A Look At FLEX LNG (FLNG) Valuation After New Contracts And Dividend Commitment

FLEX LNG LTD (BM) FLNG | 0.00 |

FLEX LNG (FLNG) has drawn fresh attention after management flagged new contracts during the Iran war and reiterated plans to maintain its dividend, supported by a modern, largely contracted LNG carrier fleet.

The recent contract wins and dividend guidance come against a backdrop of strong share price momentum, with a 30 day share price return of 11.87% and a year to date share price return of 32.59%. The 1 year total shareholder return of 52.22% and 5 year total shareholder return, which is a very large multiple of the starting point, suggest the stock has rewarded long term holders.

If these moves in LNG shipping have your attention, it could be a good moment to widen your research and uncover 19 top founder-led companies

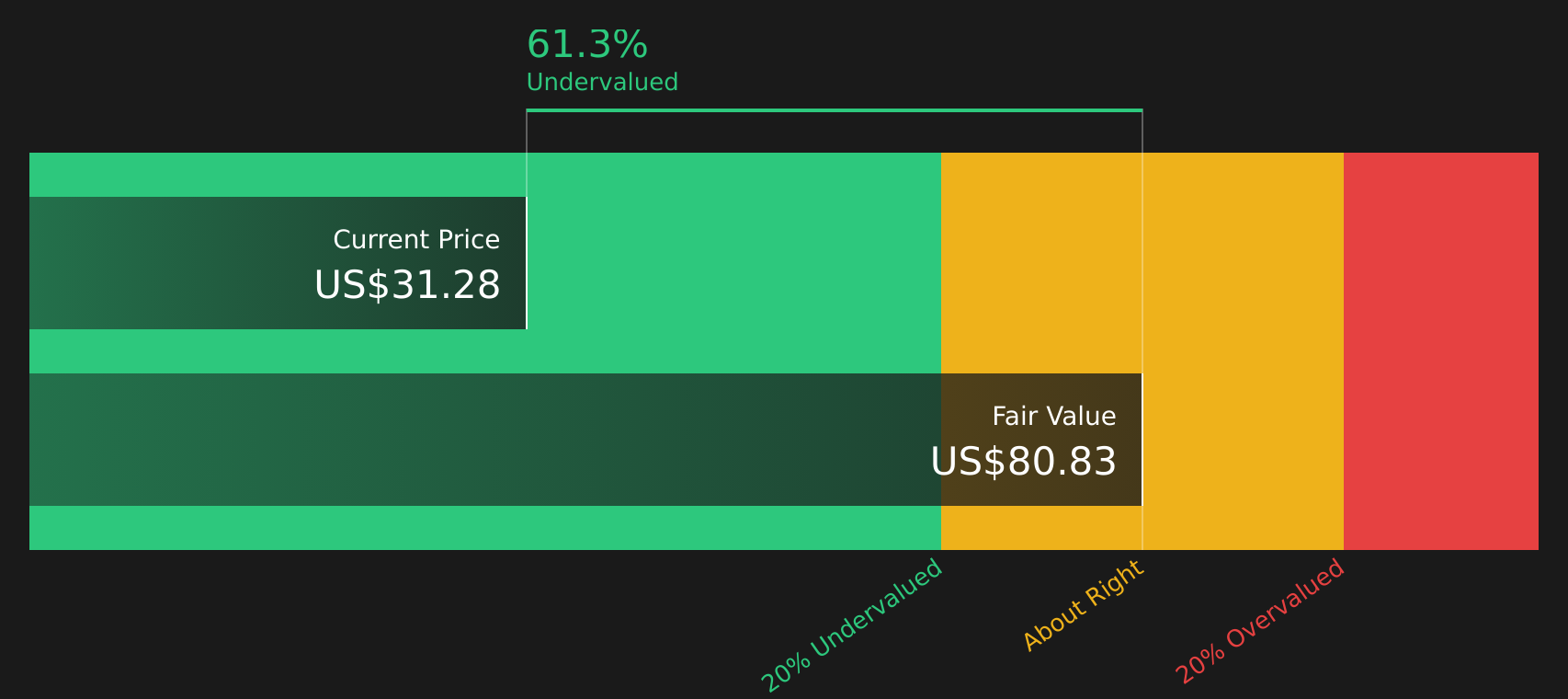

With FLEX LNG trading at US$32.71 and an intrinsic value estimate indicating a large discount, yet sitting above the average analyst price target, readers may ask whether there is still a buying opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 26.9% Overvalued

The most followed narrative puts FLEX LNG's fair value at $25.78 per share, which is well below the last close at $32.71, setting up a clear valuation gap to unpack.

The company's multi-year contract backlog (56 years minimum, up to 85 years with options) and long-term charters secure steady revenue and earnings despite short-term market softness, positioning FLEX LNG to benefit as global LNG trade volumes are projected to rise due to new export capacity coming online, particularly from the US, Qatar, and Africa, boosting future cash flow visibility and net margin stability.

Curious how that backlog translates into the fair value number? The narrative leans heavily on steadier margins, modest revenue growth, and a lower future earnings multiple. The detailed forecasts behind those levers are where the story really gets interesting.

Result: Fair Value of $25.78 (OVERVALUED)

However, this hinges on LNG shipping staying tight, and a large wave of new vessels or weaker imports in key markets like China and India could quickly challenge that view.

Another View: Cash Flows Point the Other Way

While the popular narrative frames FLEX LNG as 26.9% overvalued at a fair value of $25.78, the SWS DCF model presents a different perspective, with an estimated future cash flow value of $112.90 per share. That suggests investors need to decide which set of assumptions feels more realistic.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out FLEX LNG for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals on value and outlook, you do not want to just rely on headlines. Instead, move quickly, review the data for yourself, and weigh up the 2 key rewards and 3 important warning signs.

Ready to hunt for more investment ideas?

If FLEX LNG has sharpened your focus, do not stop at one stock. Use powerful screeners to quickly surface other opportunities that could fit your checklist.

- Target potential mispricings by scanning 48 high quality undervalued stocks that combine quality fundamentals with discounted valuations.

- Build a sturdier core by focusing on companies in the solid balance sheet and fundamentals stocks screener (44 results) that may better withstand tough conditions.

- Get ahead of the crowd by combing through a screener containing 21 high quality undiscovered gems before everyone else starts paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.