A Look At FTAI Aviation (FTAI) Valuation After Earnings Miss And Optimistic 2026 Guidance

FTAI Aviation Ltd. FTAI | 0.00 |

FTAI Aviation (FTAI) is back on traders’ radar after a Q4 2025 earnings miss was followed by a 6.14% share price jump, upbeat 2026 guidance, and fresh leadership appointments in key finance roles.

That Q4 earnings miss and the leadership reshuffle come after a strong run, with a 90 day share price return of 42.71% and a very large 3 year total shareholder return. The recent 7 day pullback of 8.13% looks more like a pause than a change in direction.

If FTAI’s move has you thinking about where growth and infrastructure demand might intersect next, it could be worth scanning our list of 24 power grid technology and infrastructure stocks as a fresh set of ideas.

With a 1 year total return above 150% and the share price sitting below some analyst targets and intrinsic estimates, is FTAI Aviation still trading at a discount, or are markets already pricing in the next leg of growth?

Most Popular Narrative: 46.5% Overvalued

According to Vestra’s widely followed narrative, FTAI Aviation’s fair value sits at $177.38, well below the last close of $259.91. This puts a spotlight on how ambitious the current pricing is.

FTAI Aviation is currently undergoing one of the most ambitious pivots in the aerospace sector, transitioning from a niche engine lessor into a high-tech energy and maintenance conglomerate. Trading at $260.35 as of the March 6, 2026 close, the stock has experienced significant volatility following its Q4 2025 earnings report on February 25. While the company reported a record full-year Adjusted EBITDA of $1.2 billion (a 38% year-over-year increase), it narrowly missed the quarterly EPS consensus, posting $1.08 against the $1.22 expected. This "miss" was largely attributed to aggressive reinvestment into its new FTAI Power segment and a ramp-up in inventory for its refurbished CFM56 engine modules.

Want to see how a fast growing earnings profile, heavy reinvestment, and an energy style re rating all feed into that $177.38 figure, and why Vestra believes the current price implies a very demanding execution path on those assumptions without spelling it out in the headline numbers?

Result: Fair Value of $177.38 (OVERVALUED)

However, there are clear pressure points, including execution risk around the FTAI Power build out and any setback in the CFM56 and V2500 aftermarket demand story.

Another Take: DCF Sees Upside

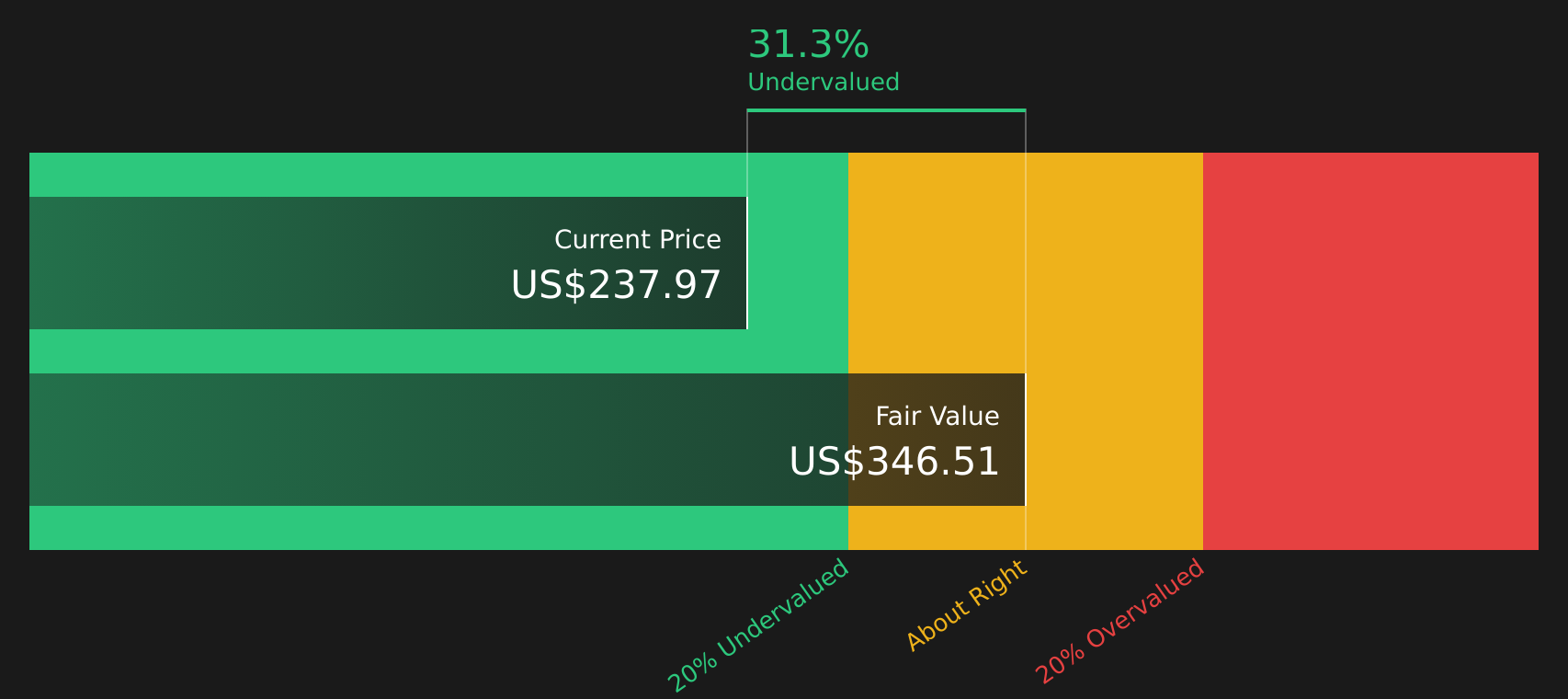

Vestra’s fair value of $177.38, based on a future earnings multiple, paints FTAI as overvalued. Our SWS DCF model points the other way, with an estimate of $411.65, which is 36.9% above the current $259.91 price. Two credible methods, one discount and one premium. Which story do you lean toward?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out FTAI Aviation for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With the story pulling in different directions, it makes sense to move quickly, review the numbers yourself, and weigh the balance of risks and rewards using 4 key rewards and 2 important warning signs.

Looking for more investment ideas?

If FTAI has sharpened your focus, do not stop here. Use the screener to line up fresh opportunities now so you are not reacting after the move.

- Target potential mispricings by scanning 50 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect them yet.

- Prioritise resilience first and sort through 67 resilient stocks with low risk scores that score well on stability and risk checks.

- Spot early stage opportunities by reviewing a screener containing 23 high quality undiscovered gems that many investors may not be watching closely yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.