A Look At Jack Henry And Associates (JKHY) Valuation After Recent Share Price Pullback

Jack Henry & Associates, Inc. JKHY | 153.93 | +1.66% |

Why Jack Henry & Associates Is On Investors’ Radar

Jack Henry & Associates (JKHY) has drawn attention after a recent share pullback, with the stock down about 10% over the past month and 4% year to date, despite slightly positive 1 year total returns.

For investors tracking longer trends, Jack Henry & Associates shows a 2% total return over the past 3 months, 6.6% over 3 years, and 24.1% over 5 years. This raises questions about how current pricing lines up with its financial profile.

The recent 9.8% 1 month share price decline to US$170.62 contrasts with mildly positive multi year total shareholder returns. This hints that sentiment has cooled in the short term even as the longer track record remains positive.

If this softer momentum has you thinking about where else growth stories might emerge in fintech and beyond, it could be worth checking out 23 top founder-led companies as a fresh source of ideas.

With the shares pulling back even as analysts set an average price target above the current US$170.62 level and some models flag a small intrinsic premium, you have to ask: is Jack Henry & Associates now undervalued, or is the market already pricing in its future growth?

Most Popular Narrative: 16% Undervalued

With Jack Henry & Associates last closing at $170.62 against a most followed fair value estimate of $202.67, the current price sits below that narrative anchor and raises a clear question about what is built into those projections.

The company is experiencing accelerated adoption of its cloud-native platforms and SaaS offerings (cloud revenue up 11% year-over-year, now 32% of total revenue and 77% of core clients hosted in private cloud), which is expected to drive higher recurring revenue, improved margins, and higher free cash flow conversion as legacy on-premise contracts decline.

Curious what kind of revenue run rate, margin profile, and future earnings multiple are baked into that fair value? The narrative leans on specific growth, profitability and discount rate assumptions that you may or may not agree with, but they are all laid out for you to weigh.

Result: Fair Value of $202.67 (UNDERVALUED)

However, you also need to weigh risks, such as bank consolidation shrinking Jack Henry’s customer base and pricing pressure from fintech rivals squeezing margins if competition intensifies.

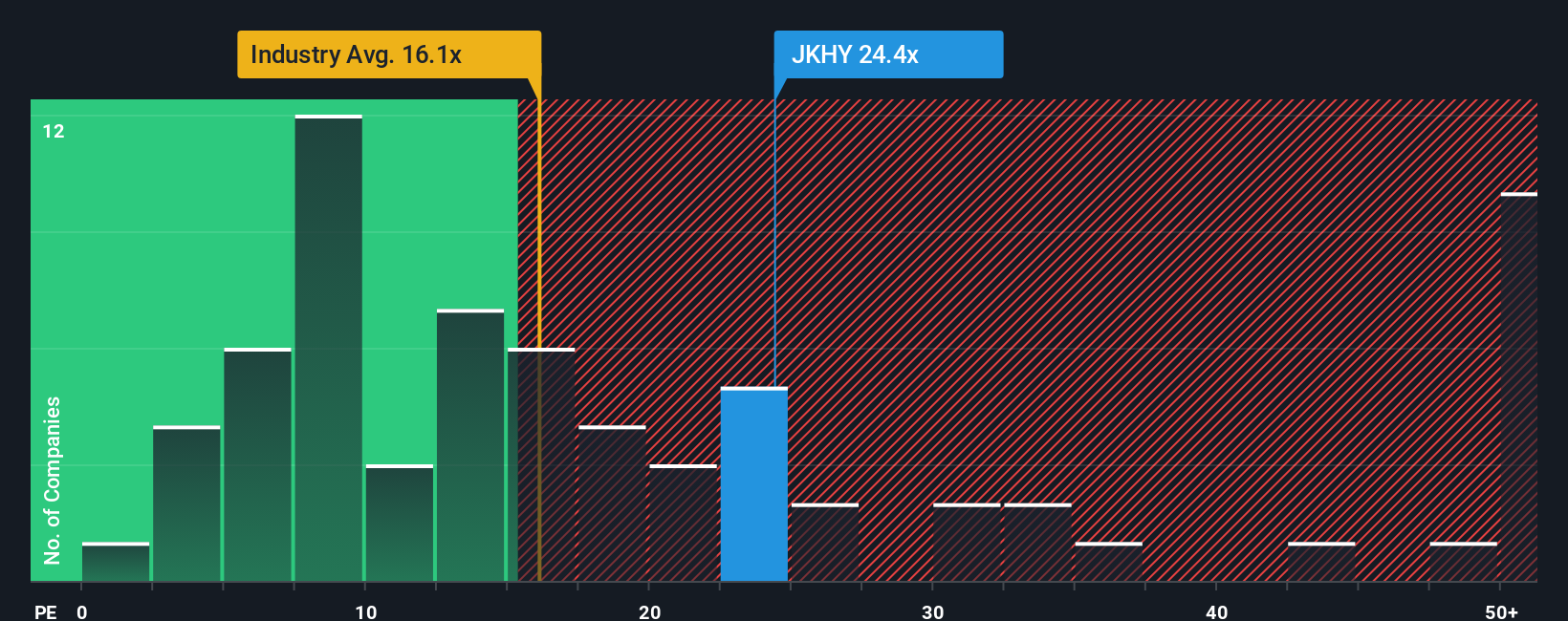

Another View: Multiples Paint A Richer Price

The fair value narrative points to Jack Henry & Associates looking 16% undervalued at around $170.62, but the picture changes when you look at simple valuation ratios. On a P/E of 24.3x, the shares sit well above the US Diversified Financial industry at 15.6x and our fair ratio of 14.3x.

In plain terms, the current price already assumes a much higher earnings valuation than both the wider industry and the level our fair ratio suggests the market could move toward over time. That raises a practical question for you: is this a quality name that justifies paying up, or are you leaning into valuation risk that limits your margin of safety?

Build Your Own Jack Henry & Associates Narrative

If you are not fully aligned with these views or prefer to rely on your own research, you can build a tailored thesis in minutes: Do it your way.

A great starting point for your Jack Henry & Associates research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready For More Investment Ideas?

If Jack Henry & Associates has sharpened your thinking, do not stop here. The real edge comes from comparing it with a wider set of opportunities tailored to your goals.

- Target potential mispricing by reviewing companies our screener tags as 51 high quality undervalued stocks that may offer a wider margin of safety.

- Prioritise resilience by scanning solid balance sheet and fundamentals stocks screener (45 results) so you can focus on businesses with stronger financial footing.

- Hunt for under-the-radar opportunities through our screener containing 24 high quality undiscovered gems that most investors might be overlooking right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.