A Look At FLEX LNG (FLNG) Valuation After New Long Term Charter Backlog Expansion

FLEX LNG LTD (BM) FLNG | 30.57 31.20 | +0.33% +2.06% Pre |

Event overview and why it matters for FLEX LNG (NYSE:FLNG) investors

FLEX LNG (NYSE:FLNG) recently received a new commitment from a supermajor that extended time charters for Flex Resolute and Flex Courageous and confirmed a 15-year contract for Flex Constellation.

These moves secure employment on firm contracts for the two vessels until at least early 2032 and for Flex Constellation until at least 2041, which provides clearer visibility on future LNG shipping revenues.

The new long-term charters arrive as FLEX LNG’s share price trades at US$30.89, with a 30 day share price return of 12.37% and a 1 year total shareholder return of 54.03%, indicating strong momentum supported by clearer contracted revenue visibility.

If this kind of contract driven story interests you, it could be worth broadening your search using a screener focused on 25 power grid technology and infrastructure stocks

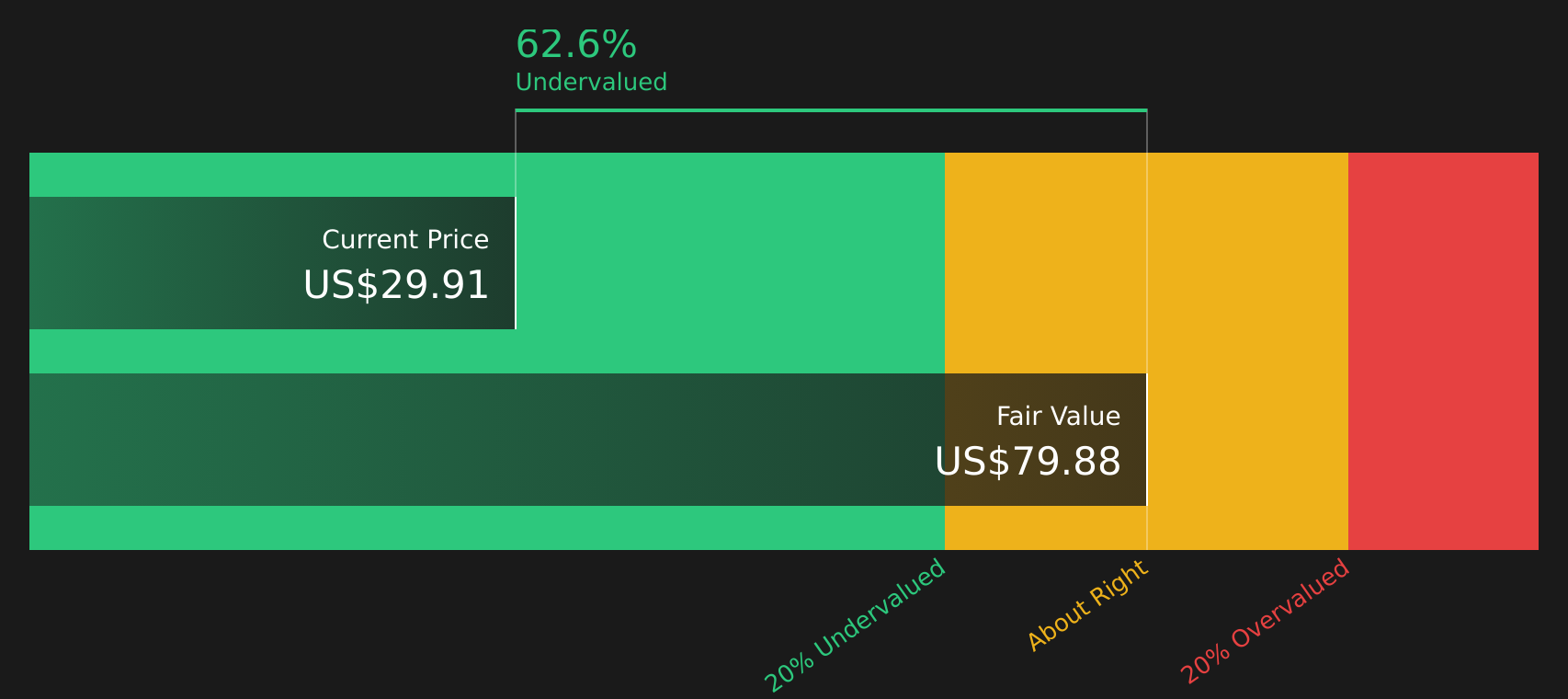

With FLNG trading at US$30.89 and an indicated intrinsic discount of 71%, the question is whether this contract backlog is still underappreciated or whether the market has already priced in years of future growth.

Most Popular Narrative: 22.3% Overvalued

FLEX LNG's widely followed narrative sets a fair value of $25.25, which sits below the latest close at $30.89, so the story leans toward a premium price.

The company's multi-year contract backlog (56 years minimum, up to 85 years with options) and long-term charters secure steady revenue and earnings despite short-term market softness. This positions FLEX LNG to benefit as global LNG trade volumes are projected to rise due to new export capacity coming online, particularly from the US, Qatar, and Africa, boosting future cash flow visibility and net margin stability.

Curious what kind of revenue path and margin profile justify that fair value and discount rate combo? The narrative leans heavily on contracted earnings and a future profit multiple that is not especially punchy on its own.

This most popular narrative blends relatively modest revenue expectations with a stronger earnings ramp, helped by wider margins and a higher return on equity forecast. It also relies on a single discount rate assumption to convert those future numbers into that $25.25 figure, which is well below the current share price of $30.89.

Result: Fair Value of $25.25 (OVERVALUED)

However, this story can be knocked off course if the expected LNG demand does not materialize, or if the wave of new vessels pressures charter rates.

Another way to look at FLEX LNG’s value

The earlier narrative leans on a fair value of $25.25 derived from earnings forecasts and a single future P/E. Our DCF model paints a very different picture, with an estimated future cash flow value of $108.12, which implies FLEX LNG is trading at a substantial discount.

That kind of gap often comes down to what you believe about contract durability, reinvestment choices, and long term LNG demand. If the cash flows in the SWS DCF model look reasonable to you, the question is how long the market might take to close that valuation gap, if at all.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out FLEX LNG for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of contract strength, differing valuation models, and mixed sentiment on risks and rewards gives you plenty to weigh up. Do not wait to review the underlying numbers and form your own judgment with the help of our breakdown of 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing opportunities that better match your goals, risk comfort, and income needs, so widen your search thoughtfully.

- Target quality at a discount by checking companies in the 58 high quality undervalued stocks that pair strong fundamentals with prices below their estimated worth.

- Strengthen your portfolio’s resilience by scanning the 73 resilient stocks with low risk scores for businesses with lower risk scores and steadier profiles.

- Hunt for future standouts before they hit the spotlight by reviewing the screener containing 25 high quality undiscovered gems packed with underfollowed companies backed by solid numbers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.