A Look at Hewlett Packard Enterprise (HPE) Valuation Following Cautious Outlook from KeyBanc After Strategy Update

Hewlett Packard Enterprise Co. HPE | 0.00 |

Hewlett Packard Enterprise (HPE) shares reacted as KeyBanc offered a cautious take following the company’s recent Strategic and Analytical Meeting. The brokerage voiced doubts about HPE’s long-term growth prospects, particularly in networking.

Even with several headline announcements this October, including a raised dividend, fresh earnings guidance, buyback expansion, and ongoing collaboration with Ericsson, HPE’s 12.7% share price return over the past quarter hints at recovering momentum. Its 22.4% total shareholder return for the past year underscores longer-term strength.

If you’re tracking technology sector shifts, it’s an ideal moment to discover other innovators using our tech and AI stocks screener: See the full list for free.

With HPE currently trading around a 13% discount to analyst price targets and boasting strong total returns, investors are left to consider whether the upside is still ahead or if the market has already factored in future growth.

Most Popular Narrative: 10.5% Undervalued

Hewlett Packard Enterprise’s latest fair value narrative points to a price target above the current share price, suggesting further upside potential. Investors are keen to see if evolving catalysts will play out.

"Strategic moves in AI, high-performance networking, and cloud services are enhancing HPE's market position, driving more predictable, higher-margin revenue streams. Operational efficiencies and cost-saving initiatives are expected to further improve margins, boost free cash flow, and support long-term earnings growth."

Want to know the playbook behind this high-stakes valuation call? The model’s bullish projections rest on ambitious growth in both earnings and margins, but also a shift in the business mix. Which future assumptions move the needle most? Dig deeper to untangle the precise financial leaps that justify this price target.

Result: Fair Value of $26.26 (UNDERVALUED)

However, lingering dependence on legacy hardware and uncertainty with Juniper integration could quickly shift sentiment if growth and margins disappoint investors.

Another View

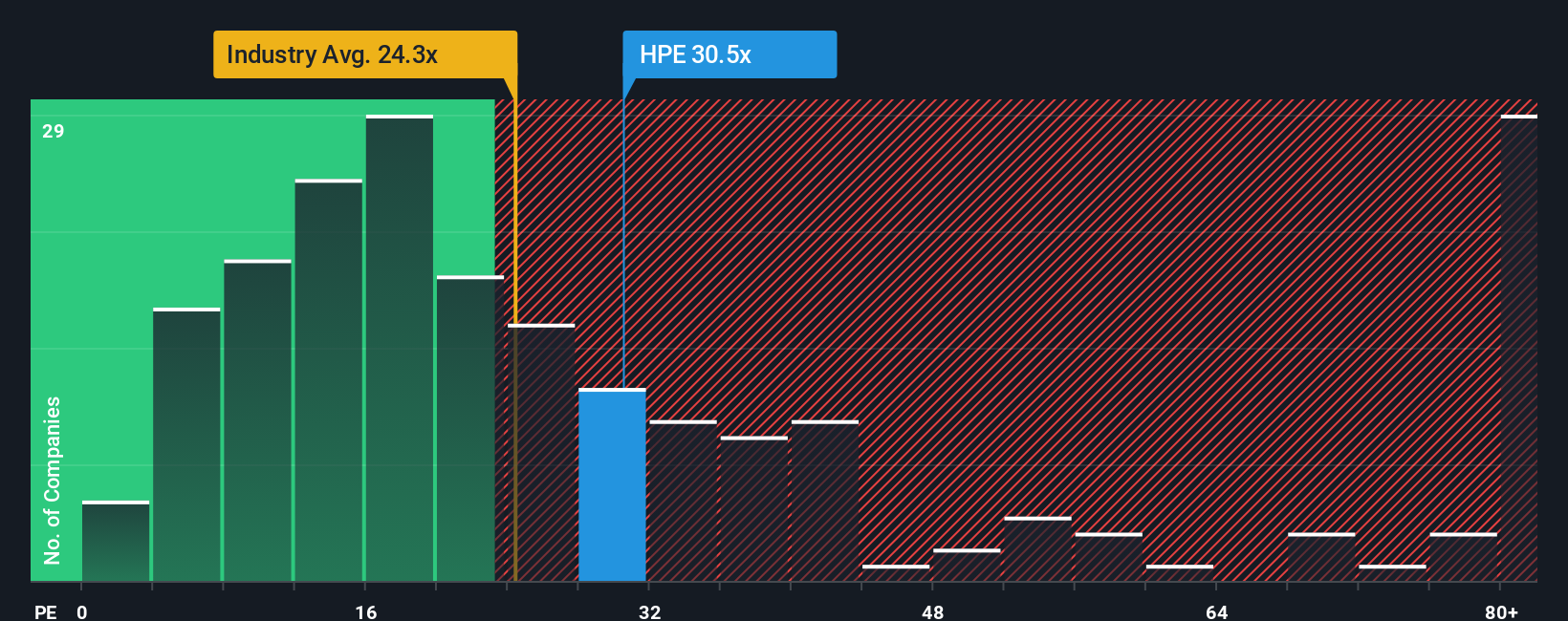

While the narrative points to HPE being undervalued, a glance at its price-to-earnings ratio introduces a different story. HPE currently trades at 27.3x earnings, which is noticeably higher than both the global tech peer average of 24.2x and its fair ratio of 47.1x. This premium suggests investors may already be betting on strong future results, raising questions about near-term upside versus valuation risk.

Build Your Own Hewlett Packard Enterprise Narrative

If you see the story unfolding differently or want to dive into the numbers on your own terms, you’re just a few minutes from shaping your own view. Do it your way.

A great starting point for your Hewlett Packard Enterprise research is our analysis highlighting 2 key rewards and 5 important warning signs that could impact your investment decision.

Ready for Your Next Smart Move?

Take your portfolio further by acting now. The best opportunities rarely wait around, so unlock new ideas with screeners tailored for ambitious investors.

- Capture potential in companies shaping tomorrow’s breakthroughs by starting with these 27 AI penny stocks. Get ahead of trends before the crowd.

- Maximize your search for strong income streams when you tap into these 17 dividend stocks with yields > 3%. This features stocks with yields over 3% and solid track records.

- Uncover hidden gems that could be trading below fair value by investigating these 872 undervalued stocks based on cash flows. Here, market mispricings present compelling chances every day.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.