A Look At Intuitive Machines (LUNR) Valuation After Record Q1 Results And New Government Space Contracts

Intuitive Machines LUNR | 0.00 |

Intuitive Machines (LUNR) is back in focus after reporting first quarter 2026 results that paired record revenue and backlog with new NASA and U.S. Space Force contracts, as well as recently announced space infrastructure acquisitions.

The share price has been volatile around this news, with a 1-day share price return down 7.2% to US$33.89 after a sharp run that left the 90-day share price return at 103.91% and the 1-year total shareholder return at 179.62%. This points to strong momentum as well as shifting views on risk and future execution.

If fast moving space stocks like Intuitive Machines interest you, it can be worth widening the lens to other high growth themes and seeing which 42 AI infrastructure stocks fits your watchlist.

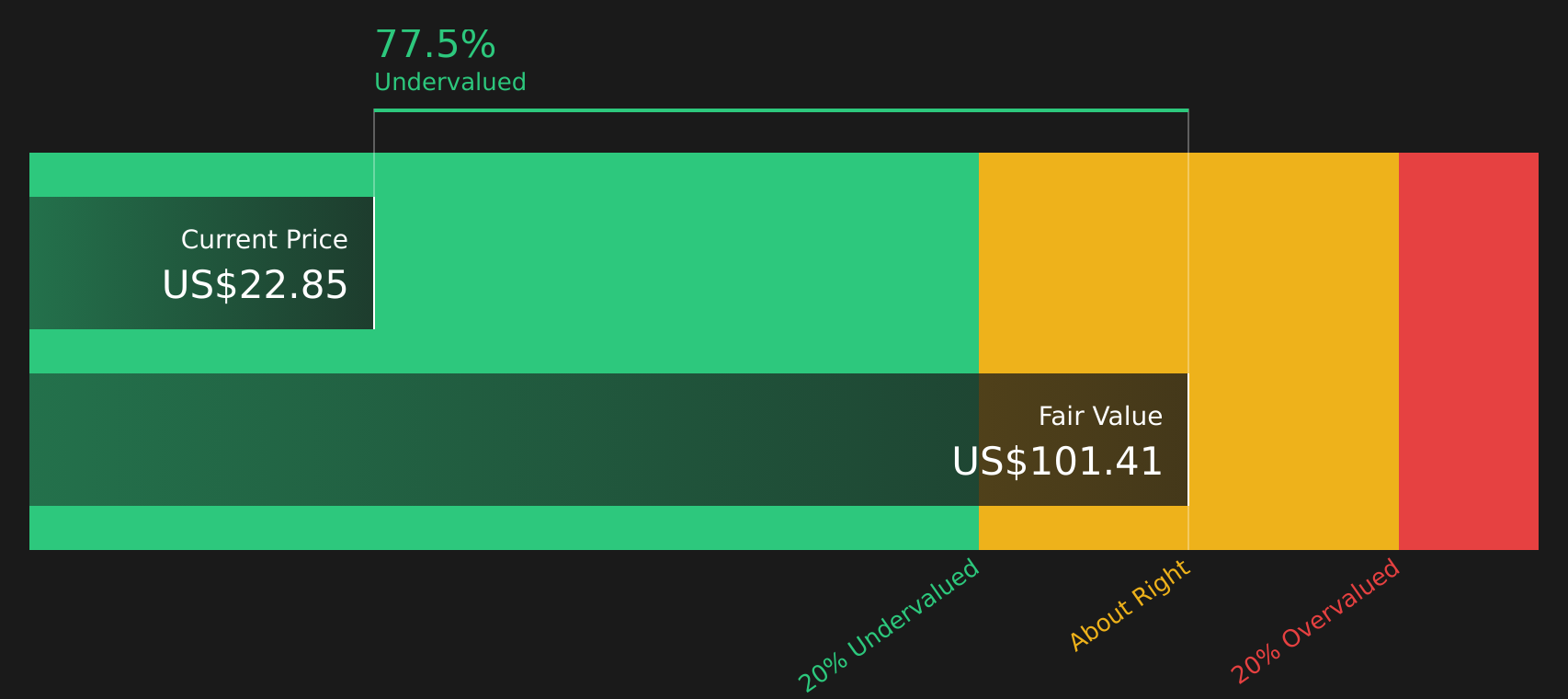

With Intuitive Machines now valued at about US$7.35b and trading only slightly below the average analyst price target, the key question is whether recent contracts and acquisitions leave upside on the table or if the stock already reflects future growth.

Most Popular Narrative: 47.3% Overvalued

At a last close of $33.89 versus a fair value of $23.00 from the most followed narrative, Intuitive Machines is framed as richly priced before factoring in recent volatility.

While LUNR’s 63.72% growth profile is fundamentally sound, the market is currently pricing in a flawless execution of every lunar mission. Considering the $15M in recent insider selling within the $23 to $25 range and the high 1.4 beta volatility, we view $23.21 as the objective "Going Concern" value. This provides a necessary buffer for investors against the inherent execution risks of the lunar economy.

Curious how a fast growing lunar services business still lands on a much lower fair value per share. The narrative hinges on ambitious revenue scale up, a shift toward higher margin data services and a much larger share count than many investors expect.

Result: Fair Value of $23.00 (OVERVALUED)

However, any slip in lunar mission execution or a slower shift into higher margin data services could quickly challenge assumptions behind the 47.3% overvaluation call.

Another View: Our DCF Points To Upside

That 47.3% overvaluation call based on a sales multiple meets a very different picture when using the SWS DCF model. On this view, Intuitive Machines at $33.89 is trading about 17% below an estimated future cash flow value of $40.94. This frames recent volatility as potential upside instead of excess and raises the question of which lens better fits how you think about risk.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Intuitive Machines for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals around value and risk, it helps to step back and weigh the full picture for yourself rather than follow the latest move. To see both sides laid out clearly, take a closer look at the 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If Intuitive Machines has sharpened your interest, do not stop here. Broaden your watchlist with a few focused ideas that many investors overlook.

- Spot potential high flyers early by scanning 28 elite penny stocks with strong financials that already show stronger balance sheets and fundamentals than typical micro caps.

- Hunt for quality at a reasonable price with the 51 high quality undervalued stocks that highlights companies combining healthier cash flows and sturdier financial positions.

- Prioritize resilience by checking the 66 resilient stocks with low risk scores featuring stocks with lower risk scores that may suit a steadier core portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.