A Look At Hyatt Hotels (H) Valuation After Mixed Analyst Downgrades And Higher Target Estimates

Hyatt Hotels Corporation Class A H | 143.47 | -0.28% |

Analyst moves put Hyatt Hotels (H) back in focus

Recent analyst actions on Hyatt Hotels (H), including an Evercore ISI Group downgrade alongside higher internal estimates, have renewed attention on the stock and on how investors are weighing its risk and reward profile.

Hyatt’s 1 day share price return of a 1.0% decline and 7 day share price return of a 2.48% decline follow a recent intraday pullback and mixed analyst commentary. However, a 90 day share price return of 10.02%, a 1 year total shareholder return of 6.27%, and a 5 year total shareholder return of 152.50% indicate that long term momentum has remained stronger than the more recent price softness.

If this mix of short term swings and longer term gains has you thinking about opportunities beyond hotels, it could be a useful time to look at auto manufacturers as a different corner of the market.

With Hyatt shares easing from recent highs yet still showing solid multi year total returns, and analysts trimming ratings while lifting price targets, investors may reasonably ask whether this is a rare opening or if the market is already banking on future growth.

Most Popular Narrative: 7.4% Undervalued

Hyatt Hotels' most followed narrative places fair value at $176.83 per share versus the last close at $163.78, a gap that hinges on some punchy long term assumptions.

The strong development pipeline, with approximately 138,000 rooms and several new signings in diverse locations like India, Italy, and the U.S., is likely to drive revenue growth as these new properties come online.

Want to understand why this narrative still supports a higher price even with lower margin assumptions and a richer future earnings multiple? The entire case rests on robust top line expansion, shifting profitability expectations and a valuation multiple more often linked to faster growing sectors. Curious how those moving parts combine into that $176.83 fair value under a 9.45% discount rate? Read on and see what the full narrative is baking in.

Result: Fair Value of $176.83 (UNDERVALUED)

However, shifts in booking behavior and uncertainty around the Playa acquisition could challenge the revenue assumptions and the higher future P/E built into this story.

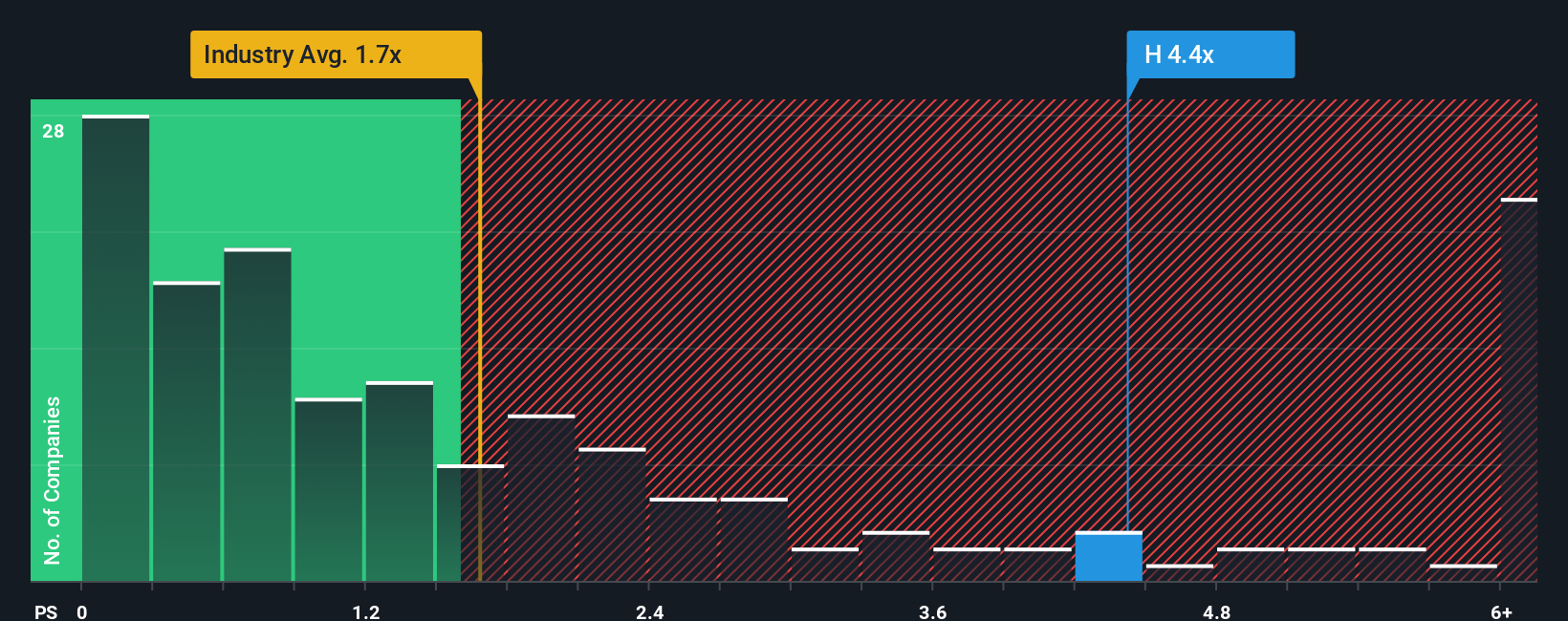

Another Angle: Rich Sales Multiple Rings Caution

Those 7.4% undervalued fair value claims sit alongside a very different signal from the market. Hyatt trades on a P/S of 4.7x, compared with a fair ratio of 3.7x, the US Hospitality average of 1.7x, and a peer average of 2.9x, which points to meaningful valuation risk if sentiment cools.

Build Your Own Hyatt Hotels Narrative

If you see the numbers differently or prefer to stress test every input yourself, you can rebuild the entire story in minutes with Do it your way.

A great starting point for your Hyatt Hotels research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Hyatt has your attention but you do not want all your research tied to a single name, broaden your watchlist now before the next move passes you by.

- Spot potential turnaround stories early by scanning these 3523 penny stocks with strong financials, which combine smaller market caps with stronger balance sheets and fundamentals than many expect.

- Zero in on future facing themes by checking out these 24 AI penny stocks, which sit at the intersection of artificial intelligence and fast changing software or hardware trends.

- Prioritise price discipline by working through these 864 undervalued stocks based on cash flows, which screens for companies trading below estimated cash flow based value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.