A Look At Huntington Bancshares (HBAN) Valuation After Q4 Miss And Acquisition Driven Growth Outlook

Huntington Bancshares Incorporated HBAN | 15.79 | -0.57% |

Huntington Bancshares (HBAN) is back in focus after fourth quarter results came in slightly below analyst expectations, while management paired that short term disappointment with upbeat guidance tied to recent acquisitions.

The mixed reaction to earnings and acquisition updates has fed into recent trading, with a 1-day share price return showing a 6.02% decline and a softer 7-day share price return showing a 2.11% decline. However, the 90-day share price return of 9.77% and 5-year total shareholder return of 66.50% suggest longer term momentum has been stronger than the latest pullback.

If Huntington’s update has you thinking about where bank led growth or consolidation might show up next, it could be worth scanning fast growing stocks with high insider ownership as a way to spot other ideas on your radar.

With the shares pulling back after a modest earnings miss but trading below some analyst price targets and internal value estimates, you have to ask: Is Huntington quietly offering value here, or is the market already baking in that growth?

Most Popular Narrative: 13.7% Undervalued

Huntington Bancshares closed at $17.64, against a widely followed fair value estimate of $20.45, which frames the recent pullback in a different light.

The expansion into Texas via the Veritex acquisition, combined with ongoing organic growth in high-population-growth markets (Texas, North Carolina, South Carolina), is set to substantially increase Huntington's addressable market and fee-generating opportunities, likely driving higher revenue and earnings growth as these regions mature.

Curious how that expansion story translates into the $20.45 fair value? The narrative leans heavily on steady revenue compounding, firm profit margins, and a richer future earnings multiple. The exact mix of those inputs is where the real story sits.

Result: Fair Value of $20.45 (UNDERVALUED)

However, that potential value case could unravel if credit costs rise faster than expected, or if the Cadence and Veritex deals run into costly integration snags.

Another Angle On Valuation

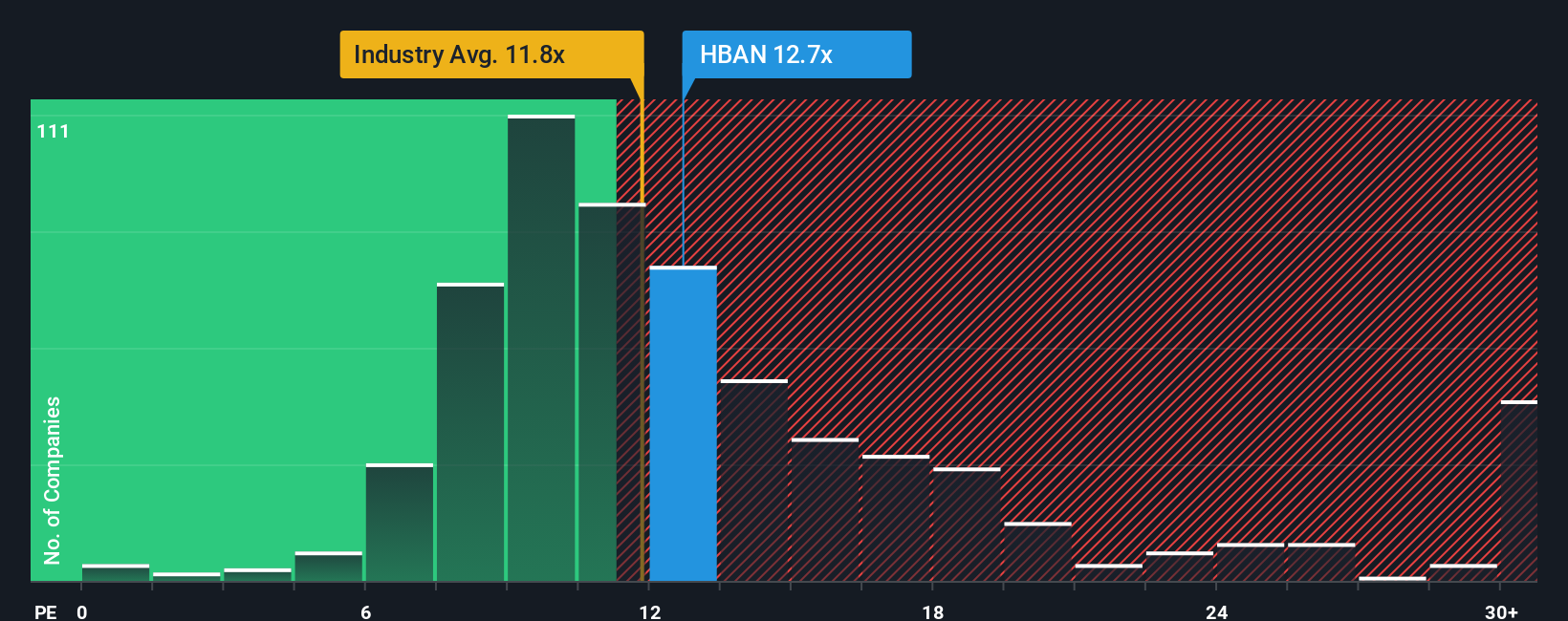

The first narrative leans on a fair value of $20.45, yet Huntington trades on a P/E of 13.1x versus 12.1x for the US Banks industry and a peer average of 13.3x. Our fair ratio of 17.4x points higher. This raises a practical question: is the bigger risk overpaying today, or underestimating what the market could pay later?

Build Your Own Huntington Bancshares Narrative

If you see the numbers differently, or want to stress test your own assumptions in just a few minutes, you can build a custom view with Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Huntington Bancshares.

Looking for more investment ideas?

If Huntington has sharpened your thinking, do not stop here. Widen your watchlist with focused stock ideas that match how you like to invest.

- Target potential mispricings by scanning these 878 undervalued stocks based on cash flows and see which companies line up with your view on value.

- Ride powerful tech trends by checking out these 24 AI penny stocks before the crowd chases the same themes.

- Put income at the center of your plan by reviewing these 12 dividend stocks with yields > 3% and weighing which yields fit your goals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.