A Look At FTAI Aviation (FTAI) Valuation As Artisan Trims Stake Over Data Center Power Concerns

FTAI Aviation Ltd. FTAI | 0.00 |

Institutional investor trims position as FTAI explores new power market

Artisan Small Cap Fund has started cutting its stake in FTAI Aviation (FTAI), pointing to what it sees as optimistic expectations around the company’s FTAI Power initiative and its data center power ambitions.

The move draws attention to how much value investors currently ascribe to FTAI’s plan to repurpose commercial jet engines for data center power generation, a business the fund expects could produce uneven and uncertain financial results over time.

At a share price of US$230.46, FTAI’s stock has pulled back recently, with the share price return down 7.01% over the past week and 14.74% over the past month, yet the 1 year total shareholder return of 86.19% and very large 5 year total shareholder return suggest long term momentum has still been strong.

If FTAI’s recent swing in expectations around data center power has caught your attention, it can be useful to compare it with other power and infrastructure related opportunities using our 35 power grid technology and infrastructure stocks

With FTAI trading at US$230.46 and compared with an average analyst price target of US$350.60, plus an indicated intrinsic discount of 32%, is the recent pullback a genuine opening or is the market already banking on future growth?

Most Popular Narrative: 2.4% Overvalued

According to the most followed narrative on FTAI Aviation, the fair value of $225.05 sits slightly below the last close of $230.46, framing the current pullback as a modest premium to that estimate.

FTAI Aviation is not a traditional aircraft lessor; it is evolving into a hybrid aerospace infrastructure and aftermarket platform.

Strengths: structural tailwinds, integrated model, aftermarket margins. Weaknesses: leverage, concentration, execution complexity. Key risk: dependence on aging fleet economics holding longer than expected.

Want to see what sits behind that price tag? The narrative leans heavily on engine scarcity, expanding aftermarket services, and a rich profit multiple to justify its view.

Result: Fair Value of $225.05 (OVERVALUED)

However, that premium view still hinges on aging engine economics and high leverage. Both of these factors could quickly challenge the narrative if conditions shift.

Another way of looking at FTAI’s value

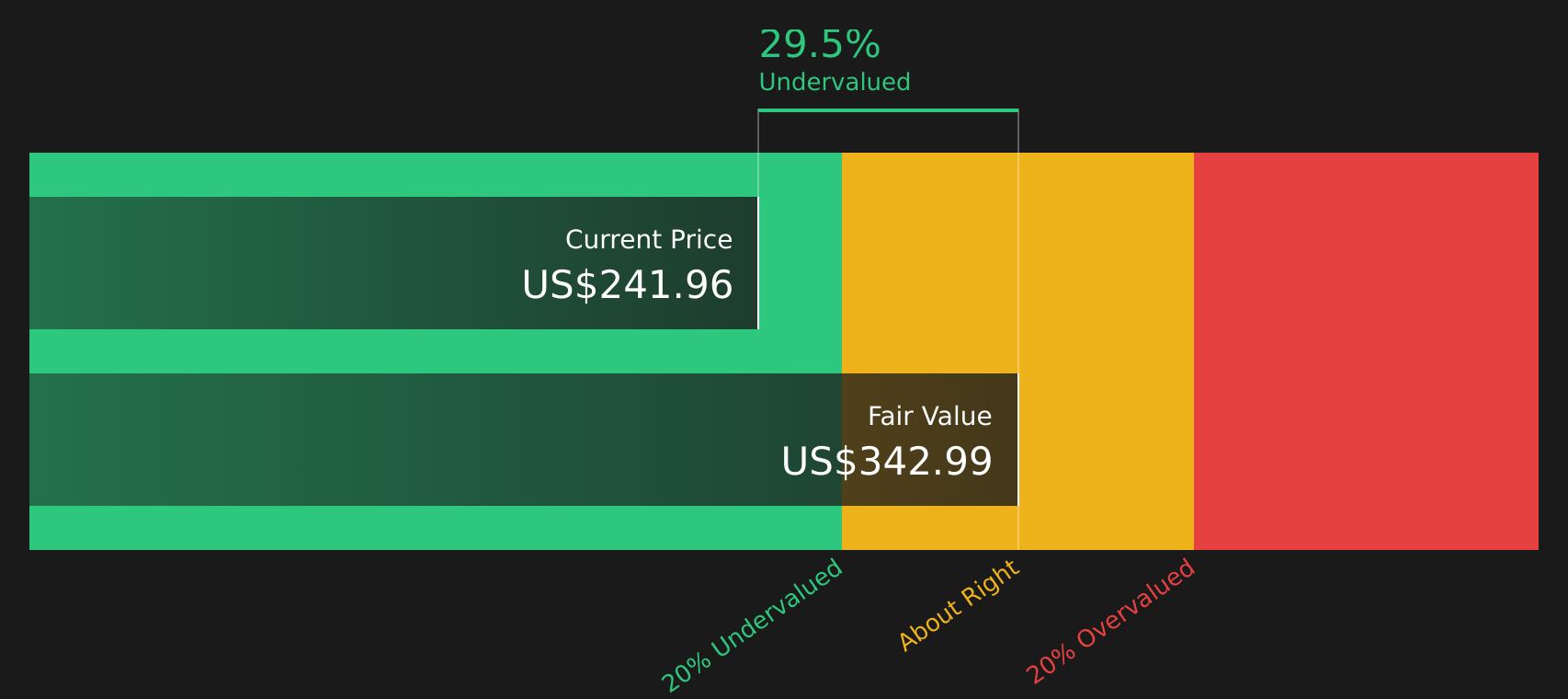

The user narrative tags FTAI as 2.4% overvalued at a fair value of US$225.05, but the Simply Wall St DCF model points the other way, with a future cash flow value of US$340.50 suggesting the stock is trading below that estimate. Which story seems more convincing to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out FTAI Aviation for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between opportunity and caution, this is a moment to move quickly and examine the data independently, beginning with the 4 key rewards and 3 important warning signs

Looking for more investment ideas?

If this story has sharpened your focus, do not stop here. The same tools can help you spot other opportunities that fit your style and risk comfort.

- Target stability by reviewing companies with strong finances and resilient balance sheets using the solid balance sheet and fundamentals stocks screener (46 results)

- Hunt for value by filtering for companies that pair quality fundamentals with prices that still look reasonable through the 47 high quality undervalued stocks

- Seek regular income by scanning companies that offer higher dividend yields and aim for staying power with the 10 dividend fortresses

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.