A Look At Huntington Ingalls Industries (HII) Valuation As USS John F. Kennedy Begins Sea Trials

Huntington Ingalls Industries, Inc. HII | 396.62 | +0.84% |

Huntington Ingalls Industries (HII) is back in focus after the USS John F. Kennedy aircraft carrier left its Newport News Shipbuilding division for sea trials, a key milestone on a complex, long-cycle naval contract.

Those carrier sea trials come on top of recent progress across HII, including completion of builder’s sea trials for USS Zumwalt and new long term engineering work under the ATSP5 contract, alongside leadership changes at Ingalls Shipbuilding. Against that backdrop, the latest US$420.51 share price follows a 30 day share price return of 20.23% and a 1 year total shareholder return of 118.17%, suggesting momentum has been strong over both shorter and longer periods.

If shipbuilding milestones have your attention, this could be a useful moment to scan the wider defense space and uncover aerospace and defense stocks as potential ideas for your watchlist.

With HII trading at US$420.51 against an analyst price target of US$380.60 and an intrinsic value signal suggesting roughly a 9% discount, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 10.5% Overvalued

Huntington Ingalls Industries' most followed narrative sees fair value at $380.60, which sits below the latest $420.51 share price and frames the current debate.

The revitalization and expansion of the U.S. maritime industrial base, supported by increased outsourcing, supply chain stabilization efforts, and targeted workforce investments (notably effective wage increases and hiring), are enabling HII to execute a 20% throughput improvement plan, directly translating into enhanced cash flow and improved earnings consistency.

Want to see what is baked into that throughput story? The narrative leans on measured revenue growth, firmer margins, and a richer future earnings multiple. Curious how those pieces line up to reach that fair value mark?

Result: Fair Value of $380.60 (OVERVALUED)

However, that story can be knocked off course if large contract awards slip in timing, or if supply chain issues keep disrupting shipyard schedules and costs.

Another View: Earnings Multiple Points to More Neutral Pricing

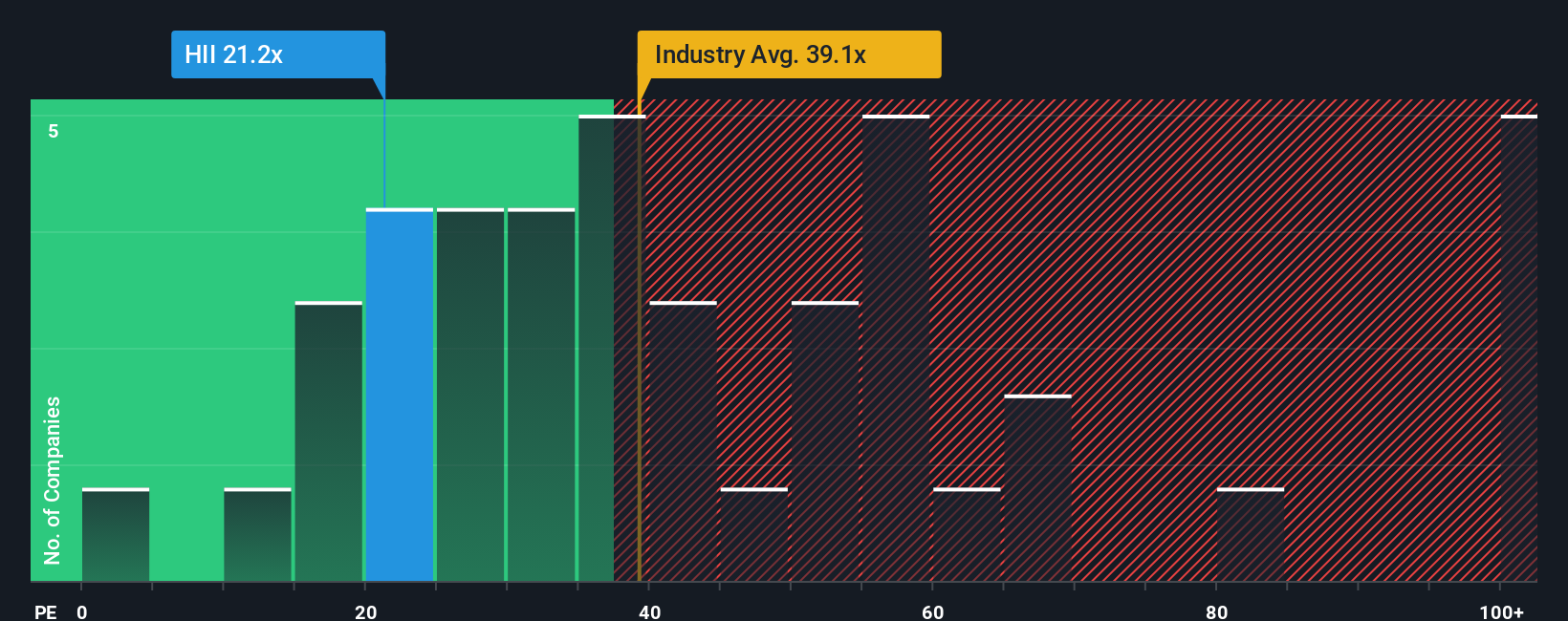

While the narrative fair value of $380.60 suggests Huntington Ingalls Industries looks 10.5% overvalued at $420.51, its valuation on earnings tells a calmer story. The current P/E of 29x sits below both peers at 37.8x and the industry at 41.6x, and very close to a fair ratio of 29.6x.

That gap is small, so instead of indicating that the stock is clearly cheap or expensive, it hints the market may already be weighing execution risks against recent share price strength. The question for you is whether that balance feels tight enough, or if you think sentiment could swing it one way or the other.

Build Your Own Huntington Ingalls Industries Narrative

If you see the numbers differently, or just want to stress test the assumptions yourself, you can spin up a fresh view and Do it your way in just a few minutes.

A great starting point for your Huntington Ingalls Industries research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If HII has you thinking more broadly about defense and beyond, this can be a smart moment to cast a wider net across other sectors and themes.

- Scan for potential mispriced names by checking out these 875 undervalued stocks based on cash flows that fit your view on fundamentals and cash flow strength.

- Approach the AI trend thoughtfully and see which companies stand out in these 110 healthcare AI stocks where technology and medical outcomes intersect.

- Explore emerging themes by reviewing these 18 cryptocurrency and blockchain stocks tied to digital assets, payment rails, and blockchain infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.