A Look At Honest Company (HNST) Valuation After Analyst Downgrades And Diaper Competition Concerns

Honest Company, Inc. HNST | 2.82 | +1.44% |

JPMorgan’s downgrade of Honest Company (HNST) to Underweight, citing tougher diaper competition and pressure on pricing, has put the stock back in focus as investors reassess expectations ahead of upcoming earnings.

At a share price of US$2.49, Honest Company’s recent news has landed on an already weak trend, with a 30 day share price return of 10.75% and a 1 year total shareholder return decline of 62.16%, suggesting momentum has been fading as competition concerns gain attention.

If this kind of pricing pressure has you rethinking consumer names, it could be a good moment to broaden your search with fast growing stocks with high insider ownership.

With Honest Company trading at US$2.49 and sitting well below its average analyst price target, yet carrying a very low value score, you have to ask: is this punished consumer stock now mispriced, or already reflecting all the growth markets expect?

Most Popular Narrative: 35% Undervalued

The most followed narrative sees Honest Company’s fair value at about US$3.83 per share versus the last close of US$2.49. This frames the stock as discounted while still incorporating modest revenue and margin expectations.

Disciplined focus on operational improvements, margin enhancement, and tariff mitigation (evidenced by record gross margin, positive net income, and improved cost structure) is expected to further improve net margins and earnings resilience over the long term, especially as marketing and supply chain investments drive increased efficiency.

Curious how a business with pressured topline assumptions still lands on a premium earnings multiple? The narrative emphasizes margin rebuild and compounding profitability. Want to see exactly how those moving pieces stack up to support that fair value?

Result: Fair Value of $3.83 (UNDERVALUED)

However, softer revenue guidance and tariff exposure reaching US$8 million in 2025 could pressure margins and challenge the idea that earnings quality continues to improve.

Another View: Earnings Multiple Paints a Tougher Picture

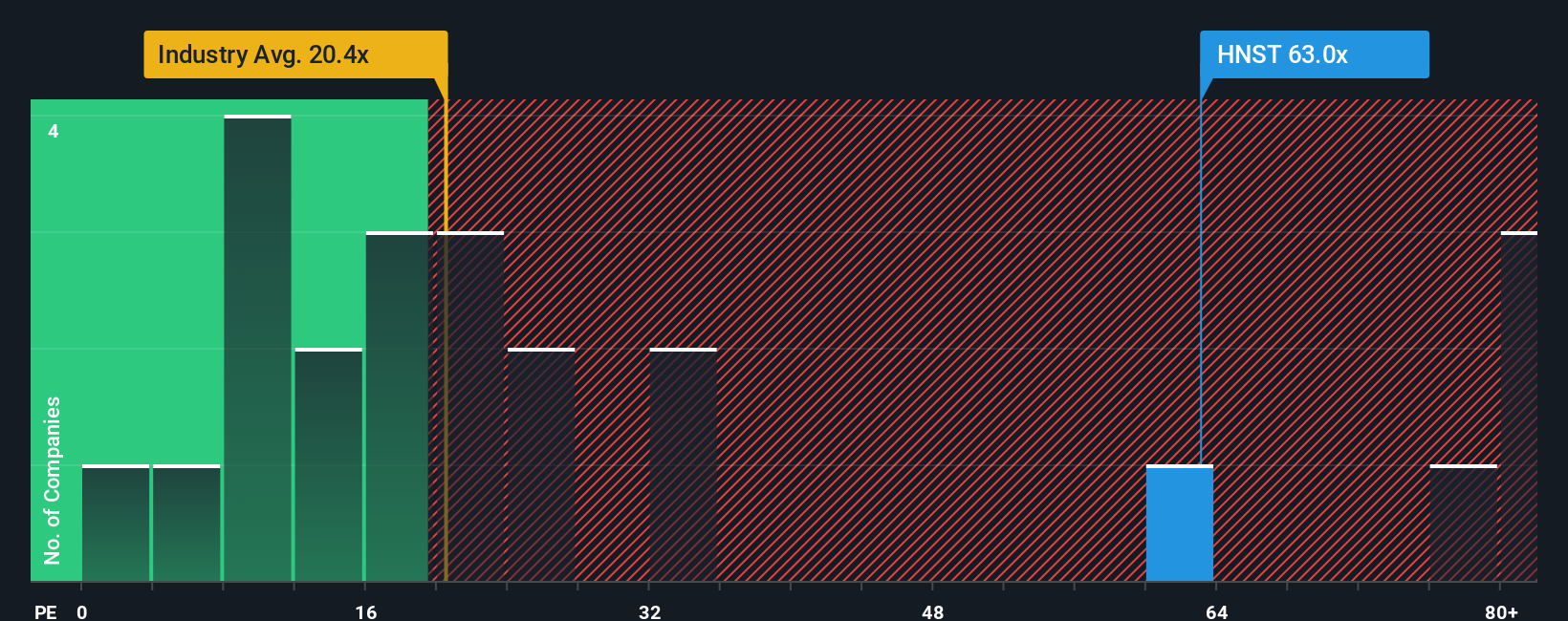

That 35% upside narrative sits awkwardly next to Honest Company’s current valuation. The shares trade on a P/E of 39.4x, compared with about 22x for the North American Personal Products industry, a fair ratio of 14.2x, and a peer average of 62.3x. The stock screens expensive versus the broader industry and the fair ratio, yet cheaper than its closer peers. Is this a setup for rerating risk, or a niche pocket where investors accept a premium?

Build Your Own Honest Company Narrative

If you see the numbers differently or want to stress test these assumptions yourself, you can spin up your own Honest Company narrative in just a few minutes, starting with Do it your way.

A great starting point for your Honest Company research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Honest Company has you rethinking where your capital works hardest, do not stop here. Widen your scope with curated stock ideas that might suit your style.

- Target potential mispricings by scanning these 875 undervalued stocks based on cash flows that line up price with underlying cash flows and fundamentals.

- Ride the next wave of automation and data-driven tools by checking out these 24 AI penny stocks that are building on artificial intelligence themes.

- Add income-focused names to your watchlist by filtering for these 12 dividend stocks with yields > 3% that clear a 3% yield hurdle.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.