A Look At iQIYI (IQ) Valuation As It Unveils Its First Offline Entertainment Park

IQIYI, INC. IQ | 1.39 | +0.72% |

iQIYI (IQ) has drawn new attention after announcing iQIYI LAND, its first offline entertainment park. It is set to open in Yangzhou in February 2026, timed around Chinese New Year travel demand.

The iQIYI LAND announcement comes as the stock trades at US$2.11, with recent momentum reflected in a 1-month share price return of 8.21% and a 7-day share price return of 4.46%. That contrasts with a weaker 3-year total shareholder return of 62.25% and 5-year total shareholder return of 89.17%. Even though the 1-year total shareholder return of 14.05% shows more recent improvement, sentiment appears firmer in the short term while longer term holders have still faced heavy losses.

If this kind of offline entertainment push catches your interest, it might be worth seeing which other media and streaming names are shifting toward tech enabled experiences through high growth tech and AI stocks.

With iQIYI posting a recent 1 year total shareholder return of 14.05% but much weaker 3 and 5 year results, the key question is whether today’s US$2.11 share price still leaves upside or if markets are already pricing in future growth.

Most Popular Narrative: 9.9% Undervalued

Compared with the last close at US$2.11, the most followed narrative pegs iQIYI’s fair value a little higher, suggesting some pricing gap to investigate.

Initiatives in IP-based consumer products and offline "experience" businesses (theme parks and immersive centers) are opening new, scalable revenue streams beyond core streaming, enhancing overall monetization and potentially improving net margins as these asset-light strategies mature.

Curious what kind of revenue mix justifies that higher value? The narrative leans on steadier top line growth, rising margins, and a lower future earnings multiple. Want to see how those ingredients fit together?

Result: Fair Value of $2.34 (UNDERVALUED)

However, that upside story can fray quickly if costly blockbuster content does not land with viewers, or if overseas growth stalls against stronger global rivals.

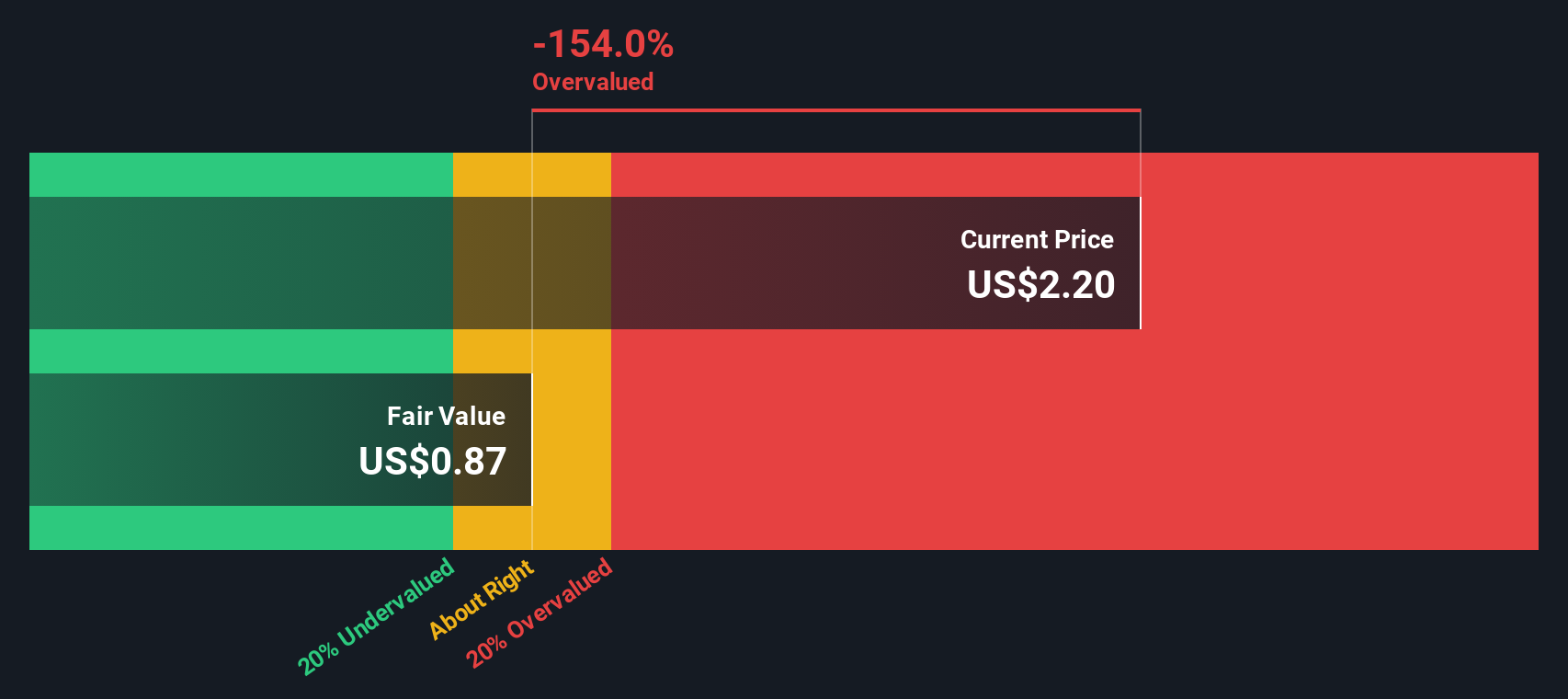

Another View: Our DCF Model Flags Overvaluation

The narrative and consensus target suggest around 10% upside, but our SWS DCF model points the other way. On that basis, iQIYI’s fair value comes out at about US$1.70, below the current US$2.11 price. This implies less of a safety buffer than the bullish story suggests.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out iQIYI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 881 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own iQIYI Narrative

If you look at the numbers and reach a different conclusion, or just want to test your own assumptions, you can build a custom view in minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding iQIYI.

Ready for more investment ideas?

If iQIYI has you thinking about what else might be worth a closer look, do not stop here. Broaden your watchlist before the next move passes you by.

- Explore potential mispricings by scanning these 881 undervalued stocks based on cash flows that the market may not be fully appreciating yet.

- Focus on future tech themes with these 26 AI penny stocks that are tied to real business models, not just hype.

- Look at income-oriented opportunities through these 12 dividend stocks with yields > 3% that currently offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.