A Look At Horace Mann Educators (HMN) Valuation After Strong Full Year Earnings And Profitability Improvements

Horace Mann Educators Corporation HMN | 43.21 | +1.05% |

Horace Mann Educators (HMN) is back in focus after reporting full year 2025 earnings, with revenue of US$1,701.4 million and net income of US$162.1 million, alongside commentary on stronger profitability.

At a share price of US$42.95, Horace Mann Educators has seen weaker short term momentum, with a 7 day share price return of 4.39% and a 30 day share price return of 3.44%. Its 1 year total shareholder return of 4.48% and 5 year total shareholder return of 34.77% reflect a steadier longer run outcome aligned with the recent earnings update and commentary around improved profitability, lighter catastrophe losses, and new partnerships such as Crayola.

If this earnings news has you thinking about where else growth and risk are shifting in financials, it could be a good time to scan 23 top founder-led companies as a fresh source of ideas.

With the shares at US$42.95, recent returns have been modest despite higher revenue and net income. This raises a key question for investors: is Horace Mann Educators still undervalued, or is the market already pricing in its future growth?

Most Popular Narrative: 13.5% Undervalued

Horace Mann Educators' most followed narrative points to a fair value of $49.67, compared with the last close at $42.95, putting projected fundamentals under the spotlight.

Extension of product offerings into supplemental and group benefits, combined with growing sales force and new partnerships (e.g., Crayola, Lakeshore Learning), is delivering record supplemental sales growth and helps diversify revenue streams away from core P&C, supporting both revenue growth and improved margin stability.

Curious what sits behind that valuation gap? The narrative focuses on steady revenue expansion, higher margins, and a future earnings multiple that is below many peers. The exact mix of growth, profitability, and discount rate assumptions might surprise you.

Result: Fair Value of $49.67 (UNDERVALUED)

However, the story can change if higher catastrophe losses return or if Horace Mann struggles to keep up with faster moving, tech led competitors.

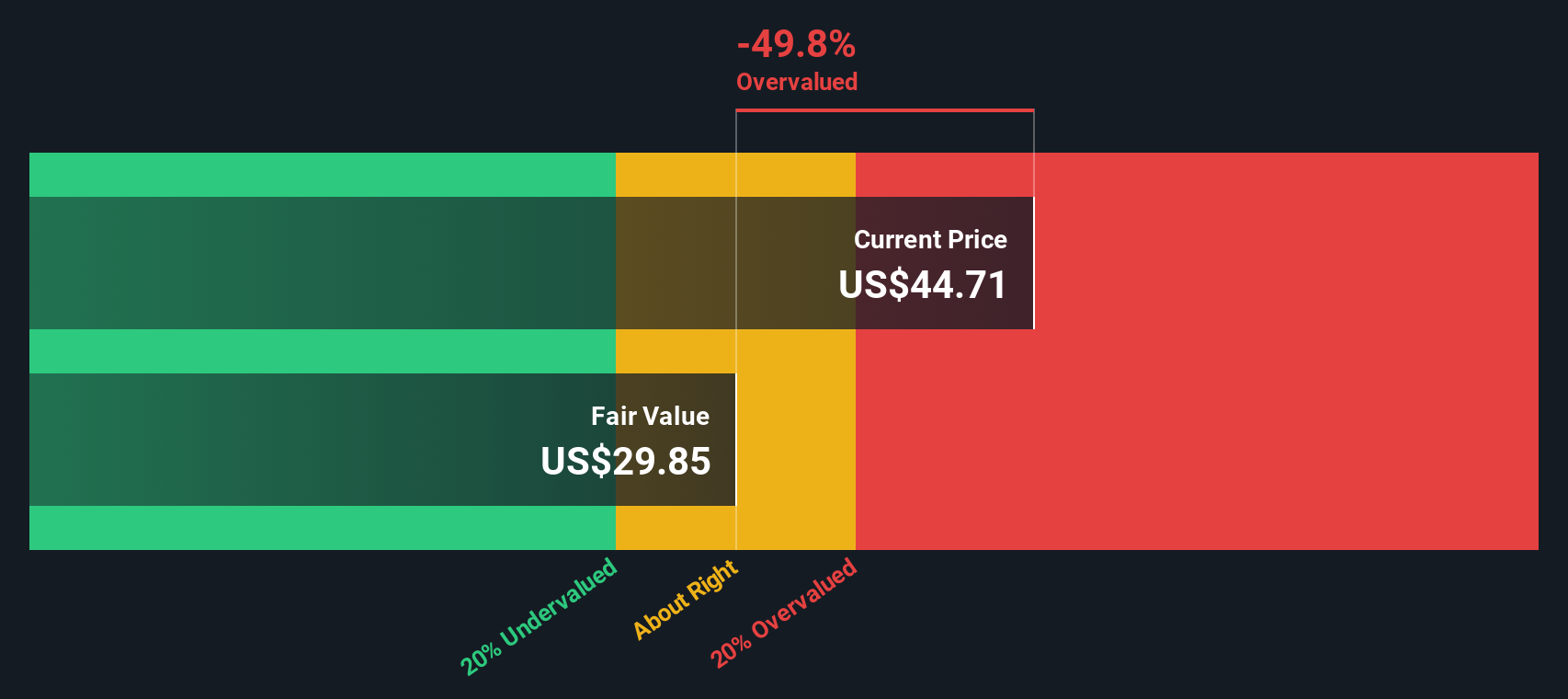

Another View: Cash Flows Paint a Different Picture

While the popular narrative points to a fair value of $49.67 using future earnings and a P/E of 10.8x, our DCF model points the other way, with an estimate of $27.52. On that basis, Horace Mann Educators at $42.95 screens as overvalued. Which story do you think is closer to reality?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Horace Mann Educators for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Horace Mann Educators Narrative

If you see the numbers differently or prefer to piece together your own view, you can shape a full thesis in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Horace Mann Educators.

Looking for more investment ideas?

If you want to widen your opportunity set beyond Horace Mann Educators, the Simply Wall St screener can quickly surface fresh stocks that fit your style and risk tolerance.

- Target value first by reviewing companies our tool flags as 51 high quality undervalued stocks, where solid fundamentals and pricing look out of sync.

- Prioritize resilience by checking out 83 resilient stocks with low risk scores, focused on businesses that score well on our risk checks.

- Spot tomorrow’s potential standouts early through our screener containing 24 high quality undiscovered gems, highlighting quality names that many investors may be overlooking right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.