A Look At Hertz Global Holdings (HTZ) Valuation After Recent Share Price Volatility

HERTZ GLOBAL HOLDINGS, INC. HTZ | 5.11 | -1.35% |

Hertz Global Holdings (HTZ) has been drawing attention after its shares moved roughly 7% in the latest session. This has prompted investors to reassess recent performance, profitability trends, and the company’s current valuation profile.

That 7.1% 1 day share price return comes after a weaker stretch, with the 30 day share price return of 6.5% decline and 90 day share price return of 15.8% decline contrasting with a 23.0% 1 year total shareholder return. This suggests short term momentum has softened while longer term holders have still seen gains.

If this kind of volatility has you looking beyond car rentals, it could be a good moment to broaden your search and check out 22 top founder-led companies as potential fresh ideas.

Hertz now trades at US$5.29, with a recent 7% daily move, mixed short term returns, a 23.0% 1 year gain, and a low value score of 3. Is this pricing in future growth, or could there still be an opportunity?

Most Popular Narrative: 8.9% Overvalued

At a last close of $5.29 versus a narrative fair value of $4.86, Hertz Global Holdings is framed as slightly ahead of its implied worth, with that gap hinging on how its future earnings story plays out.

The company's transformation includes digital partnerships (e.g., with Cox Automotive and Amadeus) to modernize both vehicle sales channels and revenue management. This provides opportunities to boost utilization, optimize pricing, and increase total revenue per available car for the long term. Hertz's proven ability to sell vehicles profitably through retail channels, combined with strong relationships with OEMs, allows for flexibility in fleet management and persistent gains on sale. This improves resilience and supports higher future margins, even during vehicle supply disruptions.

Want to see what sits behind that fair value call? This narrative leans heavily on how margins, revenue trends and future earnings multiples could evolve. The exact mix of assumptions might surprise you.

Result: Fair Value of $4.86 (OVERVALUED)

However, if Hertz’s younger fleet keeps costs in check and its digital partnerships lift utilization and pricing, that 8.9% overvaluation call could face pressure.

Another View: Sales Multiple Paints a Different Picture

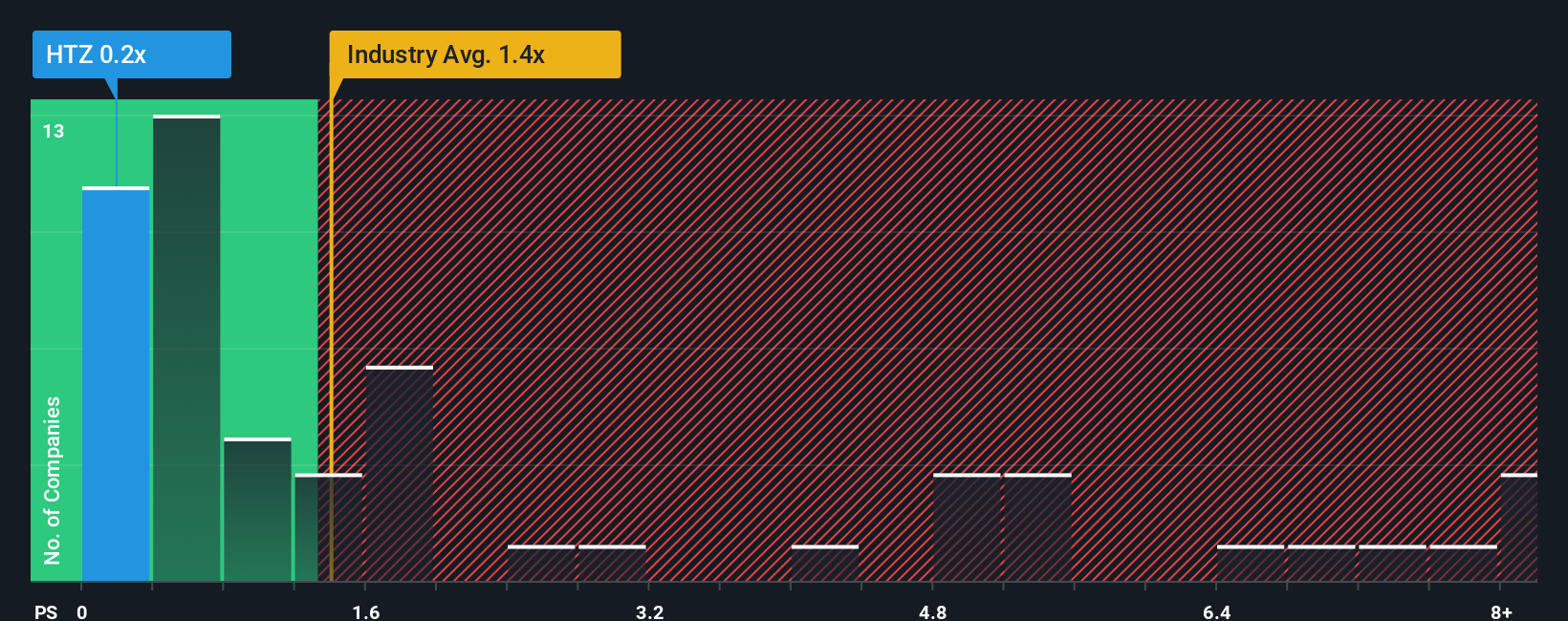

While the narrative fair value suggests Hertz Global Holdings is 8.9% overvalued at $5.29, its P/S ratio of 0.2x tells a different story. That is far below the US Transportation industry at 1.2x, the peer average at 2.1x, and even the fair ratio of 0.3x. The market could move toward that level over time.

If pricing ever shifted closer to that fair ratio, or even part of the gap to peers and the wider industry closed, the current tag might look quite different. So which signal do you treat as the one that really matters?

Build Your Own Hertz Global Holdings Narrative

If you see the numbers differently or prefer to weigh the assumptions yourself, you can build a custom Hertz view in just a few minutes by starting with Do it your way.

A great starting point for your Hertz Global Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Hertz has you rethinking where you put your money, this is your cue to scan other opportunities before the next move leaves you on the sidelines.

- Target potential mispricings by checking out 52 high quality undervalued stocks, built from companies that pair quality fundamentals with prices that may not fully reflect them.

- Strengthen your income stream with 14 dividend fortresses, focusing on businesses offering 5%+ yields and an emphasis on stability alongside payouts.

- Prioritize resilience first by reviewing 82 resilient stocks with low risk scores, a set of companies filtered for lower risk scores and steadier financial profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.