A Look At Inspire Medical Systems (INSP) Valuation After CMS Reimbursement Uncertainty

Inspire Medical Systems, Inc. INSP | 0.00 |

Why CMS reimbursement changes matter for Inspire Medical Systems (INSP)

The latest clarification from the Centers for Medicare & Medicaid Services, which removes obstructive sleep apnea as a covered diagnosis for a key procedure code, has pushed Inspire Medical Systems (INSP) into the spotlight for reimbursement risk.

This policy shift has already led some Medicare Administrative Contractors to pull back a key billing code for the company’s hypoglossal nerve stimulation therapy. This has contributed to share price volatility, analyst downgrades, and new questions around future payments.

At a share price of US$79.40, Inspire Medical Systems has seen its 7 day share price return of 13.91% and 30 day share price return of 16.83% give way to a modest 90 day share price gain of 1.53%. The 1 year total shareholder return of 57.87% and 3 year total shareholder return of 68.65% point to a longer period of weaker performance, suggesting that recent CMS reimbursement headlines and guidance changes have reinforced concerns rather than sparked a sustained recovery in momentum.

If reimbursement risk has you reassessing healthcare exposure, this can be a useful moment to scan beyond a single name and look at healthcare stocks for fresh ideas in the sector.

With INSP trading at US$79.40 after a 1-year total shareholder return decline of 57.87% and at a discount of about 36% to the current analyst price target, are investors looking at a reset entry point or a stock already pricing in future growth?

Most Popular Narrative: 43.3% Undervalued

At $79.40 against a narrative fair value of about $140.13, the most followed storyline around Inspire Medical Systems centers on whether reimbursement and earnings strength can support that gap.

The recent delay in transitioning centers to the Inspire V next generation system including slower onboarding, delayed SleepSync implementation, and the Medicare billing update are transitory issues; as these barriers resolve (with Medicare billing now live and most centers expected to complete onboarding by end of Q3), procedure volumes and revenue growth are positioned to reaccelerate in 2026 as pent up demand is realized.

Curious how that story gets to a much higher fair value? The narrative leans on faster earnings growth, firmer margins, and a premium multiple that assumes real staying power.

Result: Fair Value of $140.13 (UNDERVALUED)

However, this story can break if Inspire V rollout setbacks persist or if reimbursement and coverage shift again, which would keep volume growth and margins under pressure.

Another View: High P/E Raises a Different Question

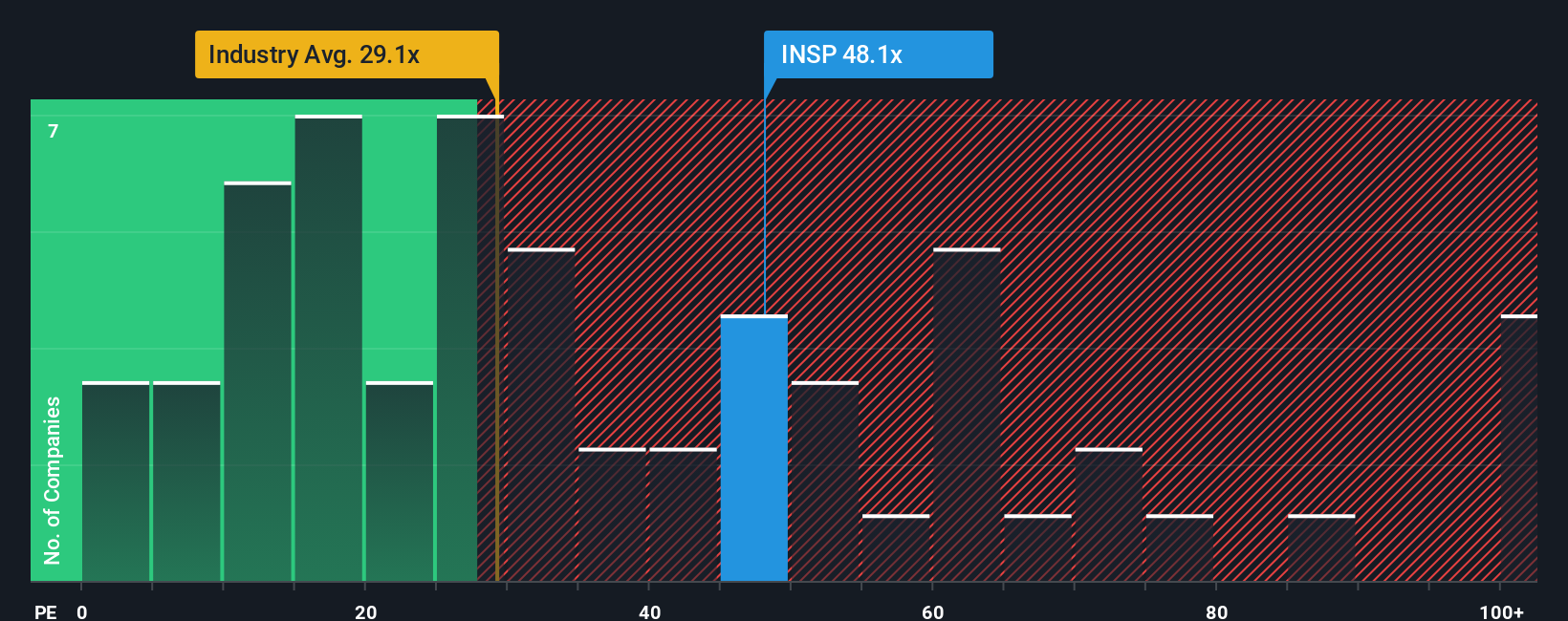

That $140.13 fair value assumes the market is comfortable paying up for future earnings. On today’s numbers though, INSP trades on a P/E of 51.8x, compared with 32x for the US Medical Equipment industry, a fair ratio of 23.8x and a peer average of 61.1x.

Those gaps suggest investors are already paying a premium price that could compress if expectations cool, even if peers stay expensive. The key question is how much valuation risk you are comfortable taking on here.

Build Your Own Inspire Medical Systems Narrative

If this view does not quite fit how you see Inspire Medical Systems, you can quickly test your own assumptions, shape a fresh thesis, and Do it your way

A great starting point for your Inspire Medical Systems research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas beyond Inspire Medical Systems?

If you are weighing reimbursement risk at INSP, do not stop here. Widen your watchlist with tools that help you spot other potential opportunities early.

- Spot potential bargains by scanning these 871 undervalued stocks based on cash flows that currently trade below what their cash flows may justify.

- Ride the wave of automation and data by checking out these 23 AI penny stocks shaping the future of artificial intelligence.

- Add income potential to your watchlist by reviewing these 13 dividend stocks with yields > 3% offering yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.