A Look At Ingevity (NGVT) Valuation After Its New Credit Agreement And Debt Repayment

Ingevity Corporation NGVT | 70.13 | -0.50% |

Why Ingevity’s new credit agreement matters for shareholders

Ingevity (NGVT) recently amended and restated its main credit agreement, extending the maturity of its revolving credit facility by five years, trimming total commitments to US$750 million, and updating interest terms.

At the same time, the company repaid US$512.1 million of outstanding revolving loans under the prior facility. This gives investors a clearer view of its current leverage, liquidity access, and banking relationships.

The refinancing news arrives after a strong run, with the share price up 18.3% over the past 90 days and a very large 105.1% 1 year total shareholder return. This suggests momentum has been building recently.

If this kind of repricing has you thinking about what else could be setting up for a strong run, it might be worth scanning 26 best rare earth metal stocks

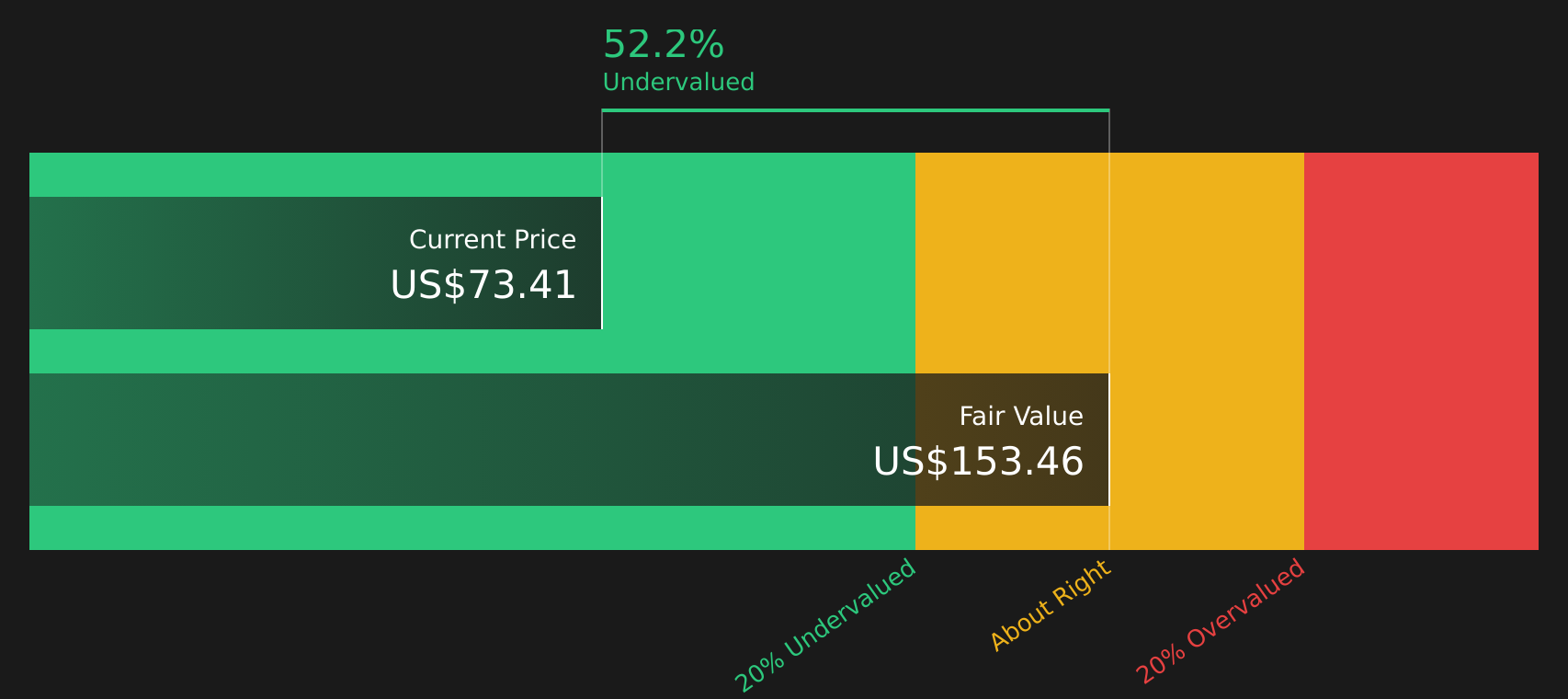

With the shares up sharply over the past year and trading at a discount to the US$79.25 analyst price target, the real question is whether Ingevity is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 10.3% Undervalued

At $71.09, the most followed narrative on Ingevity sets a fair value of $79.25, so the current price sits below that modeled outcome.

Accelerated portfolio repositioning and the advanced-stage divestiture of non-core, lower-margin businesses (Industrial Specialties and CTO refinery) are expected to drive a step-change in margin profile, enabling greater focus and capital allocation toward higher-growth, value-added specialty chemicals, supporting both revenue quality and sustained EBITDA margin improvement.

Want to see what kind of margin profile is embedded in that fair value, and how modest revenue growth still supports it? The full narrative lays out the cash flow path, profit mix shift, and valuation multiple that need to fall into place.

Result: Fair Value of $79.25 (UNDERVALUED)

However, there are clear pressure points, including the recent US$109.3 million impairment and ongoing APT margin strain, which could challenge the upbeat margin and earnings path.

Another way to look at valuation

The analyst narrative focuses on earnings and a fair value of $79.25. Our DCF model, however, indicates a higher potential valuation, with an estimated future cash flow value of $141.82 per share, which is very close to 100% above the current $71.09 price. This raises an important question: which perspective is more persuasive, the more conservative target or the cash flow calculations.

Next Steps

Seeing both risks and rewards in the story so far, it makes sense to move quickly and weigh the data for yourself using the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop with a single stock when you can quickly compare different return profiles, balance sheets, and income streams to see what really fits your plan.

- Zero in on potential mispricings by scanning companies that screen as high quality and potentially undervalued using the 62 high quality undervalued stocks.

- Prioritize resilience by focusing on businesses with stronger finances through the solid balance sheet and fundamentals stocks screener (39 results).

- Target steady income opportunities by reviewing companies highlighted in the 12 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.