retire high cost wholesale funding, should structurally expand net interest margin and enhance return on assets.

Read the complete narrative. Read the complete narrative.

Want to see what is baked into that fair value? The narrative leans heavily on faster revenue growth, sharply higher margins and a very different earnings profile by the outer years.

Result: Fair Value of $13.78 (OVERVALUED)

However, there is still a risk that credit normalization or weaker loan demand slows the C&I buildout and keeps earnings below the narrative’s expectations.

Another Angle: Book Value Paints a Different Picture

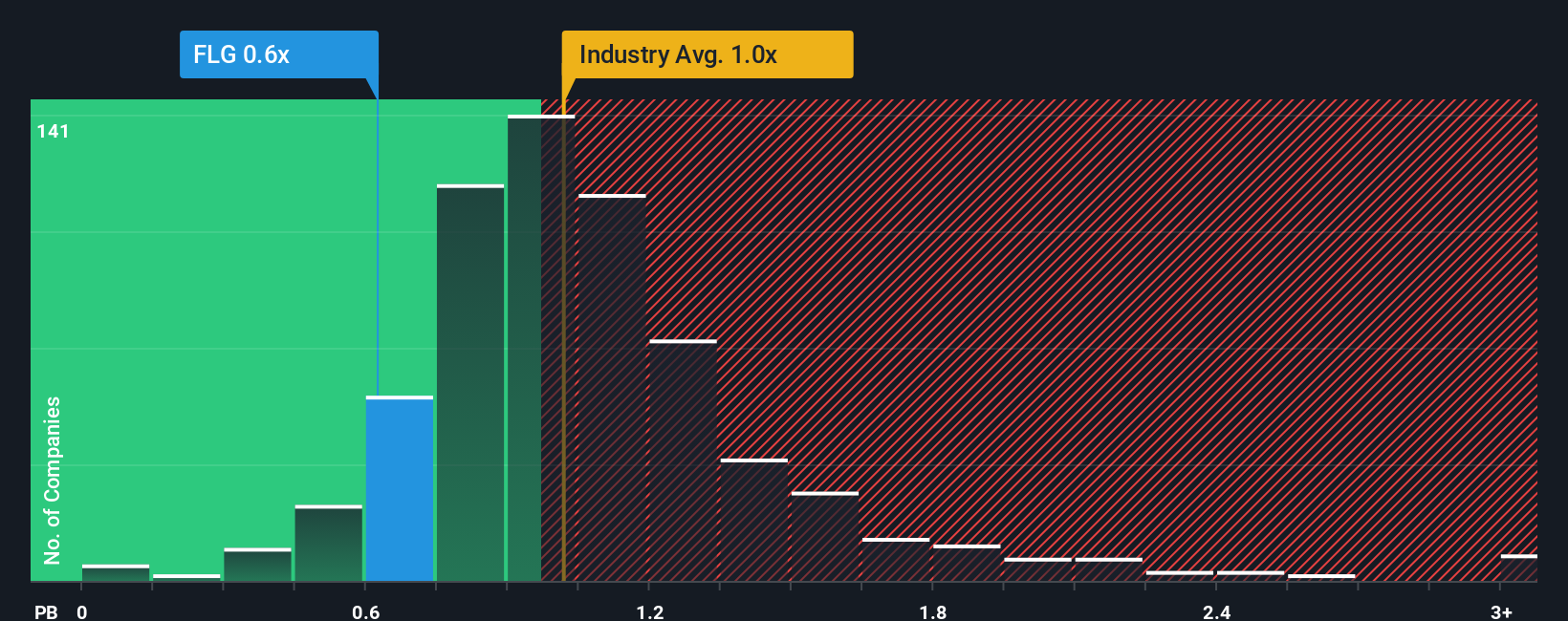

Analysts see FLG as slightly overvalued versus their $13.78 fair value, yet the current P/B of 0.8x sits below both the US Banks industry at 1.1x and peers at 1.3x. That discount hints at lower expectations. Is the market being cautious or overly harsh on future profitability risk?

Build Your Own Flagstar Bank National Association Narrative

If you are not fully on board with this view or prefer to weigh the numbers yourself, you can build a fresh narrative in minutes by starting with Do it your way.

A great starting point for your Flagstar Bank National Association research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Flagstar has sparked your interest, do not stop here. Broaden your watchlist with other clear setups that match the kind of opportunities you want to research next.

- Target potential mispricings by reviewing 51 high quality undervalued stocks that currently screen well on quality and price.

- Lock in income ideas by scanning 14 dividend fortresses that pair higher yields with stability characteristics.

- Reduce downside surprises by focusing on 83 resilient stocks with low risk scores built around resilient business and risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.