A Look At GXO Logistics (GXO) Valuation After Fortune World’s Most Admired Companies Recognition

GXO Logistics Inc GXO | 53.08 | -0.75% |

GXO Logistics (GXO) has just been named to Fortune’s list of the World’s Most Admired Companies for the first time, a recognition that has sharpened investor attention on the stock and its recent trading move.

The Fortune recognition comes as GXO’s share price has been relatively firm, with a 1 day share price return of 3.22% lifting the stock to US$56.82 and a 30 day share price return of 6.09%. Its 1 year total shareholder return of 26.01% contrasts with a more modest 3 year total shareholder return of 9.67%. This may suggest momentum has picked up recently as investors reassess its growth prospects and risk profile in light of both the accolade and operational changes such as the Lithia Springs job cuts.

If this kind of logistics story has your attention, it could be a useful moment to widen your search and check out fast growing stocks with high insider ownership.

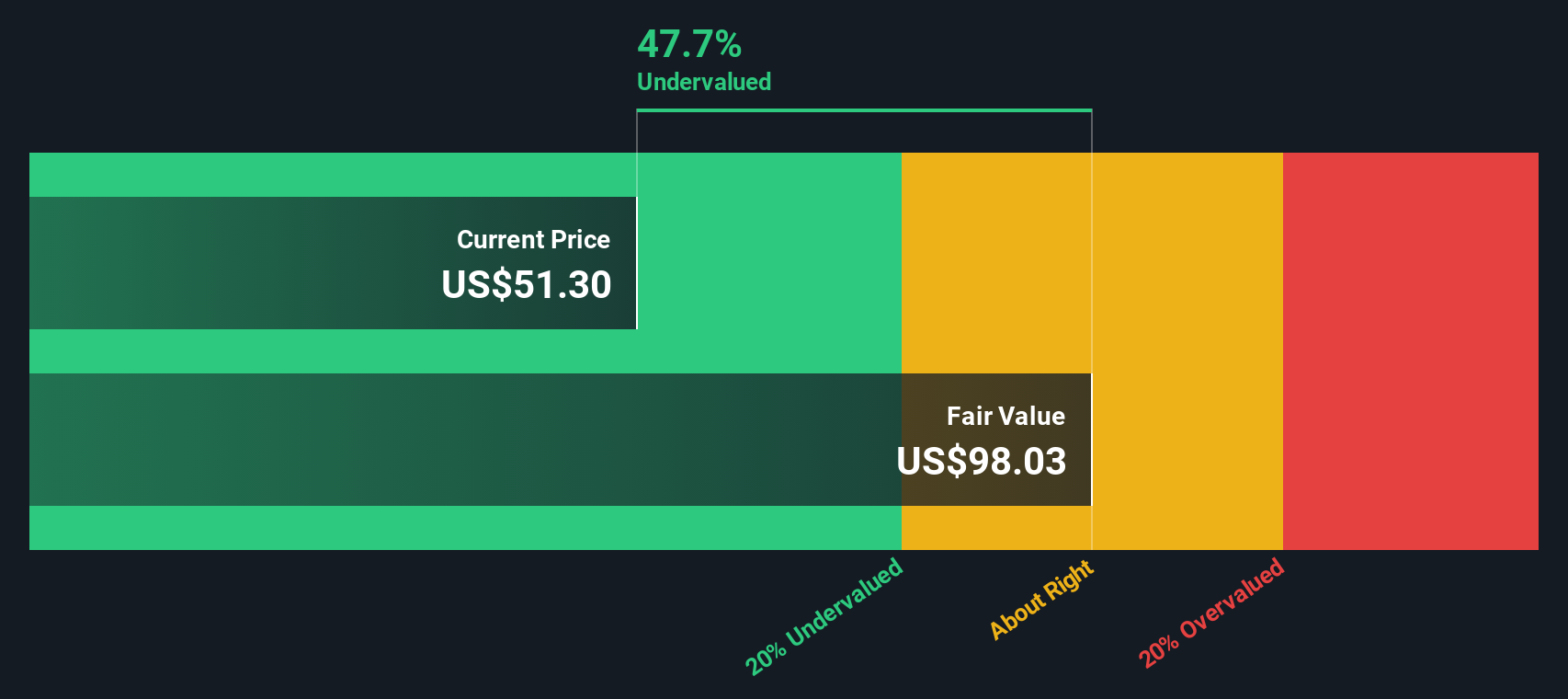

With GXO trading at US$56.82, only a small intrinsic discount indicated and the average analyst price target sitting higher at US$66.00, investors may ask whether there is still a buying opportunity or if future growth is already priced in.

Price-to-Earnings of 73.1x: Is it justified?

GXO currently trades on a P/E of 73.1x, a level that sits well above several benchmarks and raises questions about how much optimism is already in the price at US$56.82.

The P/E ratio compares the share price to the company’s earnings. A higher figure often reflects expectations for stronger profit growth or a higher quality earnings profile in future. For GXO, analysts are forecasting earnings to grow 61.1% per year, which can help explain why investors may be willing to accept a higher multiple today even though recent net profit margins sit at 0.7% and have moved below last year’s 1%.

Against the Global Logistics industry average P/E of 16.3x and a peer average of 25.7x, GXO’s 73.1x looks very rich by comparison. It is also above the estimated fair P/E of 41.1x, a level the market could move towards if expectations and reported earnings start to align more closely over time.

Result: Price-to-Earnings of 73.1x (OVERVALUED)

However, you still need to weigh risks such as a very high 73.1x P/E and thin net income of US$89m on US$12.9b revenue, which leave little room for setbacks.

Another View: DCF Suggests a Different Story

The 73.1x P/E makes GXO look expensive, yet our DCF model points to a different conclusion. At US$56.82, GXO is trading only 0.2% below an estimated future cash flow value of US$56.96, which appears roughly in line with fair value rather than stretched. Which signal matters more for you: earnings today or cash flows over time?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out GXO Logistics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 876 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own GXO Logistics Narrative

If you interpret the numbers differently or prefer to rely on your own research, you can build a fresh GXO thesis in minutes with Do it your way.

A great starting point for your GXO Logistics research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If GXO sparked your interest, do not stop here, broaden your watchlist with other focused ideas that could sharpen how you think about risk and opportunity.

- Zero in on potential value by scanning these 876 undervalued stocks based on cash flows that might offer more appealing cash flow profiles at current prices.

- Ride major tech shifts by checking out these 23 AI penny stocks positioned at the intersection of software, data and automation themes.

- Add diversification with income potential by screening these 13 dividend stocks with yields > 3% that already offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.