A Look at Four Corners Property Trust’s Valuation After Latest Property Acquisition and Stronger Quarterly Results

Four Corners Property Trust, Inc. FCPT | 23.52 23.52 | -0.55% 0.00% Post |

Four Corners Property Trust announced the acquisition of an SCA Health property in Alabama for $3.9 million, secured under a triple net lease. This move comes as the company reports stronger revenue and net income this quarter.

Four Corners Property Trust’s recent property acquisition and solid earnings update come as the stock has been working to regain momentum. While its share price picked up 1.85% in the past day and 2.24% over the week, the bigger picture tells a mixed story. The stock has seen a 9.85% share price decline year-to-date but a positive total shareholder return of 5.57% over three years, suggesting the long-term outlook remains constructive even as short-term sentiment wavers.

If you’re on the lookout for compelling opportunities beyond real estate, now’s the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With the stock showing signs of recovery but still trading nearly 20% below the average analyst price target, the key question now is whether Four Corners Property Trust represents an undervalued opportunity or if expectations for growth are already reflected in the current price.

Most Popular Narrative: 16% Undervalued

Four Corners Property Trust closed at $24.17, with the most widely followed narrative setting fair value a meaningful step higher. This brings attention to the drivers underpinning that estimate.

The company's focus on acquiring and expanding high-quality, e-commerce resistant retail and essential service properties (such as quick service restaurants, automotive services, and medical retail) positions FCPT's tenant base to benefit from long-term growth in physical service retail, supporting future rental income and revenue stability.

Curious what stunned the narrative analysts? Clue: it’s all about projected revenue expansion and margins not typically seen in this space. Find out which bold estimates form the backbone of this valuation. The math behind this price is anything but ordinary.

Result: Fair Value of $28.88 (UNDERVALUED)

However, ongoing sector concentration and challenges related to accelerating acquisitions could weigh on revenue growth. These factors may act as important catalysts that test the current bullish narrative.

Another View: DCF Model Perspective

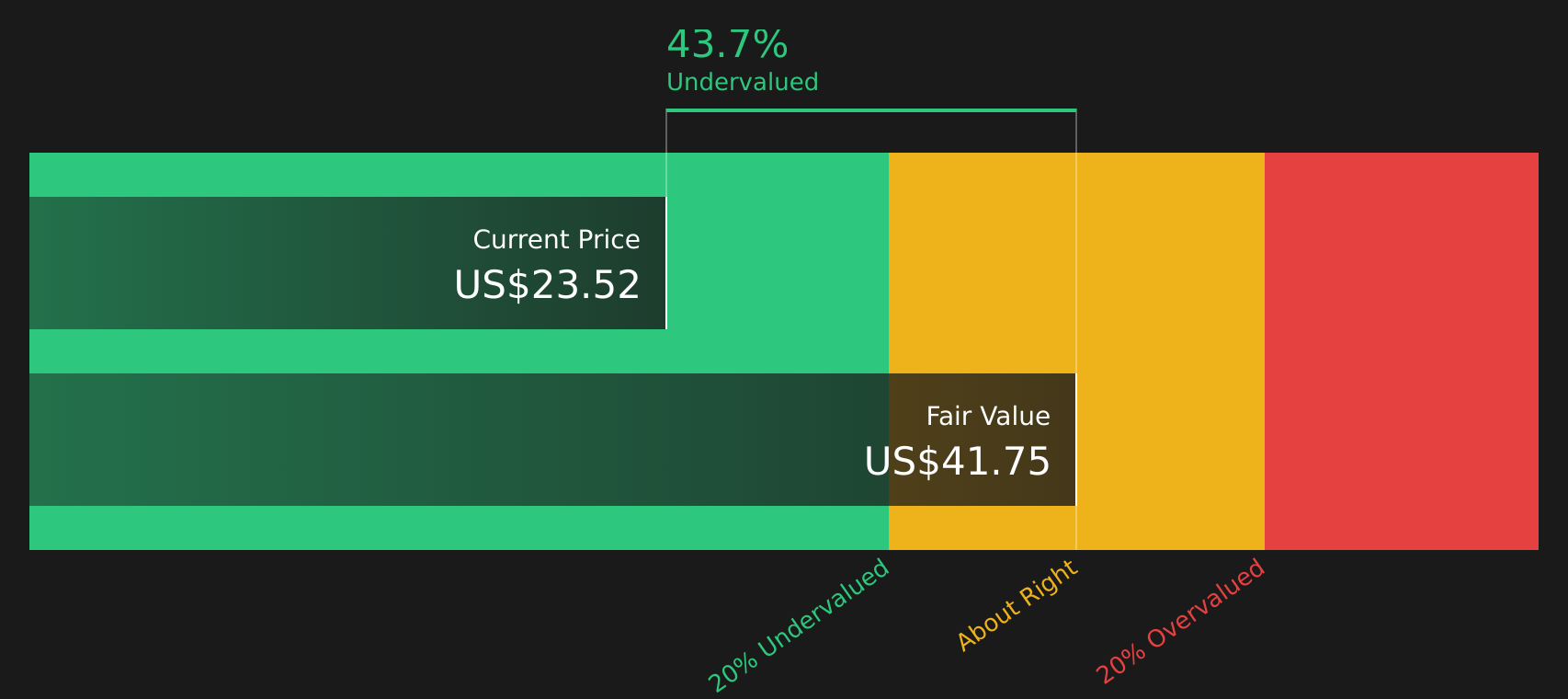

While the current valuation focuses on multiples, the SWS DCF model tells a different story. According to our DCF model, Four Corners Property Trust is trading roughly 44% below its estimated fair value. This suggests that the market may be underpricing its long-term cash flow potential. Could the DCF outlook reveal an overlooked opportunity?

Build Your Own Four Corners Property Trust Narrative

If the current perspective doesn't align with your own or you'd rather draw your own conclusions from the data, you can put together a personal narrative in under three minutes using Do it your way.

A great starting point for your Four Corners Property Trust research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Open up new opportunities and spot exceptional stocks with the Simply Wall Street Screener. Don’t let the next market mover pass you by.

- Tap into booming financial technology trends by tracking these 82 cryptocurrency and blockchain stocks as they make waves in digital payments and blockchain innovation.

- Unlock steady income potential with these 16 dividend stocks with yields > 3% which offer strong yields that can power your portfolio through any market conditions.

- Capitalize on tomorrow’s breakthroughs by following these 32 healthcare AI stocks that are transforming diagnostics, medical research, and patient outcomes through artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.